Buying a home has become more difficult over the past few years. While mortgage rates have come down from their recent highs, elevated home prices and affordability concerns continue to make homeownership feel out of reach for many first-time buyers.

On a recent episode of the Real Estate Update Podcast, host Paul Centopani sat down with Phil Ganz, president of NextWave Mortgage, to discuss the biggest affordability challenges facing today's buyers. Their conversation covered everything from down payment assistance and seller credits to financial literacy and why understanding your financing options can be just as important as finding the right home.

Here are some of the key takeaways from that conversation and what they mean for prospective homebuyers.

Affordability Looks Different Across the Country

Housing affordability is often discussed as though it's a single national issue. In reality, the obstacles buyers face can vary significantly depending on where they live.

Ganz summed it up this way: "When you look at the United States, you've got 50 different states. You've basically got 50 different countries."

In many parts of the Midwest and South, the biggest challenge is often saving enough money for a down payment and closing costs. Monthly mortgage payments may still be manageable relative to local incomes, allowing many buyers to qualify once they have enough cash saved.

The situation can be very different in higher-cost markets.

Ganz pointed to states like California, Massachusetts, and New York, where affordability extends beyond simply coming up with a down payment. As he noted during the podcast, "Even if you're a doctor," buying a home can still be a challenge in some markets.

That's why buyers shouldn't assume the same advice applies everywhere. The financing strategy that works well in one market may not be the right solution somewhere else.

