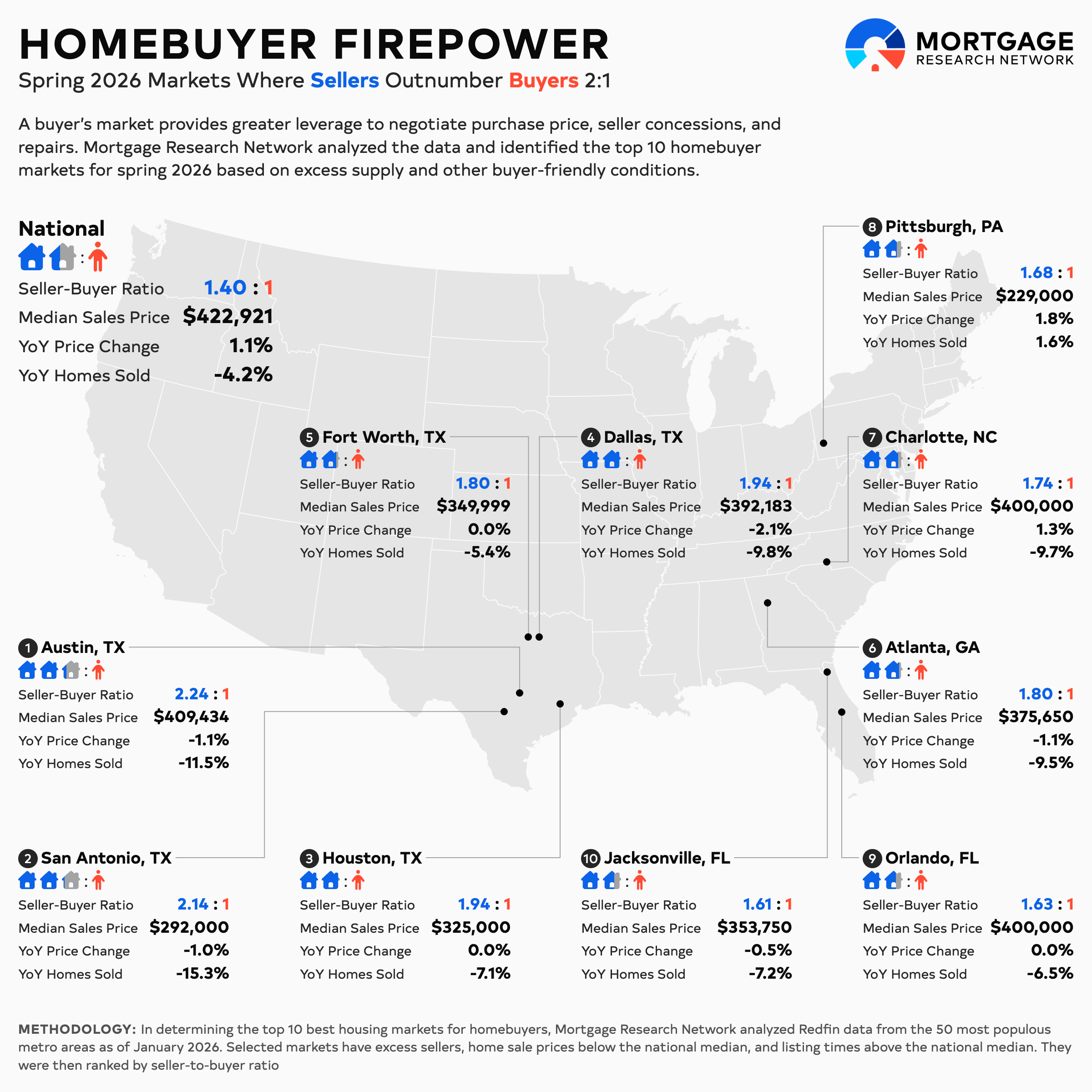

Why Buying Your First Home Feels So Hard Right Now

For many first-time homebuyers, it can feel like today’s housing market is working against them. Mortgage rates are still far above the historic lows seen during the pandemic. Home prices remain elevated in many areas of the country. And even when buyers can afford monthly payments on paper, limited inventory makes it challenging to find the right home at the right price.

