Buyers can make a down payment of 0-20% or more. How much they choose depends on their financial profile, long-term goals, tolerance for risk, and more.

Adam Godby (NMLS #2286643) is a Loan Officer and Team Lead at First Residential Independent Mortgage (NMLS #1907), a Springfield, Missouri-based national lender. Equal Housing Opportunity. First Residential is a registered DBA of Mortgage Research Center, LLC, an affiliate of Three Creeks Media.

The first time I tried to buy a home, I walked into the name-brand bank in my neighborhood and said, “I’d like to buy a home, please.”

The loan officer ran some numbers. Then he looked up from his screen, and said, “Sorry. You don’t qualify.” He didn’t say why I didn’t qualify or what I could do to improve my chances.

I walked out of the bank thinking the world was divided into two types of people: Those who can buy a home and those who can’t.

Fortunately, this isn’t true. Most people can buy a home if they can make a mortgage loan’s minimum payment and meet the loan’s minimum credit score — and if the new loan’s payments fit their monthly budget.

It does help to learn how mortgages work first. As a loan officer, I make sure my clients understand the nuances of mortgage borrowing, including the way down payments work.

First, Let’s Do the Down Payment Math

Lots of new mortgage borrowers know about down payment percentages. They know they’ll need to put 3.5 percent down on their FHA loan, for example. But they don’t always know what this means in dollars.

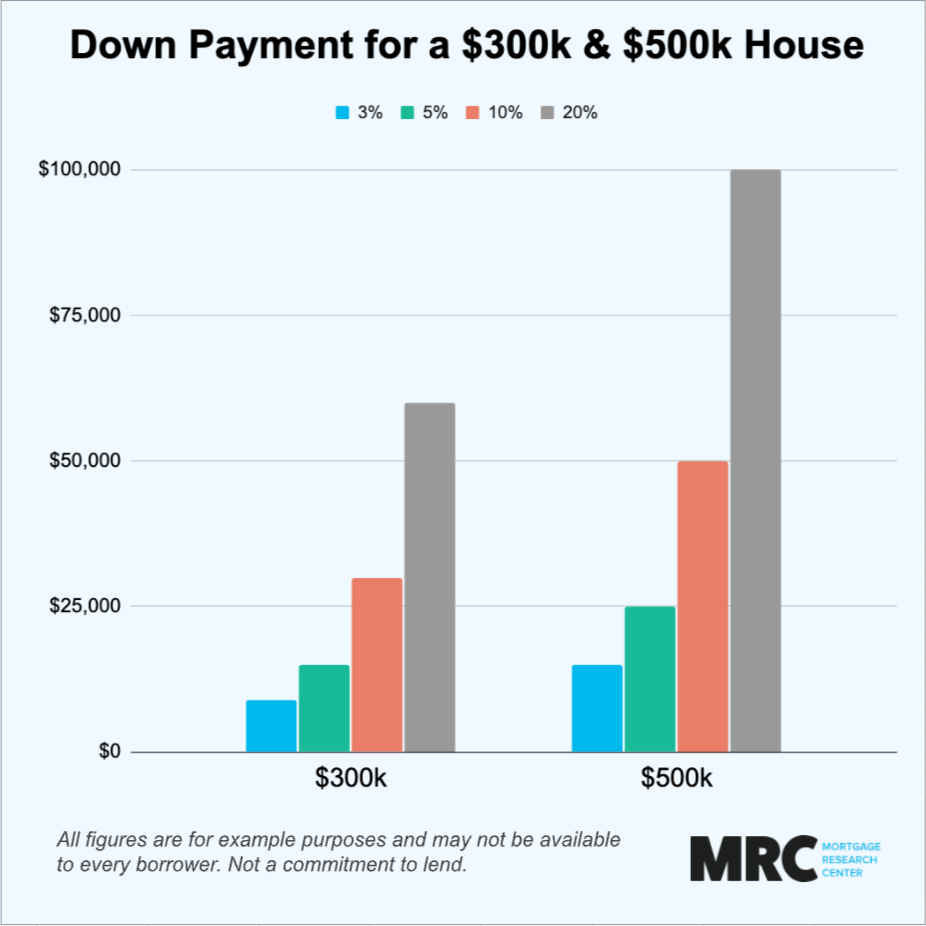

| Home Price | Desired Down Payment | Multiply By | Result |

|---|---|---|---|

| $300,000 | 3.5% | 0.035 | $10,500 |

| $300,000 | 3% | 0.03 | $9,000 |

| $300,000 | 5% | 0.05 | $15,000 |

| $300,000 | 10% | 0.10 | $30,000 |

| $300,000 | 20% | 0.20 | $60,000 |

To get the dollar amount for a 3.5 percent down payment, you multiply the home’s purchase price by 0.035. For a $300,000 house, multiply $300,000 by 0.035 to get $10,500. That’s the down payment needed to close an FHA loan on a $300,000 house.

