You might be surprised that the U.S. Department of Agriculture (USDA) does more than watch over the country’s crops and certify the slab of beef you’ll have for dinner.

Few know that the agency also has its own mortgage program. USDA-backed loans are designed for borrowers with low-to-moderate income and are meant to spur economic development in rural communities.

The best part? These home loans come with an option for 0% down payment.

However, you’ll have to meet the qualifications, which include buying a property within designated rural areas and meeting local income limits.

USDA mortgages increased 6.5% annually in 2025 — nearly six times the growth rate of overall purchase volume. Although the USDA mortgage share held at 1.2% of total originations for the second straight year, these loans could gain traction in 2026 and beyond. Falling affordability is pushing more people to explore options requiring less money upfront.

However, USDA loans face serious headwinds. Income limits have not kept up with rising home prices, mortgage rates, taxes, and insurance. Since 2022, fewer people who meet income limits can qualify for monthly payments.

| Year | USDA Purchase Originations | YoY | USDA Share of Overall Originations |

|---|---|---|---|

| 2025 | 38,409 | 6.50% | 1.20% |

| 2024 | 36,051 | 2.60% | 1.20% |

| 2023 | 35,135 | -37.10% | 1.10% |

| 2022 | 55,821 | -47.50% | 1.50% |

| 2021 | 106,374 | -15.20% | 2.30% |

| 2020 | 125,437 | 26.60% | 2.90% |

| 2019 | 99,112 | -3.50% | 2.50% |

