You may qualify as a "first-time homebuyer" even if you've owned a home before, as long as you haven't owned a primary residence in the past three years.

Buying a home can feel like an impossible dream in today’s tough market, but you might be surprised that you qualify for first-time homebuyer programs — even if you’ve previously owned a home.

With exclusive loan programs offering lower down payments, down payment help and specialized support, these loans are designed to help more Americans achieve their homeownership goals. The key is understanding what “first-time homebuyer” means. The definition could be broader than you think.

Who Qualifies as a First-Time Homebuyer?

Being a first-time homebuyer means that you haven’t owned a primary residence in the last three years, according to lending rules from agencies like Fannie Mae.

This three-year rule means you could qualify for first-time buyer programs several times throughout your life, as long as you meet that prerequisite. Whether you’ve never owned a home or sold your last property more than three years ago, you’re eligible for most of the same programs and assistance.

Others who may qualify as first-time buyers:

Each program is different, but the following individuals may also qualify for certain programs:

A displaced homemaker or single parent, even if they jointly owned a home with their spouse in the last three years.

Those who owned a mobile home not attached to a permanent foundation.

Those who have owned a home that can’t be brought up to local building codes.

First-generation homebuyers

First-generation buyers are first-timer buyers who are also the first to do so in their families. These buyers face some barriers to getting guidance on homeownership because they don’t have family members who’ve done it and can advise them.

Benefits of Being a First-Time Homebuyer

While being a first-timer to the homeownership game can be scary, it also unlocks access to helpful advantages that help you bridge the gap between renting and ownership.

According to the National Association of Realtors, first-time buyers comprised 32% of all homebuyers in 2023, up from 26% in 2022. However, this share dropped to a historic low of 24% due to affordability pressures. What’s more is that first-time buyers put a median down payment of just 9%, NAR reported.

“The U.S. housing market is split into two groups: first-time buyers struggling to enter the market and current homeowners buying with cash,” said Jessica Lautz, NAR deputy chief economist and vice president of research, in a recent news release. “First-time buyers face high home prices, high mortgage interest rates and limited inventory, making them a decade older with significantly higher incomes than previous generations of buyers. Meanwhile, current homeowners can more easily make housing trades using built-up housing equity for cash purchases or large down payments on dream homes.”

