You can use down payment gift funds to cover some or all of your home purchase costs, making homeownership more accessible. Conventional loan guidelines allow gifts from family members and other eligible donors, with straightforward documentation requirements and minimal restrictions—just be sure to follow the rules to ensure your funds are accepted.

Buying a home can take a real toll on your savings account.

You might need tens of thousands of dollars including the down payment and closing costs, even with a low-down-payment conventional loan option.

Thankfully, conventional lenders allow borrowers to use down payment gift funds to pay some or all of their purchasing expenses.

Here’s everything you need to know about down payment gift guidelines for conventional loans, including eligible donors, required documents, and exceptions to standard gifting rules.

Down Payment Gift Limits for Conventional Loans

Conventional lending standards are pretty lenient regarding how much (or how little) down payment gift you can put towards your home purchase. As long as the funds come from eligible donors, there’s no limit to the amount you can receive as long as there’s no cash back at closing.

With a conventional loan, down payment gifts can fund some or all of your:

Down payment

Closing costs

Financial reserves

In certain situations involving gifted funds, you may be required to make a personal contribution towards the purchase. But there’s even a way to use gift funds to meet that requirement. We’ll cover both of those topics later in the article.

Note: Conventional lenders do not allow gift funds to be used for investment properties. Down payment gifts may only be used when purchasing your primary residence or a second home. However, multi-unit primary residences where you rent out additional units do qualify.