For a 3 percent down payment, multiply the home price by 0.03 ($9,000); for 10 percent down, use 0.10 ($30,000). And so on.

Not everything about down payments is this simple. For example, should you pay the minimum down or try to save longer for a bigger down payment? Do you have to come up with the cash by yourself? I’ll answer these and some other questions below.

Common Down Payment Amounts

The National Association of Realtors says the median down payment size in 2024 was 15 percent, but most first-time home buyers I work with don’t pay this much. They use FHA loans to buy their homes, and FHA loans require only 3.5 percent down.

Conventional loan programs for first-time buyers may need only 3 percent down. For a $300,000 home, paying 3 percent down instead of 3.5 percent down saves $1,500.

That’s true on paper, but in reality, to get approved with only 3 percent down, the buyer would need a credit score above 700. Maybe even 720 or higher. With a credit score in the mid-600s, for example, the borrower might need a double-digit down payment to get a conventional loan.

I recently worked with a client whose credit score was just over 620. This client had to put 40 percent down to get approved for a conventional loan.

Let’s do that down payment math: Multiply 0.4 times the home purchase price. For a $300,000 home, that’s a $120,000 down payment!

For the same home, first-time buyers with credit scores as low as 580 can still put 3.5 percent down on an FHA loan. That’s what most of my clients do.

How Much Should a First-Time Buyer Put Down? 3 Tips

Articles online like to inform borrowers they won’t need 20 percent down to buy a house. And this is true. What’s not true is that everyone thinks they need 20 percent down. Nobody really comes in thinking this.

First-time buyers usually know they can put a lot less down. We can even help some buyers pay nothing down on a USDA loan.

Now, whether you should pay more than the minimum amount down? That depends on why you’re buying the home.

1. What is Your Home Buying ‘Why?’

Typical first-time home shoppers are buying a home because they — wait for it — need to buy a home. It’s not an investment strategy or get-rich-quick scheme.

They have a baby on the way and need more space, or their landlord is selling and they’re having to move out, or they’re living in their parents basement and have had about enough of that.

They need a home, so they’re not thinking too much about interest rates or property tax rates or homeowners insurance premiums. Ordinarily, for these buyers, this means putting down the minimum down payment.

That means paying 3.5 percent down for FHA. Or it could mean putting 3 percent or 5 percent down on a conventional loan.

2. What About Buyers Who Can Pay More Down?

If a buyer can wait — and wants to wait — until they’ve saved a bigger down payment, this does introduce some advantages.

The most obvious advantage: Paying more down means you can borrow less. A $300,000 house with 3.5 percent ($10,500) down needs a mortgage of $289,500. The same $300,000 house with 10 percent down ($30,000) needs a mortgage of only $270,000.

Larger down payments can lead to a slight discount in the loan’s interest rate which saves some money long-term and may make it easier to get approved. When people put 20 percent down on a conventional loan they don’t have to pay for private mortgage insurance (PMI), and this could save a couple hundred dollars a month.

3. Sellers Might Influence Your Down Payment Decision

The FHA loan appraisal, which makes sure the new home is safe and stable, is stricter than the conventional loan appraisal. Sometimes this makes the closing process take a little longer because somebody has to go out to paint or cover exposed wood on the exterior of the home.

Some sellers think this is too much hassle and don’t want to work with buyers who need to use an FHA loan. This happened with one of my clients recently. The client needed an FHA loan but the seller wouldn’t go under contract unless the buyer used a conventional loan.

The conventional loan, of course, was going to require a bigger down payment which the buyer couldn’t afford. So the buyer had to decide whether to find a different house or try to come up with more money down.

Percentage vs Dollar Amount

Most of my clients know what percentage down payment they need to make.

Down Payment Tip

It’s better to think of down payment in terms of percentages instead of dollar amounts. Lending guidelines often favor the next tier, say 10 percent instead of five percent. But there isn’t much benefit to putting seven percent down rather than five.

My clients don’t always know how much cash they’ll need to match that percentage.

Sometimes learning this number can change their plans.

I start by asking for the maximum house payment the buyer can afford each month. I also ask how much money they have saved.

Some clients are reluctant to share how much they can afford, but I’m not selling them a home or benefiting from how much they spend or don’t spend. I’m helping them buy a home. I can help a lot more when I know their real facts.

Paying more down can lead to a slight discount in the loan’s interest rate, but there’s more to consider.