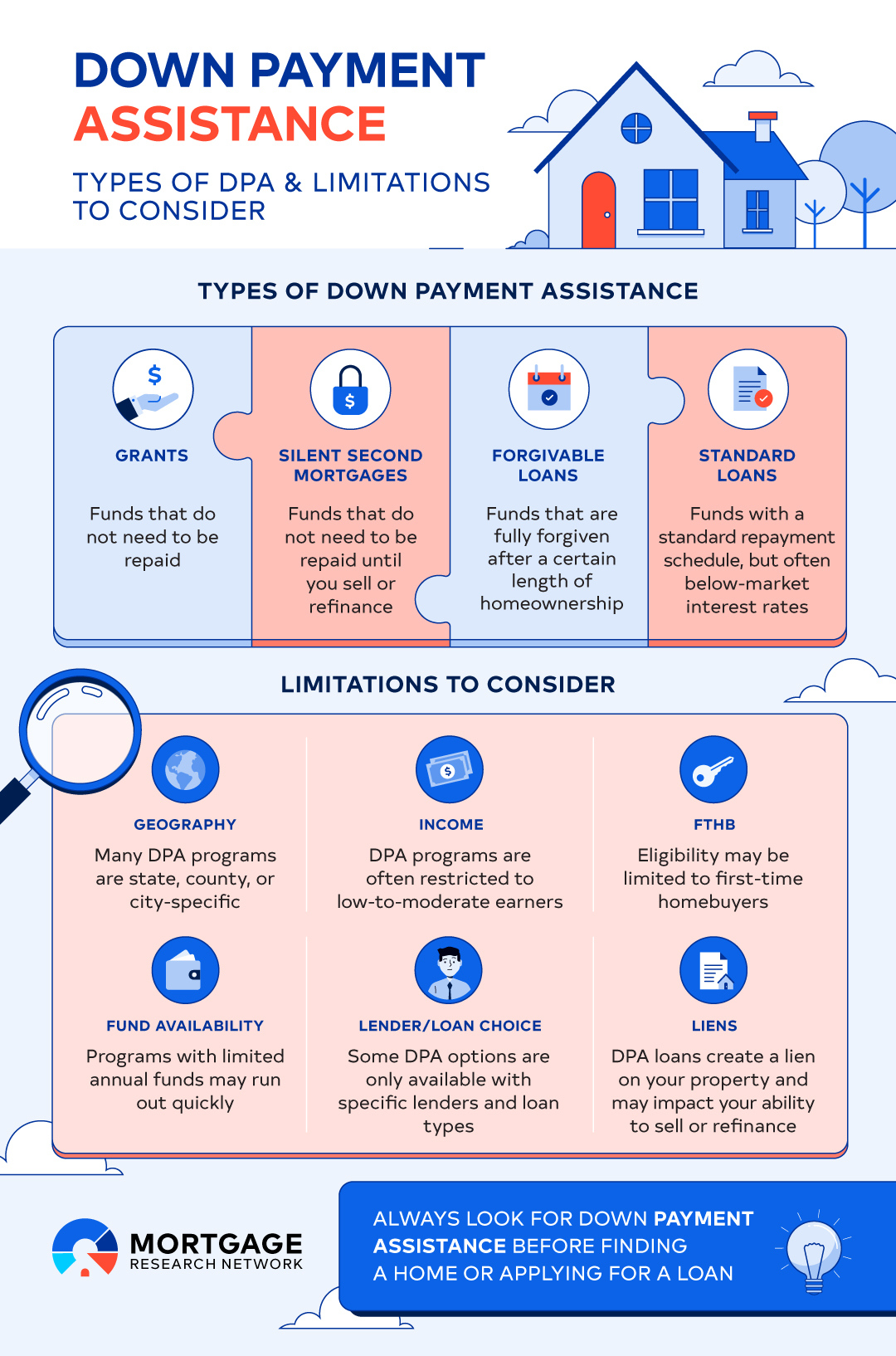

Down Payment Assistance Isn't Just One Program

One misconception among first-time buyers is that down payment assistance is a single government program.

In reality, assistance is available through state housing agencies, local governments, nonprofit organizations, employers, and other community organizations. Eligibility requirements vary by program, and many buyers qualify without realizing these resources exist.

Some of the most common forms of assistance include:

- Grants that typically don't have to be repaid if you’re eligible.

- Deferred or forgivable loans that become payable only under certain circumstances, such as selling the home or moving before satisfying occupancy requirements.

- Low-interest second mortgages that help cover down payment or closing costs.

- Shared appreciation programs that provide upfront assistance in exchange for a portion of the home's future appreciation.

Because each program works differently, buyers should take time to understand both the immediate benefits and any long-term obligations before deciding which option best fits their financial goals.

Shared Appreciation Programs Can Help – But They Aren't Right for Everyone

Shared appreciation programs have become increasingly common in some of the nation's most expensive housing markets.

These programs can provide substantial financial assistance, making homeownership possible for buyers who otherwise couldn't afford to purchase a home. In exchange, however, the organization providing the funds shares in the home's future appreciation.

Discussing one California program, Ganz explained that participants don't simply repay the original assistance. "They want that 20% back," he said, "and they want 20% of the appreciation of the home when you sell."

That doesn't necessarily make these programs a bad option.

For some buyers, especially those purchasing in extremely high-cost housing markets, sharing a portion of future appreciation may still be preferable to remaining renters indefinitely.

However, buyers should understand exactly how these programs work before signing any paperwork. Home equity has historically been one of the primary ways families build wealth, and giving up part of that future appreciation is an important tradeoff to consider.

Will Down Payment Assistance Make Your Offer Less Competitive?

Some buyers hesitate to use down payment assistance because they worry sellers will view their offer less favorably.

According to Ganz, that's generally not how these programs work.

He explained that down payment assistance is typically treated much like gift funds during the mortgage approval process and usually isn't highlighted in a buyer's offer.

That said, market conditions still matter.

In highly competitive housing markets, buyers making larger down payments may have an advantage when competing against multiple offers. In many other markets, however, buyers successfully purchase homes every day while using down payment assistance and other affordability programs.

Working with an experienced lender can help buyers identify the programs they're eligible for and understand how to structure a competitive offer.

Seller Credits Can Reduce Your Upfront Costs

Coming up with a down payment is only part of the financial challenge. Closing costs can add thousands of dollars to the amount buyers need to purchase a home.

One way to reduce those upfront expenses is through seller credits.

A seller credit allows the seller to pay some or all of the buyer's closing costs as part of the purchase agreement. In some cases, buyers may agree to a slightly higher purchase price in exchange for those credits, allowing them to finance more of their upfront expenses instead of paying cash at closing.

