Homebuying in Today's Market: What First-Time Buyers Need to Know About Mortgage Rates, Rate Locks, and Affordability

Purchasing a home can feel overwhelming, especially for first-time buyers navigating a market that looks very different than it did just a handful of years ago. Despite retreating from their recent peak, mortgage rates remain significantly higher than the record lows seen during the pandemic. In addition, affordability challenges persist in many markets, and, in some cases, buyers may still face intense competition for desirable homes.

Yet despite those challenges, homeownership remains a realistic goal for millions of Americans.

On a recent episode of the Real Estate Update podcast, Emily Overton, Capital Markets Manager at Veterans United, discussed some of the biggest questions facing today's homebuyers, from mortgage rate locks and pre-approvals to down payment assistance and market timing. Her insights offer a useful roadmap for buyers trying to make sense of an often confusing process.

The key is understanding how the mortgage process works, what loan options are available, and how to position yourself as a strong buyer before you start house hunting.

Why Mortgage Rates Matter So Much

Prospective buyers often focus on the home's purchase price, but the mortgage rate can have just as much impact on affordability. Even a one percentage-point difference can dramatically affect a monthly mortgage payment and the total amount of interest paid over the life of the loan.

Mortgage rates are influenced by a variety of economic forces, including:

- Inflation

- Federal Reserve policy

- Employment data

- Economic growth

- Investor demand for bonds

- Global financial events

While consumers often hear about the Federal Reserve raising or lowering interest rates, mortgage rates do not move directly with Fed decisions. Instead, they tend to follow broader movements in the bond market, particularly the 10-year Treasury yield.

Overton has a front-row seat to these market movements. "Mortgage rates can actually move daily and even during the day," she said.

That volatility means a buyer shopping for a mortgage today could see pricing that's totally different tomorrow.

Today's Rates Aren't as Unusual as Many Buyers Think

One challenge facing today's buyers is perspective. Many Americans became accustomed to the exceptionally low mortgage rates available during the late 2010s and into the early part of the pandemic. As rates climbed above 7% in subsequent years, many hopeful buyers concluded that borrowing costs had become prohibitively expensive.

Overton believes those comparisons can be misleading.

"There's been a lot of sticker shock with folks from seeing the twos and threes of COVIDs to the high sevens," she said. "But historically, it's not that high."

Historically speaking, mortgage rates have often been much higher than current levels. Throughout the 1970s and 1980s, rates frequently exceeded 10%, and at times topped 15%. While today's buyers face a difficult combination of elevated rates and high home prices, it is important to recognize that the ultra-low rates of the pandemic were an exception rather than the rule.

That perspective matters because many would-be buyers remain on the sidelines waiting for rates to return to 3%. Most economists do not expect that to happen anytime soon. While rates may move lower over time, buyers who postpone their plans indefinitely could miss opportunities to build equity and benefit from future home appreciation.

Understanding Mortgage Rate Locks

One of the most important but least understood parts of the mortgage process is the rate lock. A mortgage rate lock allows borrowers to secure a specific interest rate while their loan application moves through underwriting and toward closing.

"Locking in a rate just means that you're locking in a specific interest rate with your lender for a set period of time while your loan gets finalized," Overton explained.

A few key terms can help buyers understand how rate locks work:

- Rate Lock: An agreement between a borrower and lender that secures a mortgage interest rate for a specified period during the loan process.

- Lock Period: The length of time a rate remains protected. Most purchase loans use lock periods of 30, 45, or 60 days.

- Lock Extension: An extension of the original lock period if the loan is not ready to close before the lock expires.

A rate lock offers several benefits:

- Protection against rising mortgage rates

- Greater certainty about monthly payments

- Easier budgeting during the purchase process

- Reduced financial stress before closing

Without a rate lock, borrowers remain exposed to market fluctuations until closing. If rates increase during that period, the monthly payment on the loan could also rise.

Why Closing Timelines Matter

Many first-time buyers don't realize that a rate lock comes with an expiration date.

"You always want your lock to go through close," Overton said.

If closing gets delayed beyond the lock period, borrowers may need to pay a fee to extend the lock. Delays can happen for a variety of reasons, including:

- Appraisal issues

- Title problems

- Repair negotiations

- Missing documentation

- Seller-related delays

- New construction setbacks

Because of these possibilities, buyers should work closely with their lender to choose a lock period that provides sufficient time to reach the closing table.

What Happens if Rates Fall After You Lock?

One of the most common concerns among buyers is locking a rate only to watch rates decline before closing.

"If rates go down, you're typically still locked in where you are," Overton said.

However, some lenders offer a float-down option. This feature allows borrowers to take advantage of lower rates if market conditions improve after the lock is established.

Whether a float-down is available depends on the lender. Some lenders charge a fee, while others incorporate the cost into their pricing. Buyers comparing lenders should ask whether float-down options are available and under what circumstances they can be used.