First-time ownership benefits

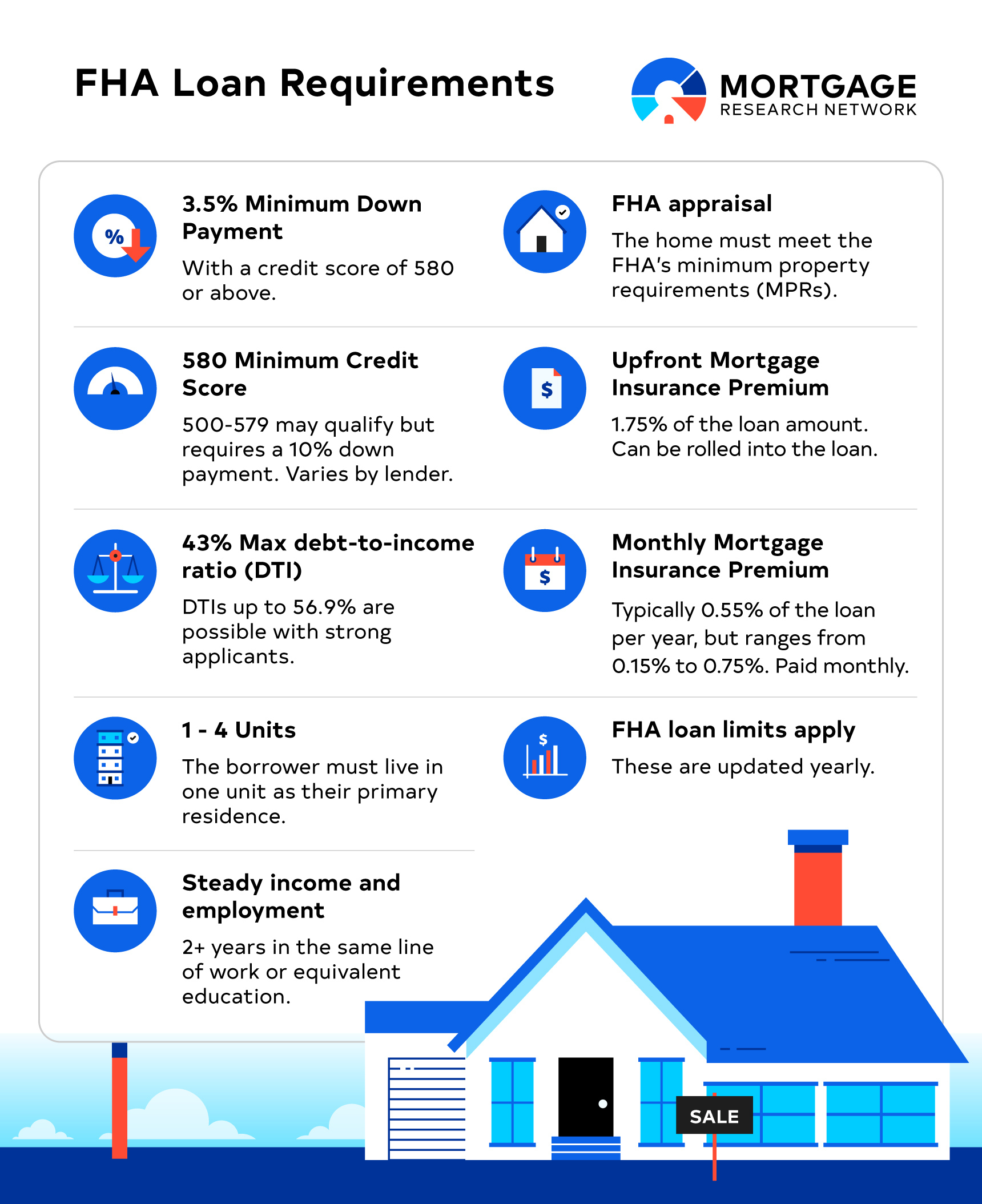

Some conventional financing options for first-timers allow down payments as low as 3%, compared to the 5% conventional financing available to other buyers. Although FHA loans aren’t restricted to first-timers, it’s another option with just a 3.5% down payment requirement and a minimum credit score of 580 (and as low as 500 with 10% down).

There are also government-backed VA and USDA loans for eligible military borrowers and buyers of eligible rural properties, respectively. Both loan options require 0% down, making them worth a second look.

You can also use down payment assistance (DPA) programs, which are available in most areas with several loan programs. These come in the form of grants or low-interest second mortgages that can cover upfront costs, such as your down payment and closing costs.

Another great benefit of first-time buyer programs is that they often include free or low-cost buyer education courses. This is invaluable for new homeowners to learn about the purchase process, how to budget for homeownership, maintain their property and other useful nuggets.

How to Find Down Payment Assistance (DPA) Programs

DPA programs are offered at the federal, state, county and city levels, making them widely available — if you know where to look. The best place to start is with your loan officer and your state’s housing agency, which administers most statewide DPA programs.

DPA programs typically work in one of three ways: grants that don’t require repayment, deferred-payment, deferred-payment loans with 0% interest that are forgiven after a certain period or low-interest second mortgages (in addition to your primary mortgage).

Colorado, for example, offers up to $25,000 in assistance, while Bank of America provides grants equal to 3% (up to $10,000) of the home’s purchase price. Other programs are available nearly nationwide, but specific amounts and terms vary by where you live and program type.

Other Qualifications to Get a Home Loan

While first-time buyer status opens doors to special programs, you'll still need to meet standard mortgage qualification requirements. Simply being eligible for first-time buyer programs doesn't guarantee automatic loan approval.

Some general mortgage qualification requirements include:

Credit score: Most conventional loan programs require a fairly strong credit profile, with some lenders setting minimum score requirements of 620+. FHA loans may accept scores as low as 580 with 3.5% down and 500 with 10% down.

Down payment: As noted, conventional loans require 3% to 5% of the home’s purchase price as a down payment. Meanwhile, FHA loans require 3.5% down (with a 580+ score) and 10% down with a 500 to 579 score. VA and USDA loans don’t require any money down.

Mortgage insurance: In most cases, if you put down less than 20%, expect to pay mortgage insurance premiums. FHA loans require an upfront and ongoing MIP, usually for the life of the loan, while conventional loans charge annual PMI that you can cancel after reaching 20% equity.

Debt-to-income (DTI) ratio: Your total monthly debt payments (including the new mortgage) typically cannot exceed 43% to 50% of your gross monthly income, depending on the loan type and your overall financial profile.

Employment and income: You'll need to demonstrate a stable employment history, usually for at least two years, to show lenders you have reliable income.