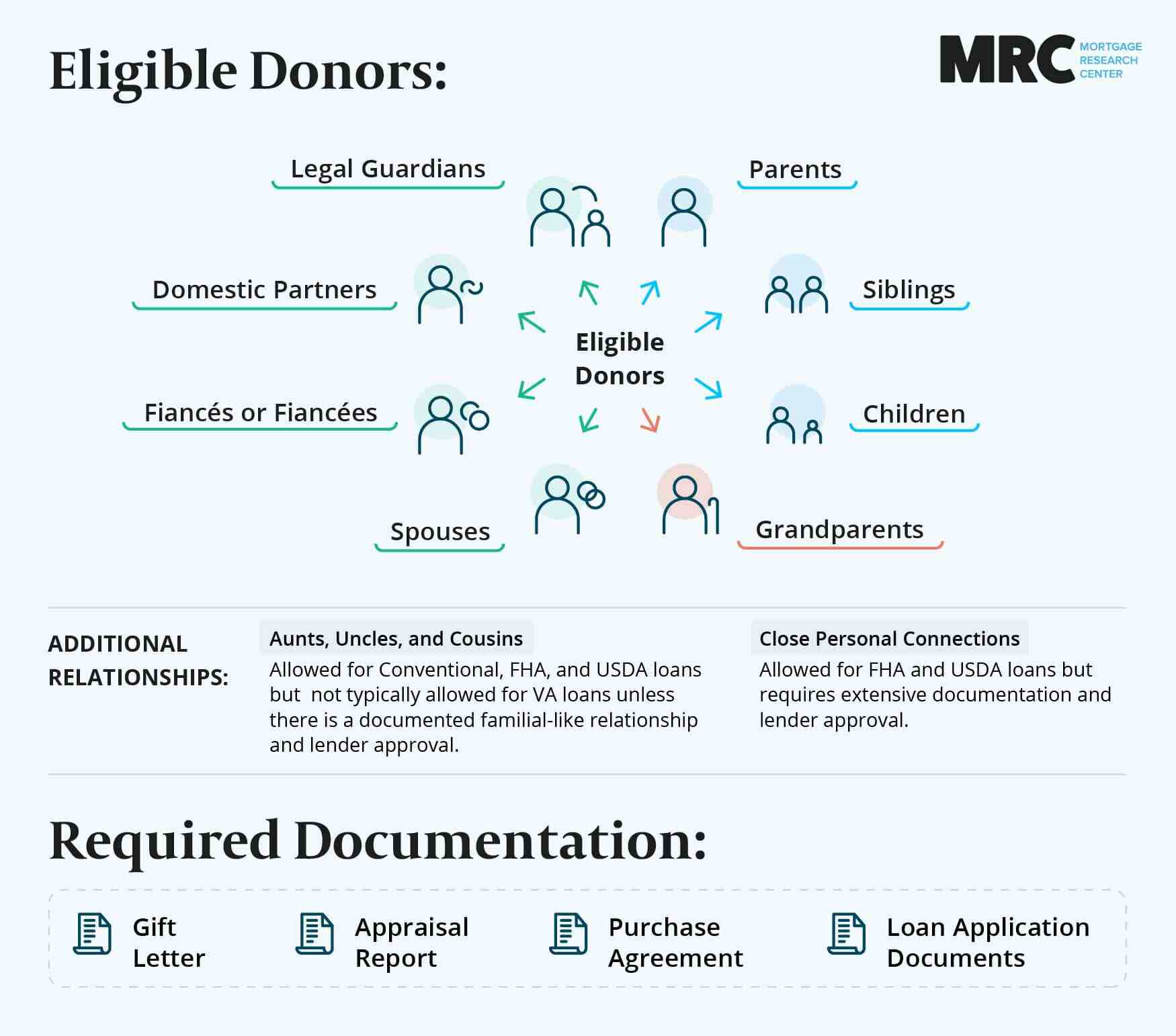

Eligible Donors for Down Payment Gifts

You can receive down payment gifts from a wide range of eligible donors. For the most part, the list includes anyone related to you by:

Blood

Adoption

Guardianship

Marriage

You can also receive gift funds from your fiancée/fiancé, domestic partner, and anyone related to them. Conventional lenders can even allow gifts from godparents and other individuals with "close, family-like ties."

Recent Change: Fannie Mae now allows gifts from the trust or estate of an eligible donor. This change went into effect in September 2023.

Exceptions to Eligible Donor Requirements

Freddie Mac cuts out a couple of exceptions to the standard list of donors. In these situations, you can receive gifts from unrelated individuals and use them as an eligible source of funds.

Wedding Down Payment Gifts

You can use money received as a wedding gift from unrelated individuals to cover your down payment and other costs. You'll need to provide a copy of your marriage license or certificate and proof that the funds were deposited into your account within 90 days of the document's date.

Graduation Down Payment Gifts

If you've recently graduated from an educational institution, graduation gifts from unrelated individuals can also be used as eligible funds. You'll need official documentation of the date you graduated, such as a diploma or transcript, and proof of the funds being deposited into your account within 90 days.