| 2018 | 102,655 | 2.70% |

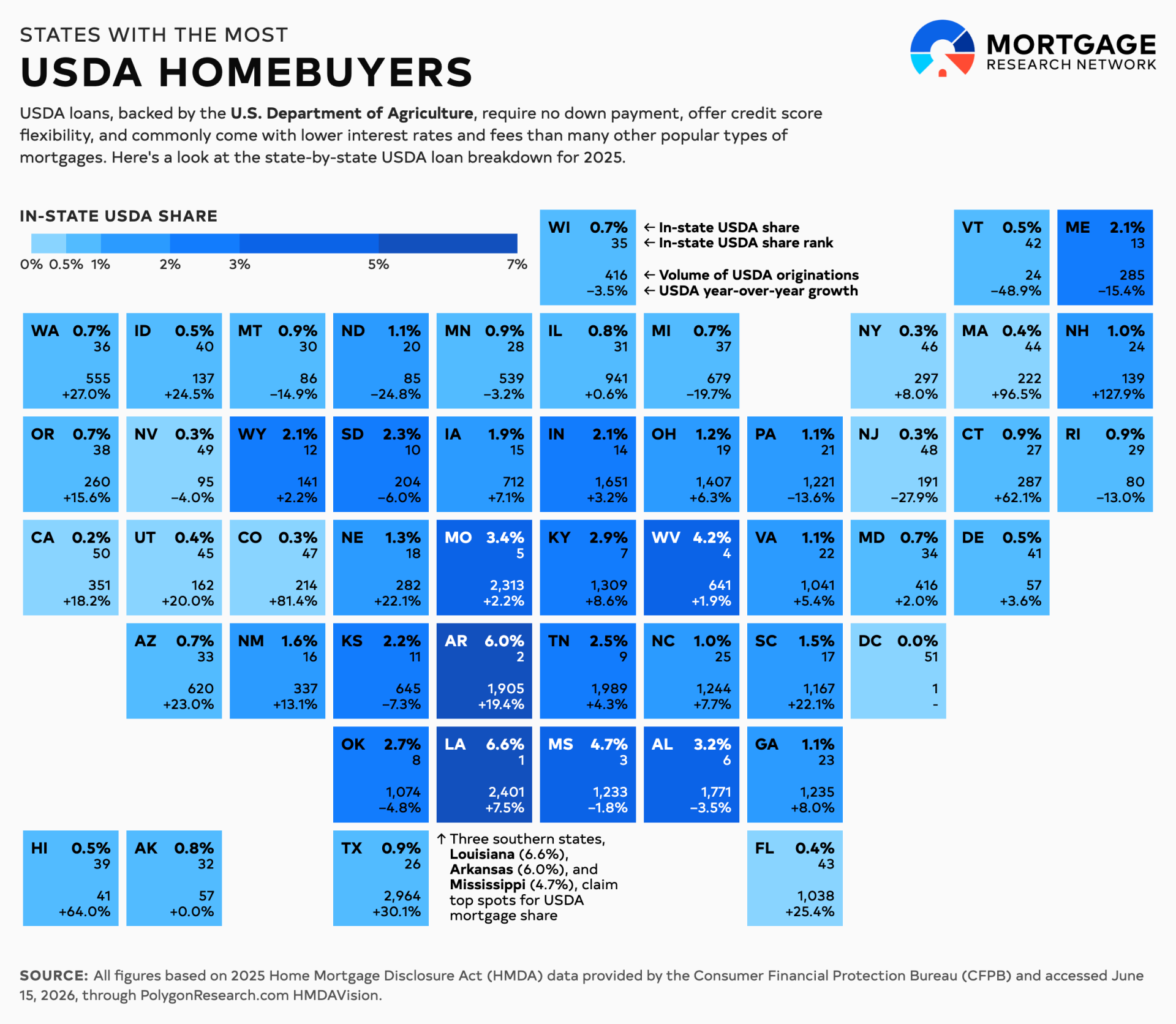

USDA Mortgages by State

Mortgages insured by the United States Department of Agriculture (USDA) are reserved for borrowers making less than 115% of their local median income. USDA loans are strictly for primary residences within allowed geographic areas.

Because of these parameters, USDA loans are always the least-used major loan type. Mortgage market share shakes out as follows.

Conventional: 68%

FHA: 20.3%

VA: 10.5%

USDA: 1.2%

However, USDA loans experienced the largest growth of any major loan type, at 6.5%, compared to yearly changes of -0.6% for conventional, 4.8% for FHA, and 5.5% for VA.

To find where USDA loans are most common, Mortgage Research Network analyzed the latest Home Mortgage Disclosure Act (HMDA) data for 2025 using Polygon Research's HMDAVision. A total of 819 lenders originated 38,409 owner-occupied USDA purchase mortgages on 1–4 unit properties. Applicants had a median income of $76,000.

Three southern states claim top spots for USDA mortgage share.

Louisiana: 6.6% USDA loan share

Arkansas: 6%

Mississippi: 4.7%

By year-over-year USDA volume growth, New Hampshire saw the biggest jump at 127.9%. Next came 96.5% in Massachusetts, 81.4% in Colorado, 64% in Hawaii, and 62.1% in Connecticut.

The table below shows USDA purchase origination data by state, ranked by in-state USDA-share, based on 2025 HMDA data.

| Rank | State | In-State USDA Share | USDA Originations | USDA YoY | Share of Total U.S. USDA Volume |

