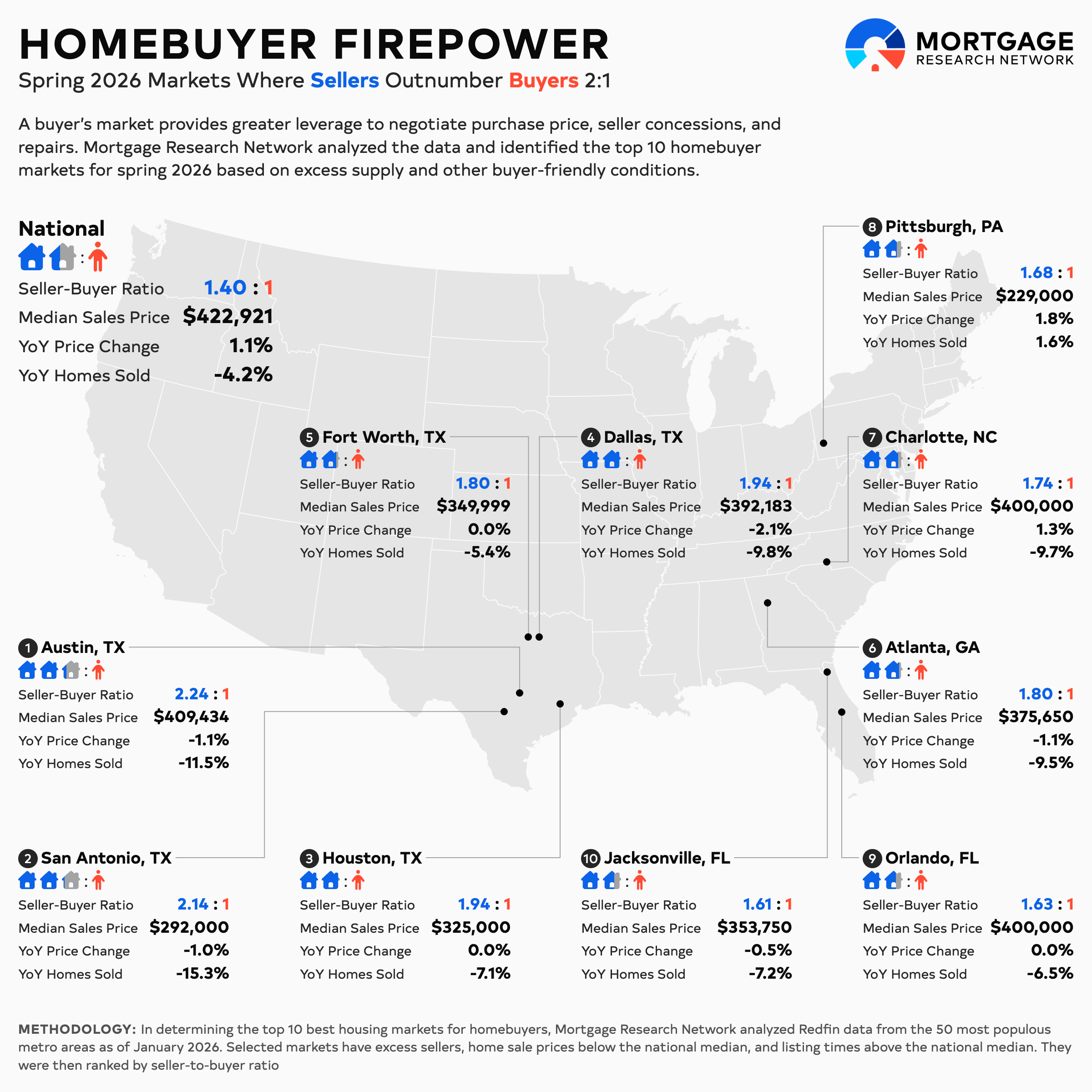

For many aspiring homeowners, the housing market can feel frustratingly contradictory. Mortgage rates remain elevated compared to the record lows of the pandemic era, home prices continue climbing in many parts of the country, and inventory shortages can make finding an affordable home difficult.

Yet the housing market isn't struggling equally everywhere.

On a recent episode of the Real Estate Update podcast, Mark Fleming, Chief Economist at First American, discussed how affordability, inventory, and buyer opportunities vary significantly from one market to another. His insights help explain why some buyers face intense competition while others are beginning to see more options emerge.

For first-time buyers especially, understanding these trends can help set realistic expectations and uncover opportunities that might otherwise be overlooked.

Affordability Depends on Where You're Looking

When people talk about a national housing affordability problem, they're not wrong. However, affordability challenges can look very different depending on location.

According to Fleming, some of the biggest affordability pressures today aren't necessarily in the places many buyers would expect.

"Generally, in markets … in the Northeast and the Midwest and the Rust Belt are markets that have relatively low inventory still and actually pretty fast house price appreciation," he said.

