Adam Godby (NMLS #2286643) is a Loan Officer and Team Lead at First Residential Independent Mortgage (NMLS #1907), a Springfield, Missouri-based national lender. Equal Housing Opportunity. First Residential is a registered DBA of Mortgage Research Center, LLC, an affiliate of Three Creeks Media.

Don’t get me wrong. I like down payment assistance programs. My clients use them all the time. For some buyers, these programs make the difference between buying a house and continuing to pay rent, and that’s huge.

But many borrowers confuse down payment “grants” with down payment “loans,” and I can see why: Lots of down payment assistance programs call themselves “grants” when they’re really issuing loans that must be repaid.

Even when a down payment loan requires no monthly payments, it may still come with strings attached. These types of strings can entangle future refinances or home sales.

So, before using a down payment assistance program, buyers should understand exactly what they’re getting into.

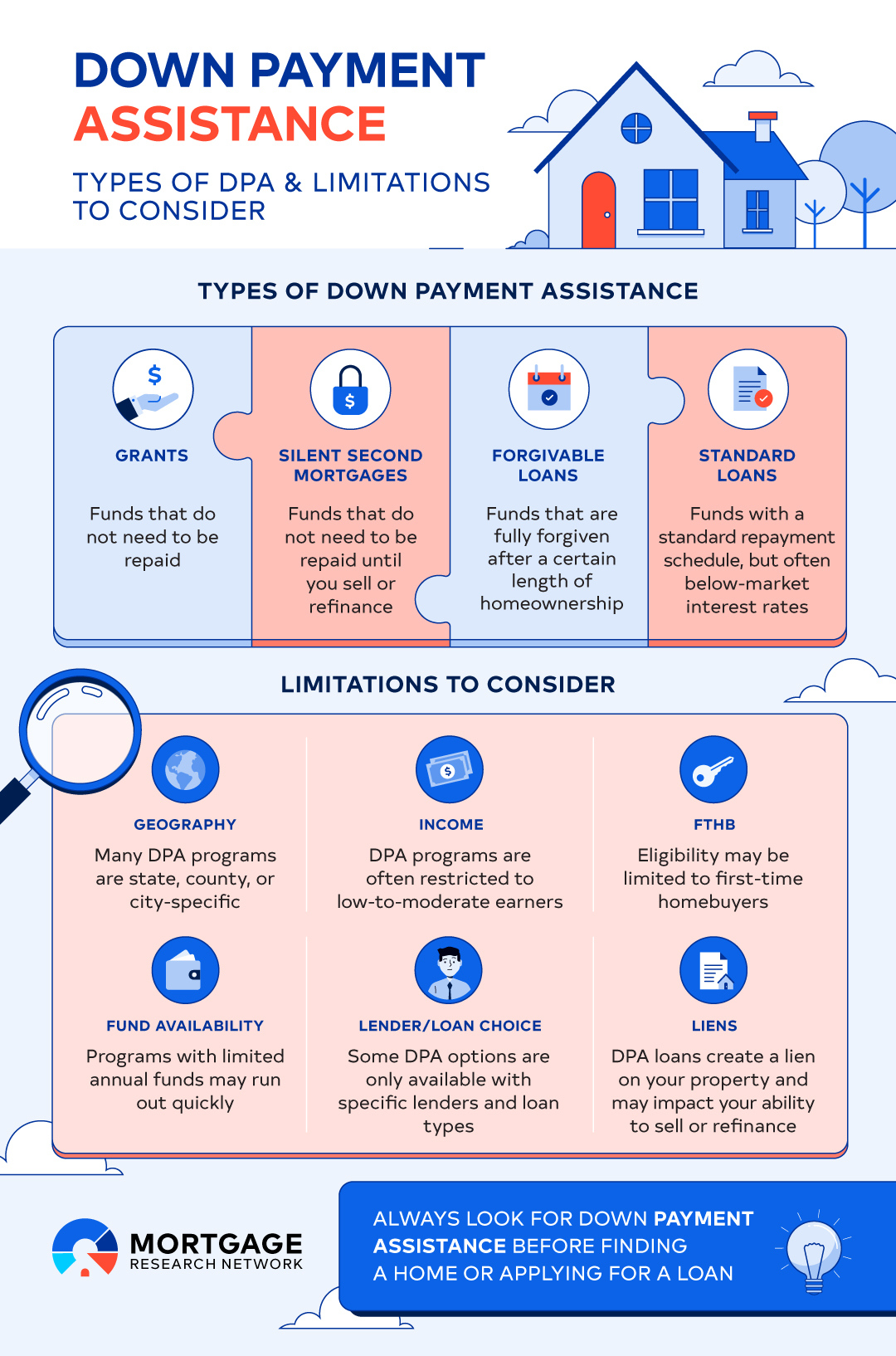

Down Payment Assistance: Is It a Grant or Is It a Loan?

Down payment assistance comes from hundreds of programs across the country. Many city and county governments run DPA programs. In some places, nonprofits, employers, or professional associations offer down payment help.

Each DPA program follows its own rules. Sometimes, the down payment help comes from:

A grant: If the DPA is a grant, the buyer won’t have to repay the money. True grants are rare. They typically go to lower-income buyers or in areas with lower housing prices. These programs tend to run out of money before the end of the year

A silent second mortgage: In these cases, the DPA is a loan that requires no monthly payments. This may seem like a grant, but the loan puts a lien on the new home that must be repaid when the homeowner sells or refinances

A forgivable loan: Some silent second mortgage balances gradually decrease on their own, even though the homeowner doesn’t make payments. Within five to 10 years, the balance can reach $0. Still, selling or refinancing before the balance is forgiven means the homeowner must repay all or part of the loan

A loan that must be repaid: Other DPA loans must be repaid by making regular payments alongside the primary mortgage payments

Any program that helps someone become a homeowner and start investing in their future instead of paying more rent is a good thing.