At the same time, many people hear that investors are driving up prices by purchasing large numbers of homes. But on a recent episode of the Real Estate Update Podcast, housing analyst Rick Sharga, CEO of CJ Patrick Company, says that explanation is often overstated.

“There are a lot of myths about investor purchases,” Sharga said. “One is that they’re gobbling up all the available inventory, and that’s not true.”

Instead, the real issue is more structural: affordability, supply shortages, and financial constraints that affect both buyers and sellers.

Affordability Is the Core Problem

At the center of today’s housing challenges is affordability. Over the past several years, buyers have faced rising home prices, higher mortgage rates, increasing insurance premiums, and property taxes that continue to climb throughout the country. Meanwhile, wages have not kept pace in many areas.

Sharga noted that investor activity may appear larger than it is because traditional buyers have stepped back.

“Even though investors bought fewer homes last year than they did the year before, their share of purchases went up simply because traditional home buyers, more and more, were on the sidelines because they couldn’t afford anything they could find to buy,” he said.

That shift creates a ripple effect across the entire market:

- Fewer buyers qualify for homes at current prices

- Existing homeowners are less likely to sell

- Inventory remains tight

- Competition increases for the few affordable homes available

For first-time buyers, the issue is often not just home prices, but monthly affordability. Even a small increase in mortgage rates can significantly increase payments and reduce purchasing power.

The “Golden Handcuffs” Effect on Inventory

A major reason housing inventory remains tight is what experts call the “lock-in effect.” Millions of homeowners refinanced during 2020 and 2021 when mortgage rates were at historic lows. Today, those homeowners are hesitant to move because doing so would dramatically increase their monthly payments.

Sharga described it simply as “golden handcuffs.”

He explained that the issue is not emotional, but mathematical. If someone has a low-rate mortgage, trading up to a more expensive home at today’s rates can double their monthly payment.

This creates a chain reaction in the housing market:

- Fewer homeowners list their homes

- Fewer starter homes become available

- First-time buyers face limited options

- Competition increases for entry-level properties

Even when people want to move, the financial trade-off often makes it difficult to justify doing so.

Why Builders Are Not Adding Enough Affordable Homes

Another common question is why new construction is not filling the gap. The answer comes down to cost and incentives.

According to Sharga, builders face significant upfront expenses before construction even begins.

“The average cost nationally according to Fannie Mae for a builder to break ground, this is before they start putting shovels in the ground, is about $100,000,” he said.

That figure includes land, permits, infrastructure, materials, labor, and financing costs. As a result, builders often focus on higher-priced homes where margins are stronger.

Key challenges for builders include:

- High land and development costs

- Expensive materials and labor

- Regulatory and zoning delays

- Limited profit margins on entry-level homes

The result is a shortage of affordable starter homes. In addition, the U.S. has underbuilt housing for years relative to population growth, which means the supply gap is long-standing and not easily fixed.

Are Investors Really the Main Problem?

Investor activity is often blamed for housing affordability issues, but the data tells a more nuanced story.

Sharga pointed out that large institutional investors represent a very small share of the overall market.

“If you look at all of the investors who own 350 or more properties and all the purchases they made last year, they bought about 36,000 homes,” he said.

In context, that is a small portion of total housing activity.

“There were about 4 million homes that traded hands last year,” he added. “You’re dealing with about 0.9% of all home sales.”

While investors are more active in some regions, especially fast-growing Sun Belt and Southeast markets, they are not the primary driver of national affordability challenges.

Investor behavior also tends to follow a pattern:

- Target older or distressed homes

- Focus on lower-cost or rental-friendly markets

- Avoid overbidding in competitive situations

- Look for long-term rental returns rather than emotional purchases

That means they often compete in a different segment of the market than typical first-time buyers.

Why Local Markets Matter More Than National Trends

Housing is not a single national market. There are thousands of local markets operating under different conditions.

Some areas are driven by tourism and short-term rentals. Others are shaped by job growth, land availability, or strict zoning laws. Coastal cities may face severe supply shortages, while inland markets could still offer relative affordability.