It’s Never One-Size-Fits-All Answer

Even buyers who have saved lots of cash for a down payment might want to hold some money back to pay their closing costs or to use as an emergency fund in case they need to make a big repair or lose a job after buying the home.

Oddly enough, some buyers can save more by putting less down. Let’s say someone has saved for a 20 percent down payment. They may want to put 15 percent down instead of the full 20 percent down.

Yes, this buyer now has to get PMI, but PMI can lower a loan’s interest rate because loans with PMI are less risky in the eyes of lenders than loans without PMI. That’s because PMI pays the lender if the borrower defaults. Some of the loan’s risk is moved off the lender to the PMI company.

After closing on the home and moving in, the buyer can pay down the principal enough to cancel PMI, usually after six months.

Mortgages are complicated. Every buyer is different, so any good loan officer will ask questions to find out the buyer’s immediate needs, long-term goals, and monthly budget. Needs, goals, and resources — this is what will answer how much the buyer should pay down on the new home.

Other Homebuying Costs to Consider

Lots of first-time buyers don’t know they’ll have to pay closing costs, too. These costs cover the professional services required to become an official homeowner. They can cost as much, or more, than the home’s down payment.

Buyers can ask the home’s seller to help with this huge expense, but they need to ask for help before going under contract to buy the home. That way they can negotiate this help with closing costs into the home price.

For example, they can offer to pay a little more for the house in exchange for help from the seller with upfront closing costs. There is a limit to this strategy: The home’s purchase price still can’t exceed the appraised value of the new home.

About 80 percent of the first-time buyers I work with get closing cost help from the seller, so it’s definitely worth asking about.

Monthly costs can surprise buyers, too

Many buyers also don’t know they’ll be paying for mortgage insurance each month. For most FHA loans this adds 0.55 percent to the loan’s cost each year. Conventional loans require PMI which can cost even more.

(PMI can be canceled later but FHA mortgage insurance can’t unless the buyer puts 10 percent or more down.)

Then there’s homeowners insurance and property taxes. Mortgage lenders add these costs to the loan’s monthly payment. This extra part of the payment goes into an escrow fund. Then, at the end of the year, the money saved up in escrow pays for the annual tax bill and insurance coverage.

How much are taxes and insurance? They vary a lot by location and home value and insurance company. But these costs have to be factored into what the buyer can afford each month.

Even if the lender didn’t collect these fees from the borrower in monthly installments, the borrower would have to come up with the money — usually thousands of dollars — to pay the annual tax and insurance bills. But to make things simpler and more streamlined for the borrower, they usually require one-twelfth of the annual cost with each mortgage payment.

An escrow fund saves the borrower from remembering to make annual or bi-annual payments to their local tax collecting authority and homeowners insurance company.

Pros and Cons of a Smaller Down Payment

The biggest pro of a smaller down payment: You can buy a home now instead of waiting for years while you save a lot more money. By the way, while you save, home prices will probably be getting more expensive. So by the time you get a bigger down payment saved, you’ll need even more money to put down.

The biggest con of a smaller down payment: You’ll have to borrow more of the home’s price. From the lender’s point of view, borrowing more increases your loan-to-value ratio, or LTV. Small down payments mean higher LTVs, and higher LTVs are riskier for lenders. Higher risk increases interest rates.

But, once again, FHA exists to help buyers solve this problem. FHA helps buyers make smaller down payments without exposing the lender to a higher risk.

Down Payment Sources

A lot of first-time buyers I work with get help from their parents or other relatives to make their down payments. To make this work, the person who gives the money writes a letter saying they’re not requiring the home buyer to repay the money.

Gifts work best when the donor pays the title company at closing rather than giving the money to the home buyer. If the donor gives the money to the home buyer, I have to ask for bank statements from the donor to trace the money trail. A lot of donors don’t like having to share their bank statements.

As a buyer, you’ll have to share two months of bank statements. This is how we make sure buyers can afford to make the down payment and monthly payments going forward.

Some borrowers who are short on cash can use local assistance programs to help with their down payments or closing costs. But this isn’t always the best idea. Most of these loan-for-down-payment plans put a second lien on the home.

This means the loans will have to be repaid if you sell or refinance the home. Sometimes the lien lasts only five years but I have seen them that last all 30 years of the mortgage.

Summing It All Up

Saving up a down payment (and the closing costs) presents the biggest obstacle for many first-time buyers.

I suggest keeping it simple. Find a loan officer who will listen to you and help guide you through the borrowing process. Be transparent about your finances. The loan officer needs to know about your financial life in order to find the best loan for you. That's just another reason why choosing the right mortgage lender is so important.

And if a lender says no and won’t explain why, ask a different lender for an opinion. That’s what I did. I found a great loan officer, bought my first home, and now I enjoy helping others do the same.