|---|---|---|---|---|---|

| 1 | Louisiana | 6.60% | 2,401 | 7.50% | 6.30% |

| 2 | Arkansas | 6.00% | 1,905 | 19.40% | 5.00% |

| 3 | Mississippi | 4.70% | 1,233 | -1.80% | 3.20% |

| 4 | West Virginia | 4.20% | 641 | 1.90% | 1.70% |

| 5 | Missouri | 3.40% | 2,313 | 2.20% | 6.00% |

| 6 | Alabama | 3.20% | 1,771 | -3.50% | 4.60% |

| 7 | Kentucky | 2.90% | 1,309 | 8.60% | 3.40% |

| 8 | Oklahoma | 2.70% | 1,074 | -4.80% | 2.80% |

| 9 | Tennessee | 2.50% | 1,989 | 4.30% | 5.20% |

| 10 | South Dakota | 2.30% | 204 | -6.00% | 0.50% |

| 11 | Kansas | 2.20% | 645 | -7.30% | 1.70% |

| 12 | Wyoming | 2.10% | 141 | 2.20% | 0.40% |

| 13 | Maine | 2.10% | 285 | -15.40% | 0.70% |

| 14 | Indiana | 2.10% | 1,651 | 3.20% | 4.30% |

| 15 | Iowa | 1.90% | 712 | 7.10% | 1.90% |

| 16 | New Mexico | 1.60% | 337 | 13.10% | 0.90% |

| 17 | South Carolina | 1.50% | 1,167 | 22.10% | 3.00% |

| 18 | Nebraska | 1.30% | 282 | 22.10% | 0.70% |

| 19 | Ohio | 1.20% | 1,407 | 6.30% | 3.70% |

| 20 | North Dakota | 1.10% | 85 | -24.80% | 0.20% |

| 21 | Pennsylvania | 1.10% | 1,221 | -13.60% | 3.20% |

| 22 | Virginia | 1.10% | 1,041 | 5.40% | 2.70% |

| 23 | Georgia | 1.10% | 1,235 | 8.00% | 3.20% |

| 24 | New Hampshire | 1.00% | 139 | 127.90% | 0.40% |

| 25 | North Carolina | 1.00% | 1,244 | 7.70% | 3.20% |

| 26 | Texas | 0.90% | 2,964 | 30.10% | 7.70% |

| 27 | Connecticut | 0.90% | 287 | 62.10% | 0.70% |

| 28 | Minnesota | 0.90% | 539 | -3.20% | 1.40% |

| 29 | Rhode Island | 0.90% | 80 | -13.00% | 0.20% |

| 30 | Montana | 0.90% | 86 | -14.90% | 0.20% |

| 31 | Illinois | 0.80% | 941 | 0.60% | 2.40% |

| 32 | Alaska | 0.80% | 57 | 0.00% | 0.10% |

| 33 | Arizona | 0.70% | 620 | 23.00% | 1.60% |

| 34 | Maryland | 0.70% | 416 | 2.00% | 1.10% |

| 35 | Wisconsin | 0.70% | 416 | -3.50% | 1.10% |

| 36 | Washington | 0.70% | 555 | 27.00% | 1.40% |

| 37 | Michigan | 0.70% | 679 | -19.70% | 1.80% |

| 38 | Oregon | 0.70% | 260 | 15.60% | 0.70% |

| 39 | Hawaii | 0.50% | 41 | 64.00% | 0.10% |

| 40 | Idaho | 0.50% | 137 | 24.50% | 0.40% |

| 41 | Delaware | 0.50% | 57 | 3.60% | 0.10% |

| 42 | Vermont | 0.50% | 24 | -48.90% | 0.10% |

| 43 | Florida | 0.40% | 1,038 | 25.40% | 2.70% |

| 44 | Massachusetts | 0.40% | 222 | 96.50% | 0.60% |

| 45 | Utah | 0.40% | 162 | 20.00% | 0.40% |

| 46 | New York | 0.30% | 297 | 8.00% | 0.80% |

| 47 | Colorado | 0.30% | 214 | 81.40% | 0.60% |

| 48 | New Jersey | 0.30% | 191 | -27.90% | 0.50% |

| 49 | Nevada | 0.30% | 95 | -4.00% | 0.20% |

| 50 | California | 0.20% | 351 | 18.20% | 0.90% |

| 51 | District of Columbia | 0.00% | 1 | - | 0.00% |

Applying for a USDA Loan

Not all lenders offer USDA mortgages, so you’ll first need to find one that does (and one with lots of experience could prove beneficial).

“USDA is the one loan program where lender experience can be the difference between closing on time and watching your deal fall apart,” said Ashley Harris, director of homebuyer education at Neighbors Bank.

“Every USDA file goes through two separate approvals. The lender underwrites it first, then USDA’s own Rural Development office must independently review and issue a conditional commitment before you can close. That second review doesn’t forgive mistakes. A lender who closes USDA loans every week knows what Rural Development in your specific state is looking for, what documentation they want to see upfront, what the current turn times are, and how to structure a file that sails through both approvals the first time.”

Neighbors Bank (NMLS #491986) is a Columbia, Missouri-based national lender. Equal Housing Opportunity. Neighbors Bank is an affiliate of Three Creeks Media, which operates this website.

USDA loans can offer a less expensive avenue toward homeownership, with no down payment, more affordable upfront and monthly mortgage insurance than FHA, and lower average interest rates compared to conventional home loans — a difference of 55 basis points for 30-year fixed-rate mortgages, as of June 30, 2026. They also come with no credit score threshold to clear, though most lenders will have their own underwriting standards to meet.

To be eligible to qualify for a USDA mortgage, you’ll need to meet the following:

Household income below 115% of the local median

A debt-to-income (DTI) ratio under 41%

Purchasing a primary residence

The property must be located in an eligible rural or suburban area

It should be noted that while USDA-backed loans have the option of a 0% down payment, they do come with an upfront guarantee fee and an annual fee.

See MRN’s full breakdown of USDA mortgages for more information.

Find The Right USDA Lender

Because USDA loans occupy a smaller corner of the lending market and aren’t available everywhere, a qualified lender may be harder to find.

Starting your search with the highest volume USDA lenders could help you find one with plenty of experience in your vicinity. Shopping for quotes with multiple lenders is another proven strategy that provides you the leverage to negotiate a lower mortgage rate.

If you’re ready to begin, speak with a local USDA lender today.

All figures based on 2025 Home Mortgage Disclosure Act (HMDA) data provided by the Consumer Financial Protection Bureau (CFPB) and accessed June 15, 2026, through PolygonResearch.com HMDAVision.