If you’ve spent any time looking at homes lately, you probably know the feeling: the math of homeownership is broken. We are currently living through one of the most lopsided housing markets in American history.

It is a market defined by a paradox. Millions of people want to buy, but despite active listings rising over the past couple of years, the number of homes on the market is still far lower than it was a decade ago. But beyond that, what is available feels financially out of reach for the average earner.

In a recent session of the Real Estate Update podcast, Hannah Jones, Senior Economist at Realtor.com, sat down with Paul Centopani to peel back the layers of this crisis. The headline figure? The U.S. was short 4 million homes in 2025, up from 3.8 million in 2024. The shortage is also known as the “supply gap.”

But how did we get here? It isn't just one bad policy or a single year of high interest rates. It is a compounding "perfect storm" of high construction costs, restrictive zoning, and a generation of buyers facing hurdles their parents never imagined.

The Supply-Side Stagnation: Why Builders Are "Squeamish"

The most fundamental rule of economics is supply and demand. In a healthy market, high demand and rising prices signal to builders that it is time to ramp up production. However, that mechanism has hit a wall. Builders aren't just being cautious; they are facing a landscape where the cost of entry is often higher than the potential profit.

The Cost of a "Stick in the Ground"

Today, new construction is significantly more expensive than it was prior to 2020. This isn't just about the price of lumber, which famously spiked and then stabilized, but about the holistic cost of development.

Labor Shortages: The construction industry lost a massive portion of its skilled workforce during the 2008 crash, and it never truly recovered. Today, specialized labor (plumbers, electricians, and HVAC technicians) is at a premium.

Material Volatility: While lumber prices have cooled, the cost of concrete, electrical components, and specialized appliances remains elevated due to global supply chain shifts.

Borrowing Costs for Builders: Builders rely on loans to fund their projects. When the Fed raises rates, it doesn't just impact your mortgage; it impacts the builder’s ability to finance the development of an entire subdivision.

"We see on the construction side, there's increasing labor costs, increasing material costs," Jones explains. "Builders are a little bit antsy, a little bit squeamish to risk overbuilding... they ratchet down their construction as they feel these cost pressures and know they can't really pass those costs on to buyers."

The Zoning Paradox

Even if a builder has the capital and the labor, they often lack the permission. In high-demand regions, particularly the Northeast and parts of California, zoning laws often mandate that homes be built on large, expensive lots. This effectively outlaws the "starter home."

When a builder is forced to buy a large lot and pay high regulatory fees, they cannot afford to build a $250,000 house; they must

build a $600,000 house just to break even. This is why we see a surplus

of "luxury" builds while the entry-level market remains a desert.

The "Missing" Generation and the 30-Grand Hurdle

One of the most startling statistics from Realtor.com is that 1.8 million potential Gen Z and Millennial households are currently "missing" from the market. These aren't people who don't want to own a home; they are people for whom the barrier to entry has become a vertical wall.

The Death of the Starter Home

For decades, the "starter home" was the ladder to the middle class. You bought a small, 1,200-square-foot bungalow, built equity for five years, and then moved up. Today, that ladder is missing its bottom rungs.

Jones points out that the share of homes priced under $350,000 has plummeted. Before the pandemic, this bucket represented a massive portion of the market. Today, it’s down to a third or less. This creates a "vicious cycle" where the few affordable homes that do hit the market are immediately swarmed by dozens of offers, driving the price up and out of reach again.