Pre-Qualification vs. Pre-Approval

Many buyers mistakenly believe pre-qualification and pre-approval mean the same thing. They do not.

According to Overton, a pre-qualification is often an initial review based largely on information provided by the borrower and a credit check. A full pre-approval involves a much deeper review of income, employment, assets, tax returns, debts, and credit history.

"We're digging into your information a little bit more, and we can give you a more realistic look at what your buying power would be," Overton said.

A simple way to think about the difference is:

- Pre-Qualification: An initial estimate of buying power based on basic financial information and a credit review. It can help buyers begin their home search, but it does not involve extensive verification of financial documents.

- Pre-Approval: A more detailed review of a borrower's finances that includes documentation such as income records, bank statements, and employment information. A pre-approval provides a more accurate picture of what a buyer can afford and typically carries more weight with sellers.

The distinction becomes especially important when buyers begin making offers. Sellers often view pre-approved buyers more favorably because much of the financial review has already been completed.

How Buyers Can Strengthen Their Position

Preparation remains one of the most effective ways to gain an edge in today's housing market. Overton recommends getting as fully approved as possible before beginning a serious home search.

Buyers can also improve their chances of a smooth transaction by:

- Gathering financial documents early

- Keeping funds for closing costs readily available

- Maintaining stable employment

- Avoiding new debt during the mortgage process

- Working with responsive lenders and real estate agents

Just as importantly, buyers should avoid major financial changes while pursuing a mortgage.

"Don't go get a new car," Overton advised.

Opening new credit accounts, financing furniture, changing jobs, or taking on additional debt can all affect mortgage qualification. Many lenders perform final checks before closing, meaning financial decisions made late in the process can still impact approval.

Understanding Closing Costs

Saving for a down payment is only part of the financial challenge. Closing costs often add thousands of dollars to the amount buyers need at settlement.

According to Overton, setting aside several thousand dollars for closing costs is a prudent strategy. In many markets, these expenses total between 2% and 5% of the home's purchase price.

Common closing costs include:

- Loan origination fees

- Appraisal fees

- Title insurance

- Recording fees

- Escrow funding

- Prepaid property taxes

- Homeowners insurance premiums

Buyers who budget only for a down payment may be surprised to learn they’ll also be responsible for these additional expenses.

Loan Programs That Can Help First-Time Buyers

Many prospective homeowners still believe they need a 20% down payment to buy a house. In reality, several mortgage programs allow qualified borrowers to purchase with far less cash upfront.

VA Loans

Overton highlighted the VA loan as one of the strongest financing options available for eligible service members and veterans.

"There is 0% down payment required," she said. "There's no mortgage insurance."

VA loans are backed by the Department of Veterans Affairs and are available to eligible veterans, active-duty service members, and certain surviving spouses.

Key benefits include:

- No down payment requirement

- No monthly mortgage insurance

- Competitive interest rates

- Flexible credit guidelines

- Limits on certain closing costs

Many eligible borrowers are unaware that they qualify for a VA loan, making it worthwhile to check eligibility with a lender before considering other options.