Sharga noted that states like Hawaii and Montana show higher investor ownership rates largely due to tourism and vacation rental demand.

For buyers, this means focusing on local conditions rather than national headlines. Before buying, first-time buyers should evaluate:

- Local inventory levels and days on market

- Insurance costs and property taxes

- Neighborhood-level price trends

- School districts and commute patterns

- Future development or zoning changes

Understanding these factors can reveal opportunities that broader statistics might hide.

What First-Time Buyers Can Actually Control

Many factors in the housing market are outside a buyer’s control. Larger economic forces drive mortgage rates, inflation, and inventory levels. But buyers still have meaningful control over their own readiness.

One of the most important steps is getting pre-approved before beginning a home search.

“If you and somebody else make the same offer in terms of price on a house, your ability to show that you’re going to be able to get that financing probably gives you a little bit of a leg up,” Sharga said.

Buyers should also focus on improving their financial profile:

- Paying down high-interest debt

- Strengthening credit scores

- Building emergency savings

- Avoiding large new purchases before closing

Another key factor is understanding total monthly costs, not just purchase price. A home’s affordability includes mortgage payments, taxes, insurance, maintenance, and HOA fees.

This is especially important in states where insurance costs have risen significantly in recent years.

Should Buyers Wait for Better Conditions?

Many first-time buyers are waiting for mortgage rates to fall or home prices to drop before entering the market. However, Sharga warns that timing the market is extremely difficult.

“People wait for mortgages to bottom out, they wait for home prices to bottom out. You’re almost inevitably going to miss the bottom,” he said.

Waiting can sometimes backfire because lower rates often bring more buyers back into the market, increasing competition and pushing prices higher.

Fixer-Uppers: Opportunity With Risk

With affordability stretched, some buyers consider homes that need repairs. These properties can offer value, but they also come with risk if costs are underestimated.

Sharga highlighted common mistakes with fixer-uppers based on his experience with real estate investors:

“The two most common mistakes I’ve seen investors make in the fix-and-flip market is they typically fall in love with the property and overestimate what they’re going to be able to sell it for,” he said. “And they typically underestimate how much it’s going to cost to repair the property.”

Before purchasing a fixer-upper, buyers should carefully evaluate:

- Roof condition

- Plumbing and electrical systems

- HVAC systems

- Foundation stability

- Water damage or mold risks

At the same time, smaller upgrades can still make a meaningful difference. Fresh paint and basic curb-appeal improvements can add value and enhance livability without incurring overwhelming costs.

Renting vs Buying in Today’s Market

Even with challenges, homeownership still offers long-term advantages for many buyers. These include equity building, housing stability, and potential appreciation over time.

However, buying is not always the right short-term choice. Renting may make more sense for people who are still building savings or who expect to move within a few years.

The decision often depends on:

- Job stability

- Savings and credit readiness

- Local price-to-rent ratios

- How long the buyer plans to stay in the area

Economic Uncertainty Still Shapes Housing

Housing does not operate in isolation. Inflation, bond markets, energy prices, and global events heavily influence mortgage rates.

Sharga noted that rising oil prices and geopolitical uncertainty can directly affect mortgage rates by impacting bond yields.

“We’ve seen oil prices go up, we’ve seen that kind of upset the bond markets,” he said. “Because of that, bond yields have gone up significantly, which is taking mortgage rates back up with them.”

This reinforces a key point: housing conditions can shift quickly, and certainty is rare.

Putting It All Together

First-time homebuyers today are facing a difficult but not impossible market. Affordability challenges, limited inventory, and higher borrowing costs are real constraints, but they are driven by broader structural forces rather than by any single cause, such as investor activity.

As Rick Sharga explained, many of the common fears in the market are overstated. The real challenge is balancing income, monthly payments, and available supply in a constrained environment.

Success for buyers often comes down to preparation and discipline:

- Getting financially ready early

- Understanding true monthly affordability

- Staying flexible on location and property type

- Avoiding attempts to time the market perfectly

Or as Sharga put it, the key is simple:

“If you find a house that you really like and you can afford to buy that house at today’s prices with today’s mortgage rates, and you plan to stay there for at least three to five years, don’t wait.”