Cities throughout the Midwest and Northeast continue to face inventory shortages, which puts upward pressure on prices. In some markets, home values are still increasing at annual rates of 6% or 7%, making it difficult for wages to keep pace.

Meanwhile, parts of the South and Sun Belt have experienced a different dynamic. Areas that saw explosive growth during the pandemic are now seeing inventory increase and price growth slow. Some markets have even experienced modest price corrections.

The result is a housing market that is increasingly regional rather than national. Conditions in one city may bear little resemblance to conditions a few states away.

Why Entry-Level Buyers Face the Biggest Challenge

Not all homebuyers experience the market the same way. According to Fleming, entry-level buyers are facing some of the greatest obstacles. The reason comes down to a housing market chain reaction that has largely stalled.

In a healthy housing market, first-time buyers purchase starter homes. The people selling those homes move into larger homes, and those sellers move into different homes of their own. This process creates a continuous flow of housing inventory through multiple price ranges.

Today, that process is broken.

Many existing homeowners are reluctant to sell because they secured mortgage rates near 3% during the pandemic. Selling their current home often means giving up a historically low rate and replacing it with a significantly higher one.

As Fleming explained, many homeowners are simply choosing to stay put. The result is fewer starter homes becoming available for first-time buyers.

A few important housing concepts help explain what's happening:

- Move-Up Buyer: A homeowner who sells their current property and purchases a larger, newer, or more expensive home.

- Inventory: The number of homes currently available for sale in a market.

- Mortgage Rate Lock-In Effect: The tendency of homeowners to remain in their current homes because they don't want to give up a mortgage with a significantly lower interest rate than today's market rates.

When move-up buyers stop moving, fewer homes become available at the entry level. That shortage can make competition especially fierce for affordable homes.

Why New Construction Is Becoming More Important

One surprising consequence of the inventory shortage is that some first-time buyers are increasingly turning to newly built homes.

"Many first-time homebuyers are actually now buying new homes instead," Fleming said.

Traditionally, first-time buyers often entered the market through existing homes. But because many current homeowners aren't selling, builders have an opportunity to fill some of the gap.

New construction offers several advantages:

- More available inventory in some markets

- Builder incentives that may reduce upfront costs

- Opportunities to customize finishes and features

- Less immediate maintenance and repair work

Builders have also become more creative in helping buyers manage affordability. Some are offering mortgage rate buydowns, closing cost assistance, or smaller floor plans designed specifically for entry-level buyers.

While new homes aren't always less expensive than existing homes, they may offer more opportunities in markets where resale inventory remains limited.

Increasing Affordability Starts With Lowering Monthly Costs

When discussing affordability, many buyers focus exclusively on home prices. Fleming argues there are several ways buyers can improve affordability even when prices remain high.

Some of the most common strategies include:

- Increasing the down payment

- Purchasing mortgage discount points

- Considering an adjustable-rate mortgage

- Expanding the search to less expensive neighborhoods

- Looking at smaller homes or older properties

The challenge, of course, is that saving additional money for a down payment is often easier said than done. "Historically, the main reason why people can't afford a home is less the mortgage payment and more the down payment," commented Fleming.

Even buyers who can comfortably afford a monthly payment may struggle to save enough cash for upfront costs.

Understanding Mortgage Points

One affordability strategy many buyers overlook is purchasing mortgage points. Fleming explained that borrowers can pay an upfront fee to reduce their mortgage interest rate.

A few key terms can help explain the concept:

- Mortgage Point (Discount Point): An upfront fee paid to a lender in exchange for a lower interest rate.

- Rate Buydown: The process of paying points to reduce the mortgage rate and monthly payment.

- Break-Even Point: The amount of time it takes for monthly savings from a lower rate to exceed the upfront cost of purchasing points.

Whether buying points makes sense depends largely on how long a buyer expects to keep the mortgage. Buyers planning to remain in the home for many years may benefit more than someone expecting to move after only a few.

Adjustable-Rate Mortgages Aren't What They Used to Be

For many consumers, adjustable-rate mortgages, or ARMs, carry negative associations because of their role during the housing crisis nearly two decades ago.

Fleming believes today's products are often misunderstood. "This is not the ARM of the global financial crisis," he said.

Modern adjustable-rate mortgages frequently include fixed-rate periods of seven or 10 years before any adjustments occur. During that fixed period, borrowers make the same payment they would with a traditional mortgage.

Understanding a couple key terms can help:

- Adjustable-Rate Mortgage (ARM): A mortgage that begins with a fixed interest rate for a set period before potentially adjusting based on market conditions.

- Fixed Period: The initial period during which the mortgage interest rate cannot change, often seven or 10 years.

According to Fleming, many first-time buyers may not remain in the home long enough to experience the adjustment period.