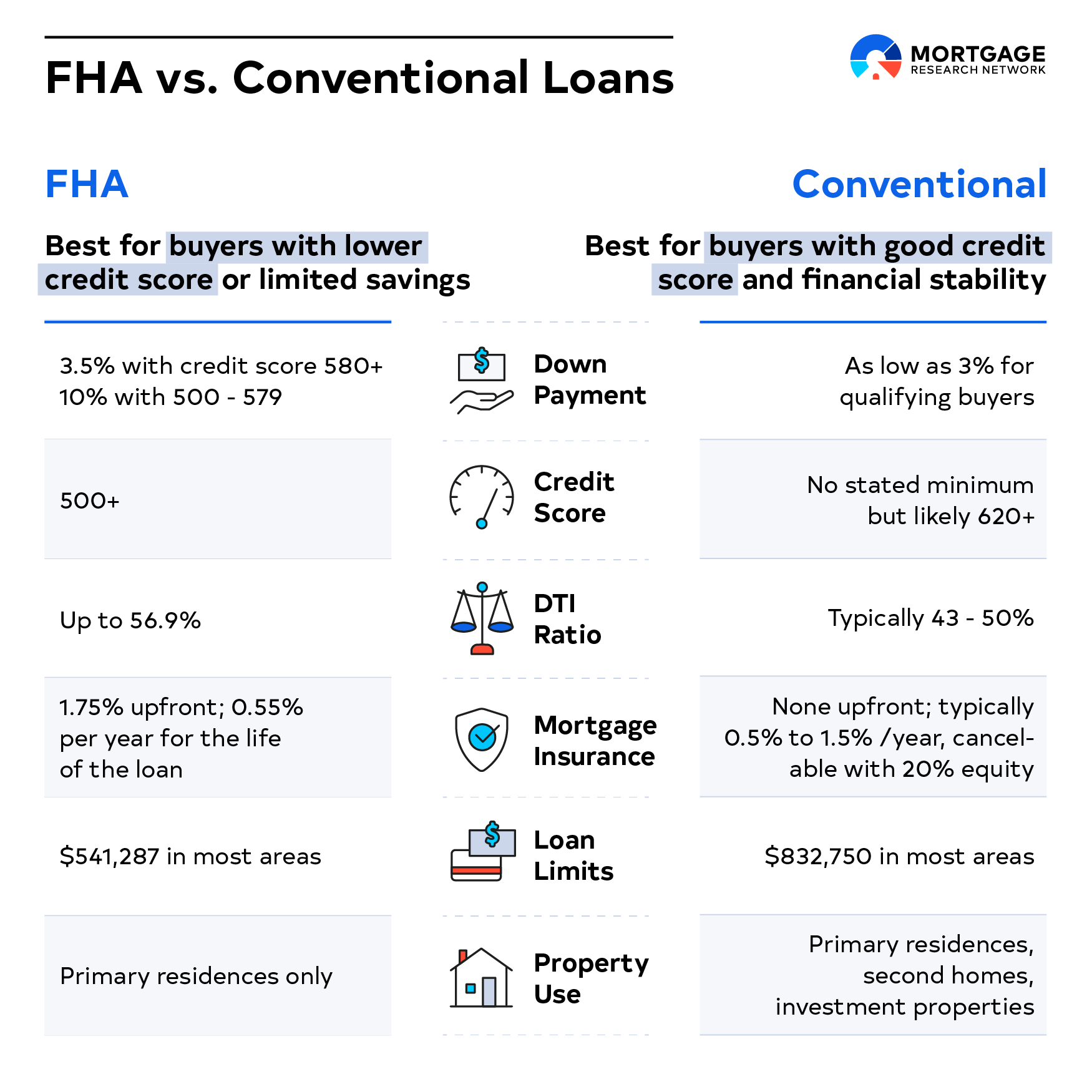

FHA Loans

For borrowers who do not qualify for VA financing, FHA loans remain a popular alternative.

Backed by the Federal Housing Administration, FHA loans were designed to help borrowers with limited savings or less-than-perfect credit.

Key benefits include:

- Down payments as low as 3.5%

- More flexible credit requirements

- Higher allowable debt-to-income ratios in some cases

- Widely available through participating lenders

While FHA loans require mortgage insurance, they continue to serve as an important entry point for first-time buyers.

Conventional 97 Loans

Conventional 97 loans offer another pathway into homeownership and can serve as a good alternative to FHA financing for buyers with stronger credit profiles.

Key benefits include:

- Just 3% down required

- Available to many first-time buyers

- Mortgage insurance can eventually be removed

- Potentially lower long-term costs than FHA loans

One of the biggest advantages is that private mortgage insurance can be canceled once the borrower reaches sufficient equity in the home.

Down Payment Assistance Programs

For many households, qualifying for a mortgage is not the primary obstacle. Saving enough money for a down payment and closing costs is often the bigger challenge.

"Down payment assistance programs can be layered on top of different types of loans," Overton said.

Depending on the program, assistance may come in the form of:

- Grants

- Forgivable loans

- Deferred-payment loans

- Lower-interest loans

Thousands of these down payment assistance programs exist nationwide through state housing agencies, local governments, nonprofits, employers, and community development organizations. Buyers are commonly surprised to learn they qualify for assistance.

Should You Wait for Rates to Fall?

Many prospective buyers continue to delay their home search while hoping mortgage rates will decline significantly.

"If you're trying to time the market, I wouldn't recommend it," Overton said.

Instead of trying to predict future mortgage rates, buyers should focus on factors they can control, including:

- Income stability

- Credit health

- Savings

- Debt management

Overton encourages buyers to ask themselves a few fundamental questions: "Do you have stable income? Do you think you'll stay in your home for a few years? And can you comfortably afford a payment for the houses that you're looking at?"

Those answers are likely to have a much greater impact on long-term financial success than any short-term prediction about where mortgage rates may go next.

The Bottom Line

Affordability challenges remain real, and first-time buyers face obstacles that previous generations may not have encountered. Yet numerous tools and programs exist to help make homeownership more attainable.

Understanding concepts such as rate locks, pre-approvals, closing costs, and low-down-payment loan programs can help buyers make more informed decisions and avoid common mistakes. While Overton highlighted certain aspects of the homebuying and borrowing process, there’s a broader lesson for any prospective homeowner: focus on your financial readiness rather than trying to predict the housing market perfectly.

For buyers with a stable income, realistic expectations, and a long-term plan, homeownership can still be a smart financial move, regardless of where mortgage rates are this month.