Ganz noted that many successful first-time buyers combine multiple affordability tools rather than relying on just one strategy.

Depending on market conditions, buyers may be able to combine:

- Down payment assistance programs

- Seller credits toward closing costs

- Gift funds from eligible family members

- Low-down-payment mortgage programs

Using more than one of these strategies can significantly reduce the cash needed to purchase a home and may allow buyers to enter the market sooner than expected.

Should You Wait for Mortgage Rates to Fall?

Many prospective buyers continue to delay purchasing a home, hoping mortgage rates will fall or home prices will become more affordable.

While that may seem like a reasonable strategy, predicting where the housing market is headed is easier said than done.

Ganz believes waiting for perfect conditions often keeps buyers on the sidelines longer than necessary. "The biggest mistake that a lot of first-time homebuyers make is wait too long," he said during the podcast.

Part of the problem, he argues, is that many buyers expect every piece of the puzzle to fall into place before they're willing to move forward. "They want everything to be right," Ganz said. "It's like a Hallmark movie at Christmas time."

In reality, every housing market comes with tradeoffs.

Lower mortgage rates can improve affordability, but they also tend to bring more buyers into the market, increasing competition. On the other hand, slower housing markets may create opportunities to negotiate a lower purchase price or ask sellers to contribute toward closing costs.

Rather than trying to predict the perfect time to buy, prospective homeowners may benefit more from focusing on whether they're financially prepared when the right home becomes available.

Financial Literacy Is Just as Important as Financing

Finding the right loan is only part of the homebuying process. Understanding how that loan works can be just as important.

During the interview, Ganz explained that his team spends considerable time reviewing loan estimates, discussing available mortgage programs, and walking buyers through different financing scenarios before they begin shopping for a home.

As he put it, "We don't do hypotheticals. We give you the facts and the truth."

That education can help buyers better understand how much home they can realistically afford, how different loan programs compare, and what they'll need to bring to closing.

While technology has made it easier than ever to apply for a mortgage online, it hasn't replaced the value of speaking with an experienced lending professional who can explain your options and answer questions along the way.

Building Toward Homeownership Often Takes Time

Affording a home isn't simply about finding the right mortgage program. For many buyers, it also means developing healthy financial habits well before they begin house hunting.

That may involve saving consistently, paying down debt, improving credit, or adjusting spending priorities to meet long-term goals.

Ganz believes financial education should begin long before someone applies for a mortgage. In fact, he said, "Financial literacy should begin at day zero."

While every household's financial situation is different, preparing to buy a home often requires patience and planning. Small improvements – whether it's paying off a credit card balance, increasing monthly savings, or improving a credit score – can make a meaningful difference when it's time to qualify for a mortgage.

Know Your Numbers Before You Start Shopping

When asked for his top piece of advice for first-time buyers, Ganz didn't hesitate.

"Know your numbers," he said.

More specifically, he recommends sitting down with a mortgage professional and reviewing a loan estimate before beginning your home search. Understanding your estimated monthly payment, cash needed at closing, and available financing options can help you shop with greater confidence.

Before you begin looking at homes, it's worth making sure you understand:

- How much cash you'll need to close

- Your estimated monthly mortgage payment

- Which loan programs you qualify for

- Whether you're eligible for down payment or closing cost assistance

- A monthly payment that comfortably fits your budget – not simply the maximum a lender is willing to approve

Having those answers before making an offer can help buyers make informed financial decisions instead of emotional ones.

Bottom Line

Today's housing market continues to present challenges for first-time buyers, but higher home prices and mortgage rates don't necessarily put homeownership out of reach.

As Ganz explained on the Real Estate Update Podcast, buyers have more tools available than many people realize. Down payment assistance, seller credits, low-down-payment mortgage programs, and personalized guidance from an experienced lender can all help make purchasing a home more attainable.

No two buyers – or housing markets – are exactly alike. Taking the time to understand your financing options, research available assistance programs, and determine what fits comfortably within your budget can put you in a much stronger position when you're ready to buy.