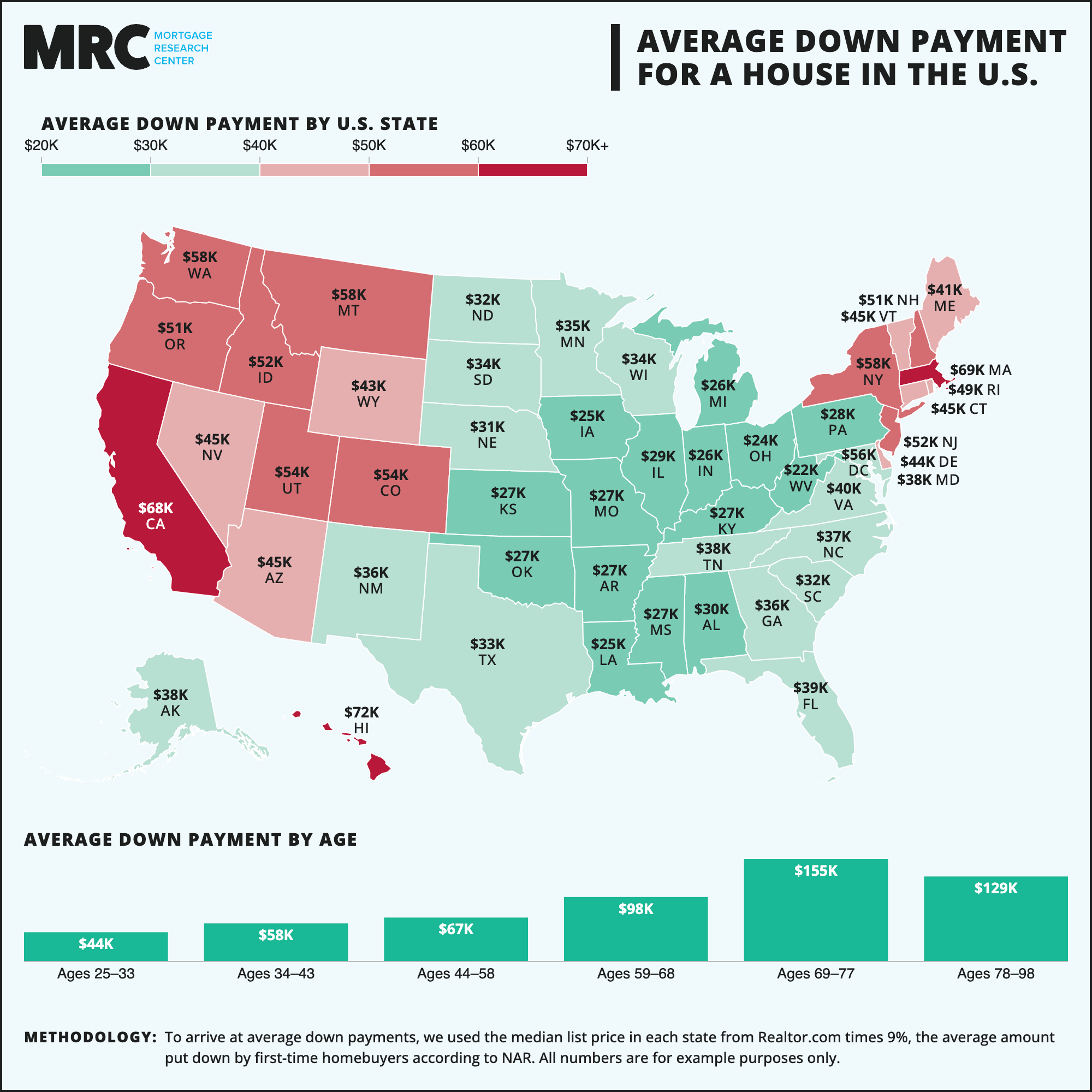

Forget the Avocado Toast: The Down Payment Reality

The cultural trope that young people can't afford homes because of lifestyle spending is a mathematical fallacy. "Considering the typical down payment today is about $30,000... that’s going to be a lot of avocado toast to avoid eating," Jones quips.

In many markets, $30,000 is actually a conservative estimate. If you’re aiming for a 20% down payment on a median-priced home in a major metro area, you’re looking at $70,000 to $100,000. For a young worker whose rent has also increased by 20% over the last few years, saving that amount is a decades-long project without "the Bank of Mom and Dad."

Thankfully, there are mortgage options available with far smaller down payments. However, for many buyers, even coming up with just 3% of the price of a home – as well as the upfront closing costs – can be a challenge.

Debunking the "15 Million Vacant Homes" Myth

A common talking point on social media is that we don't have a supply problem, we have a distribution problem. Critics point to Census data showing roughly 15 million vacant units in the U.S. and suggest we should simply occupy those. Jones clarifies why this isn't a viable solution.

Not All Vacancies Are Created Equal

When the Census Bureau counts a "vacant" unit, they are using a very broad definition.

Seasonal and Recreational: A huge chunk of these are beach houses, mountain cabins, and "snowbird" condos that aren't intended for year-round residency.

Units in Transition: These are homes that have been sold but the new owners haven't moved in yet, or apartments that are currently between tenants.

The Location Mismatch: Many truly vacant, abandoned homes are located in "legacy cities" or rural areas where there are no jobs. You cannot solve a housing crisis in Austin or Boston by pointing to a vacant house in a declining rural township.

"Once we take out all those pieces, we’re seeing a much smaller portion of the pie," Jones says. "Vacancy rates for homes that can actually be occupied are still pretty historically low."

Legislative Lifelines: Will Washington Save the Market?

The federal government has finally shifted its focus toward the supply side of the equation. Historically, many government programs focused on "demand-side" help—like first-time homebuyer credits. The problem? Giving people more money to buy homes when there are few homes to buy just drives prices higher.

The Housing for the 21st Century Act

This legislation, which recently passed a Senate vote, is designed to incentivize local governments to ditch restrictive zoning. By offering federal grants to cities that allow for higher density (like duplexes and "missing middle" housing), the hope is to jumpstart construction.

Executive Orders and Community Banks

Two recent executive orders have also made waves. One aims to cut "red tape" in construction, while the other seeks to expand mortgage credit by empowering community banks.

Some observers are wary, remembering the "loose" lending that led to the 2008 subprime crisis. However, Jones notes a key difference: "The [community] banks will keep loans on their books... they have skin in the game, not to go lending to people who are not credit-worthy."

This is a stark contrast to the 2000s, where bad loans were packaged into "toxic" securities and sold off, leaving the original lender with zero risk.

The Path Forward: Think Global, Act Local

If the federal government is the "macro" solution, the "micro" solution happens at your local City Council meeting. This is where the real power over your neighborhood lies.

If you want more affordable housing, it often means supporting "density" – the very thing many current homeowners fight against. "Advocating for that, talking to your local policy drivers about... making it possible to build more on smaller lots," is the most effective thing a citizen can do, according to Jones.

What to Watch This Spring

Now that we’re into the traditional spring homebuying season, the market is at a crossroads. We’ve seen mortgage rates dip and then bounce back, leaving buyers in a state of "rate fatigue."

Jones is watching for a "revival," but it will likely be localized. Markets like Austin, which saw a massive price correction over the last 18 months, are now seeing a "leveling out" that might finally feel like a fair entry point for buyers.

The Bottom Line

The 4 million home gap didn't happen overnight, and it won't be solved by a single spring season or one piece of legislation. It will require a sustained effort to bring down construction costs, modernize zoning, and help young buyers bridge the down payment gap.

Until then, the best strategy for buyers is to remain flexible and informed. As Hannah Jones suggests, "Having that knowledge is definitely helpful... because it can be really scary and challenging if you don’t live and breathe housing market stuff."