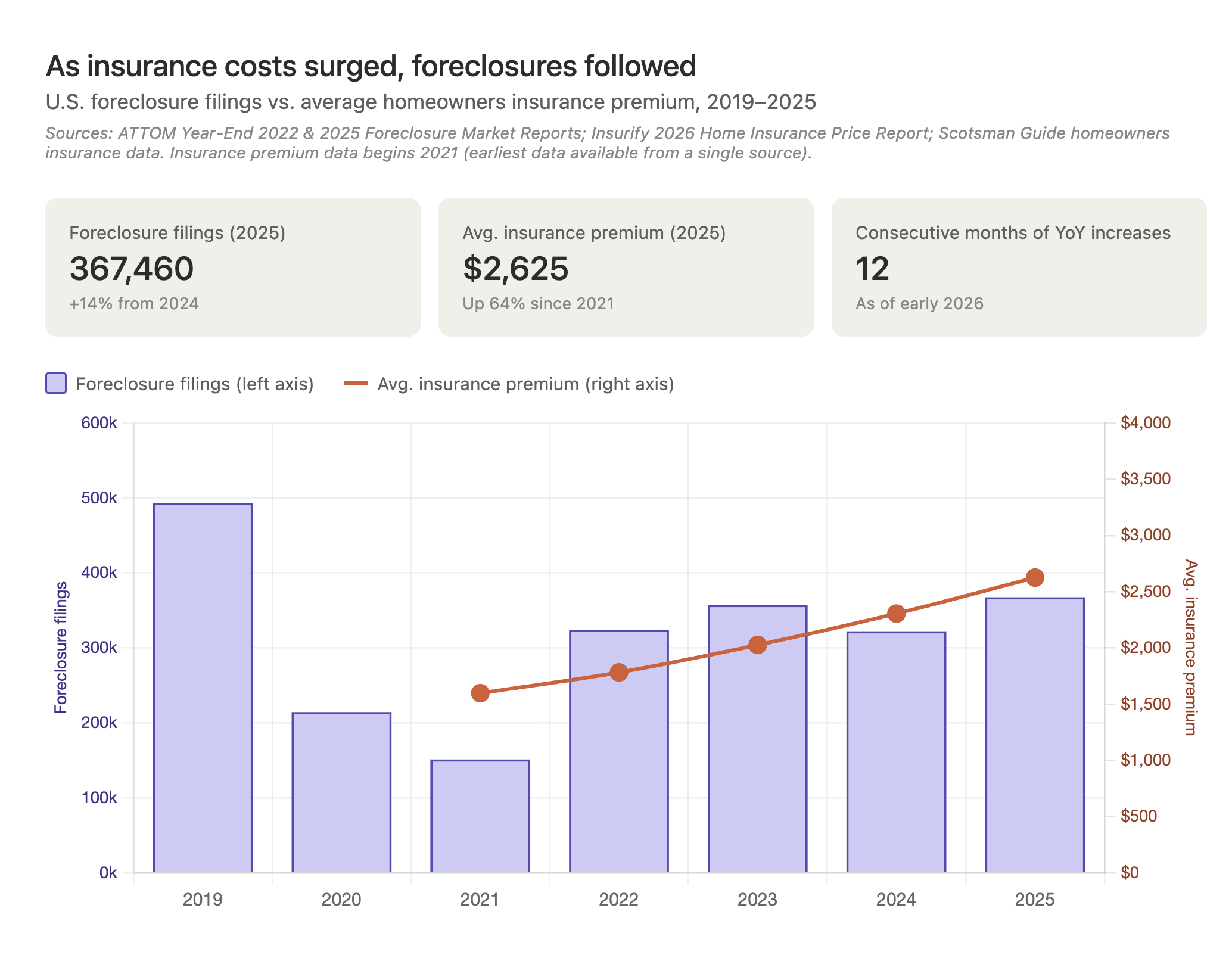

Foreclosure filings climbed to 367,460 properties in 2025 — up 14% from the year before and the highest level in six years, according to ATTOM. A number like that usually signals one thing: people who borrowed more than they could afford.

But that's not what's happening this time.

The homeowners losing their homes in 2026 often have low, fixed mortgage rates locked in during the pandemic. The culprit isn't their loan. It's everything that comes with it.

By the numbers

367,460 U.S. properties had foreclosure filings in 2025 — up 14% from 2024

Q1 2026 filings were up 26% year-over-year — the pace is accelerating

12 consecutive months of year-over-year foreclosure increases as of early 2026

Foreclosures are still down 25% from 2019 pre-pandemic levels — but the trend line is pointing sharply upward

It's not the mortgage — it's everything else

Here's what's actually squeezing homeowners out of their homes:

Homeowners insurance

The average annual premium hit $2,625 in 2025, up from $1,597 in 2021 — a 64% increase in four years

Premiums rose 7.4% in 2021, 11.6% in 2022, 13.7% in 2023, 13.8% in 2024, and are projected to climb another 4% in 2026

In high-risk states like Florida, Louisiana, and California, premiums are far higher — Florida homeowners pay 181% above the national average

Property taxes

The average annual property tax bill reached $4,427 in 2024, up 3% in a single year

Since 2019, property tax burdens have risen in nearly every county in the country

HOA fees

Average HOA fees have jumped 25–40% since 2020 in many metro areas

Condo owners face the steepest increases, with some Florida buildings issuing six-figure special assessments tied to post-Surfside reserve mandates

Together, these costs can add $500 to $1,000 per month on top of a mortgage payment — turning an affordable home into an unaffordable one.

Who's getting hit hardest

The states with the worst foreclosure rates in 2025, per ATTOM:

Florida — 1 in every 230 housing units with a filing

Delaware — 1 in every 240 units

South Carolina — 1 in every 242 units

Illinois — 1 in every 248 units

Nevada — 1 in every 248 units

Florida's prominence on this list is no coincidence — it's ground zero for the insurance crisis, with premiums running far above the national average and condo reserve mandates adding a new layer of financial pressure.

What this means if you own a home

If you're a current homeowner, the most important thing you can do right now is audit the total cost of your homeownership — not just your mortgage payment.

Check your insurance renewal carefully. Many homeowners are seeing 20–30% increases on renewal without realizing it.

Watch your escrow account. Most lenders collect insurance and taxes through escrow and adjust payments annually. A large escrow shortfall can mean a sudden jump in your monthly payment.

Don't assume equity protects you. Foreclosure proceedings can begin even when a home has significant equity — it's about cash flow, not net worth.

What this means if you're buying

If you're shopping for a home, the sticker price is only part of the math.

Always get an insurance quote before making an offer — especially in coastal, wildfire-prone, or flood-risk areas. Rates can vary dramatically by zip code.

Ask about HOA financials. Request reserve fund statements and look for deferred maintenance — a building with a depleted reserve is a liability you're inheriting.

Factor property taxes into your monthly budget, not just closing cost estimates. Use the current assessed value, not the seller's tax bill, since reassessments often follow a sale.

The bottom line

The foreclosure story of 2026 isn't about reckless borrowing. It's about the rising cost of staying put — and it's a warning sign for millions of homeowners who feel financially secure because their mortgage rate is low.