Cash reserves: You must have enough savings to cover your down payment, closing costs and typically up to six months of mortgage payments as reserves for emergencies. Exact amounts vary by lender/loan type.

Home Loan Programs for First-Time Buyers

Several loan programs cater specifically to first-time buyers or offer features that make them particularly attractive to this group. Here’s a brief overview of the most popular types.

Conventional 97 Loans

The Conventional 97 loan allows first-time buyers to purchase a home with just 3% down through Fannie Mae and Freddie Mac programs. This loan requires at least one borrower to be a first-time buyer.

Unlike some other programs, Fannie Mae's standard 97% LTV loan has no income limits, making it accessible to a broader range of buyers. The program offers cancelable private mortgage insurance, which can be removed once you reach 20% equity.

HomeReady® by Fannie Mae

HomeReady is designed for low-to-moderate income borrowers and requires earnings at or below 80% of the area median income. This program offers 3% down payments and allows you to count income from boarders or other household members who aren't on the loan.

HomeReady offers reduced private mortgage insurance costs compared to standard conventional loans. The program also considers positive rent payment history in loan eligibility, which can help renters with limited credit history.

HomePath® by Fannie Mae

HomePath is Fannie Mae's program for purchasing foreclosed properties owned by the government-sponsored enterprise. These homes are sold "as-is," but buyers can often get them below market value. HomePath Ready Buyer is a related program offering up to 3% closing cost assistance for buyers who complete a homebuyer education course.

Home Possible® by Freddie Mac

Home Possible requires a minimum credit score of 660, 3% down payment and a DTI ratio below 43%. Like HomeReady, it's designed for low-to-moderate income borrowers and offers reduced mortgage insurance costs.

This program allows "sweat equity," where buyers can contribute labor toward their down payment with seller approval, though this requires advance planning and agreement.

HomeOne® by Freddie Mac

HomeOne resembles Fannie Mae's standard Conventional 97 program and doesn't have income limits, making it accessible to higher-earning first-time buyers. It requires 3% down and offers competitive rates for qualified borrowers.

FHA Loans

FHA loans require a minimum down payment of 3.5% with a 580 or higher credit score or 10% with a score between 500 and 579. These government-backed loans are available to all buyers, not just first-timers, and have no income limits.

FHA loans require mortgage insurance for the life of the loan, but they offer more flexible credit and income requirements than conventional options.

Good Neighbor Next Door

This HUD program offers significant discounts (up to 50% off list price) to teachers, firefighters, emergency medical technicians and law enforcement officers. Participants must live in the home as their primary residence for at least three years and commit to the community they're serving.

USDA Loans

USDA loans are available for rural and some suburban properties, offering 100% financing (no down payment required) for eligible buyers. These loans require borrowers to earn less than 115% of the area's median income and usually require a credit score of 640 or higher.

VA Loans

Available to eligible veterans, active-duty service members, and surviving spouses, VA loans typically require no down payment and no mortgage insurance. These loans offer competitive rates and flexible credit requirements, making them an excellent option for military families.

State and Local Programs

Most states, counties and cities offer their own first-time buyer programs through their Housing Finance Agencies. These programs often provide down payment assistance, reduced interest rates or special loan terms tailored to local market conditions.

How to Get the Most Out of First-Time Homebuyer Programs

Before you start your home search, sit down with a loan professional to understand your first-time homebuyer options and how to qualify for the programs that best suit your situation. Working with experienced real estate agents and mortgage loan officers who understand these programs can make the difference between a smooth transaction and a bumpy ride to the closing table.

Research early on in the process. Many DPA and local programs have limited funding that’s allocated on a first-come, first-served basis, so starting your application process early in the year can boost your chances of securing help.

This is a biggie: Budget for expenses beyond the initial home purchase. In addition to your down payment and closing costs, you’ll need to pony up for home inspections, appraisals, moving costs, immediate and ongoing maintenance, property taxes, homeowners insurance and (potentially) homeowners association dues.

Consider taking a homebuyer education course even if it’s not required for your loan program. This can be a great way to prepare yourself for what’s ahead on your homeownership journey and better prepare you, mentally and financially, for making sound, savvy real estate decisions.

Final Thoughts

The path to homeownership might be more accessible than you think, especially with the wide range of first-time buyer programs available today. Whether you're truly buying your first home or returning to homeownership after a three-year gap, these programs can provide the financial support and guidance you need to make your dream a reality.

Ready to explore your homebuying options? Start your journey here to connect with experienced professionals who can help you navigate the first-time buyer programs that best fit your situation.