But buyers should learn how their DPA program works before going under contract on a home and applying for a mortgage. I’ve worked with buyers who learned they weren’t eligible for their program after going under contract. Unfortunately, they couldn’t follow through and buy the home after all.

Down Payment Assistance vs. No Money Down Loans

Before digging deeper into down payment assistance programs and how they work, I need to make a clear distinction between DPA programs and no money down loans programs.

Some buyers can get home loans that require no money down to begin with. Typically, these buyers are limited to:

Military families: The VA loan program eliminates the need for the down payment. Active duty military members, veterans, and some surviving spouses of veterans who died on active duty should look into this loan program

Rural buyers with moderate incomes: The USDA loan program also requires no money down. People with moderate income (115% of the median income in their area) who are buying homes in areas the USDA considers rural can apply.

Making no down payment is already baked into these loans so there’s typically no need for down payment help, although DPA programs can sometimes be used as closing cost assistance. Most other loans, including popular FHA and conventional loans, require out-of-pocket contribution from the buyer.

Conventional loan programs can go as low as 3 percent down. For reference, on a $250,000 home, 3 percent is $7,500. FHA loans require 3.5 percent down, which is $8,750 on a $250,000 home.

Should You Use Down Payment Assistance?

So, let’s say you want to buy a $250,000 house with an FHA loan. You’ll need to make the 3.5 percent down payment, which amounts to $8,750. If you have the money in your savings account, you’ll just need to prove that by showing your bank account statement to your loan officer or loan processor.

If you don’t have the money already saved you have three main choices:

Save the money

Ask family members to help

Use down payment assistance (DPA)

All three choices have pros and cons:

| Plan | Pros | Cons |

|---|---|---|

| Saving the money yourself | Simplicity: No need to follow down payment assistance rules when using your own money | A moving target: While you’re saving, the house will likely become more expensive, and you’ll need to save even more money |

| Getting help from family members | No repayments: There should be no need to repay a down payment gift from your family; in fact, the donor will need to state this in a letter to the lender | Could get personal: Family members who gift money may need to share their bank statements with the lender; also, not every homebuyer has family who can help |

| Getting help from a DPA program | Buying faster: You can buy sooner with less money out of pocket and without involving family or friends | Financial strings attached: Are you eligible for your local DPA program? Will it put a lien on your home? Typically there are at least some strings attached |

There’s no such thing as free money. That’s why there are cons to every scenario in the table above. In any down payment scenario, it’s the buyer’s job to learn the cons. Find out what strings are attached and how they could affect the future of the property.

How to Avoid Down Payment Assistance Surprises

I’ve worked with buyers who thought they were eligible for a DPA program but learned – after finding a home, going under contract, and applying for a mortgage – that they were not eligible for the DPA program after all.

This ended their homebuying journey. With no down payment, they couldn’t get approved for the mortgage. They had to back out of the deal, and someone else bought the house.

The surprise may come later, when the homeowner decides to sell or refinance and learns the DPA loan has to be paid off first. Paying off the DPA loan along with paying Realtor commissions, or closing costs on a refinance, can drain equity.

The best way to avoid surprises is to learn all the DPA program’s details before finding a home to buy.

Down Payment Assistance Strings: What Might Be Attached

The strings attached to down payment assistance vary from program to program. Some can be temporary; others might prevent you from using the program to begin with.

Strings include:

Geography: Typical DPA programs work only in specific areas. Sometimes, eligibility can change from neighborhood to neighborhood

Income: Many DPA programs help only buyers who earn low or moderate incomes; other programs limit grants to lower-income borrowers but offer DPA loans to higher-earning buyers

Fund availability: Programs that give grants to buyers usually have a limited amount of money to grant each year. They often run out of money before the end of the year

First-time buyer requirement: Many programs help only first-time buyers, which is usually defined as people who haven’t owned a home in the past three years

Lender and loan choice: DPA programs tend to limit which lender you can use or what type of loan you can get

Liens: Most DPA programs issue loans, not grants. Like any mortgage loan, DPA loans put a lien on the home, which means the loan balance must be repaid if you sell or refinance. (With some programs this lien gets gradually smaller each year you stay in the home)

Before you find a home and make an offer, find out how the down payment assistance program you want to use works and whether you’re eligible.

Some Lenders Offer Down Payment Assistance Programs

Some mortgage lenders, including the lender I work for, have started their own down payment assistance programs.

First Residential Mortgage, my company, has two DPA programs. One is a silent second mortgage that requires no payments and is forgivable if the buyer stays in the home for five years. The other plan requires monthly payments to pay off.

If you need help with your down payment, I recommend looking for a lender that operates its own program. One of the best things about using a lender’s DPA? You can expect the program to work with the primary mortgage you’re getting.

With my lender’s programs, if you’re eligible for the primary mortgage, you’re eligible for the DPA program. There are no geography, income, or fund availability hurdles to jump through.

I’ve had a buyer who could have afforded their own down payment, but used our DPA program because it allowed them to invest their own money elsewhere.

Know Your Program Before You Count on It

Buyers who need down payment help should absolutely look into their local DPA programs. Here’s my main piece of advice: Learn about the program before deciding to depend on it.

Too many times I’ve worked with buyers who learned that down payment assistance programs existed, decided to use one, and then started shopping for a home. They found the right home, went under contract, and then learned about their DPA’s program’s strings. Worst case scenario, they learned they didn’t qualify for the DPA program after all.

Buyers can avoid that bad outcome by asking questions upfront. Ask your loan officer, and if you’re not getting answers, find a different loan officer to ask. Sooner or later you’ll come across somebody like me who wants buyers to know all the details.