"Most first-timers usually move within that seven- or 10-year window to that move-up home," he said.

That doesn't mean ARMs are appropriate for everyone. Buyers should carefully evaluate their long-term plans and understand the potential risks. However, they may offer a lower monthly payment than a traditional 30-year fixed mortgage.

Are Mortgage Rates Really High?

Many buyers continue to view today's mortgage rates as exceptionally expensive because they compare them to the pandemic years. However, this perspective can be misleading.

"You know, a 6% to 6.5% mortgage is pretty normal by historic standards," remarked Fleming.

The rates seen during 2020 and 2021 were among the lowest ever recorded. While today's borrowing costs may feel high compared to those unusual years, they remain relatively normal – or even low – when viewed over several decades of housing history.

The bigger challenge may be the combination of mortgage rates and home prices, as well as the additional costs of property taxes and homeowners insurance.

How Inflation Affects Homebuyers

Mortgage rates aren't the only economic factor affecting affordability. Fleming pointed to rising costs for necessities such as food and fuel as another challenge for prospective homeowners. When households spend more money on essentials, less money remains available for savings.

That can delay:

- Down payment accumulation

- Emergency fund savings

- Closing cost preparation

- Home maintenance reserves

Beyond the direct financial impact, inflation can also affect buyer confidence.

"The bigger [problem] is fear and uncertainty," Fleming said.

Uncertainty often causes both buyers and sellers to delay major financial decisions. As a result, housing activity slows even when economic conditions remain relatively healthy.

What Does a Balanced Housing Market Look Like?

Housing experts often talk about "balanced markets," but many buyers aren't sure what that means. According to Fleming, inventory remains one of the best ways to measure market balance.

A few important terms include:

- Months of Supply: The amount of time it would take to sell all available homes at the current pace of sales.

- Balanced Market: A market where supply and demand are roughly equal, creating stable price growth.

- House Price Appreciation: The rate at which home values increase over time.

Historically, housing economists view roughly five to six months of supply as a balanced market.

When inventory falls well below that level, prices tend to rise rapidly because buyers compete for limited homes. When inventory rises significantly above that level, price growth typically slows or reverses.

While some markets are moving closer to balanced inventory levels, Fleming noted that housing activity itself remains unusually slow because many owners still aren't selling.

The Long-Term Solution to the Housing Shortage

Many proposals have emerged for increasing housing supply, from converting vacant office buildings into apartments to redeveloping old shopping malls.

While those ideas can help, Fleming believes the biggest opportunity lies elsewhere.

"The real key is regulation and zoning," he said.

Specifically, many experts believe local governments could increase the housing supply by making it easier to build.

Potential solutions include:

- Allowing more housing construction on vacant land

- Simplifying approval processes

- Reducing zoning restrictions

- Encouraging duplexes and triplexes in single-family neighborhoods

- Supporting higher-density development near jobs and transportation

One concept gaining attention is upzoning, which allows more housing units to be built on land previously reserved for a single home.

For example, a property that currently contains one older home could potentially be redeveloped into a duplex or triplex, increasing housing supply while creating lower-cost ownership opportunities.

While zoning reform remains politically challenging in many communities, housing economists increasingly view it as one of the most effective long-term solutions to America's housing shortage.

Buy a Home When You're Ready

Despite all the discussion about mortgage rates, inventory levels, affordability, and economic uncertainty, Fleming's most important advice for buyers remains remarkably simple.

"Buy a home when you're ready."

That readiness isn't just financial.

According to Fleming, life events often play a larger role in homeownership decisions than market conditions. Marriage, children, changing family needs, and long-term lifestyle goals frequently drive the decision to buy.

Once that decision has been made, buyers can focus on finding a home that fits their budget and circumstances.

Fleming also encourages first-time buyers to avoid placing too much pressure on their first purchase. "And remember, if you're a first-time homebuyer, your first home is usually not your forever home," he said.

Many buyers become fixated on finding the perfect property. In reality, a starter home is often exactly that: a starting point. A smaller home, an older home, or a home in a less expensive neighborhood can provide an opportunity to begin building equity and participating in future home price appreciation.

The Bottom Line

Housing affordability remains a challenge across much of the country, but opportunities still exist for buyers who understand how today's market works. Inventory shortages, elevated mortgage rates, and economic uncertainty have created obstacles, particularly for first-time buyers searching for entry-level homes.

Still, buyers have more options than they may realize. New construction, mortgage points, adjustable-rate mortgages, and low-down-payment financing strategies can all help improve affordability.

Most importantly, buyers should remember that homeownership is often a long-term lifestyle decision rather than a short-term market timing exercise. As Fleming emphasized, the best time to buy is not necessarily when rates are lowest or inventory is highest. It's when your finances, goals, and life circumstances align with the responsibilities and opportunities that come with owning a home.