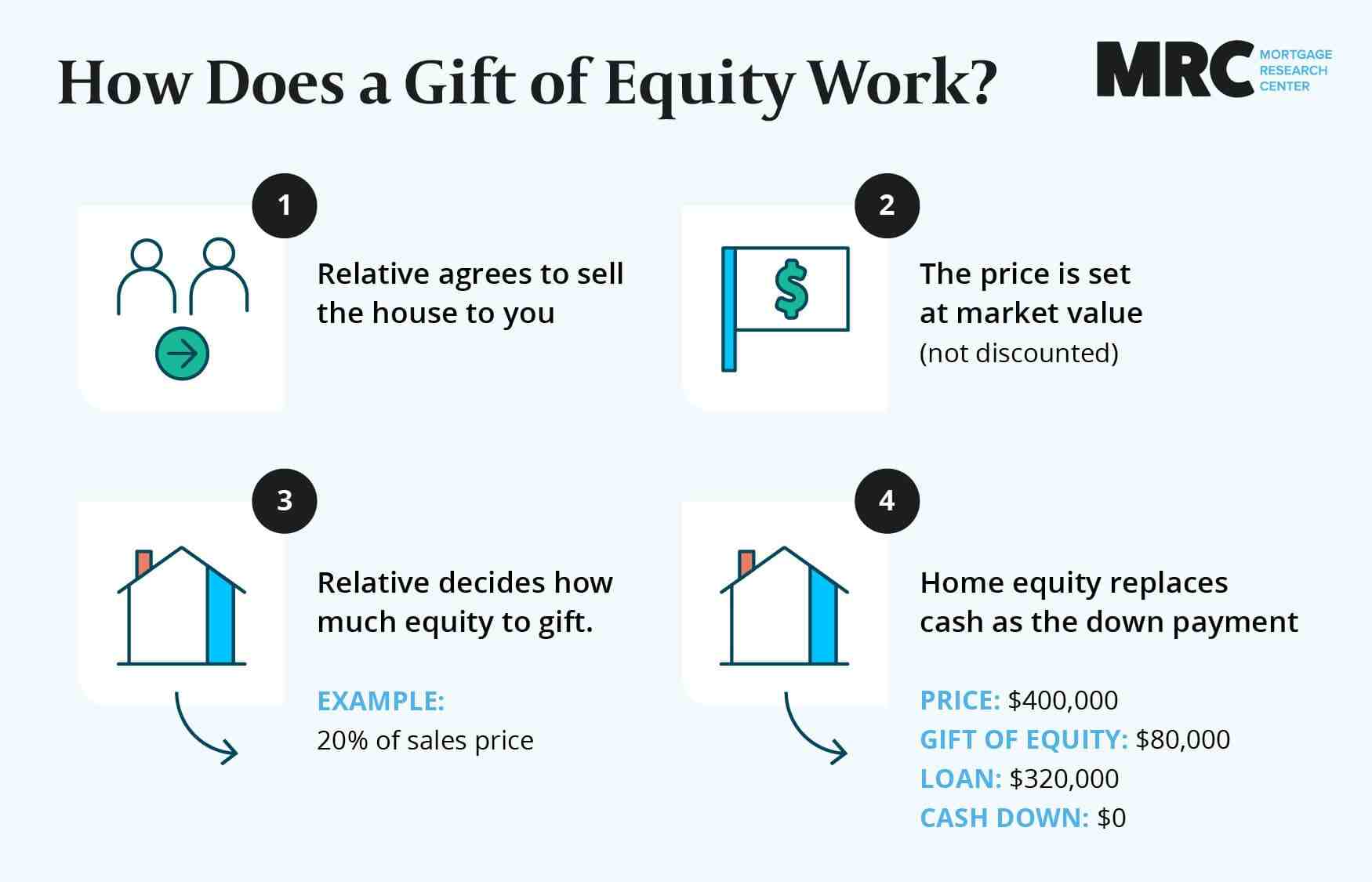

Gifts of Equity

A gift of equity is a specific type of down payment gift that you can receive when purchasing a home from anyone who's an eligible donor. Instead of writing a check, they credit part of the home’s equity to you.

No money changes hands, but you can use the gifted equity to cover your down payment and closing costs.

Closing Cost Credits

Lenders allow you to receive closing cost credits from the property seller, real estate agent, or other interested parties. These unique gift funds cannot be put towards your down payment but can pay conventional loan closing costs.

While there’s no maximum to standard gift funds, closing cost credits provided by an interested party are limited by the size of your down payment. For your primary residence or a second home, the limits in most cases are:

Down Payment | Max. Closing Cost Credits |

Less than 10% | 3% |

10% - 24.99% | 6% |

25% or Greater | 9% |

Gift Funds: Documentation Needed

You will need a little extra documentation when receiving down payment gift funds. However, the requirements should be minimal compared to the rest of the lending process.

Supporting Documentation for Gifted Funds

Lenders will want proof that the donor has the funds available. Most often, the simplest way to prove available funds is with a bank or investment account statement in the donor's name.

If you've already received the down payment gift funds, lenders need proof that the funds originated from the donor and were deposited into your account. This could be:

Your deposit slip and the canceled check

Your deposit slip and the donor's withdrawal slip

Electronic evidence that the funds have transferred from the donor’s account to yours

Gift Letter

You will also need to provide a gift letter, signed by the donor, documenting the details of the down payment gift. Your lender will likely provide you with a letter in their preferred format, but expect it to include:

The donor’s relationship to you

The donor’s full name, address, and telephone number

The exact or maximum dollar amount the donor is gifting

A statement that the donor does not expect you to repay the gift

Potential Issues With Down Payment Gifts

Down payment gifts can usually cover your upfront mortgage expenses with little problem. There are, however, a few potential issues that you may run into:

1. Your donor does not want to provide account statements.

If your donor is uncomfortable turning over financial account statements to prove the availability of funds, they can transfer the funds to you and only have to prove that the gift originated from them. Or, to simplify the process, they can write a check or transfer the gift amount directly to the closing agent.

2. Your donor doesn’t meet eligibility requirements.

Down payment gift guidelines have a comprehensive list of eligible donors, from direct family to godparents and individuals with family-like ties. But if your donor doesn’t meet the eligibility requirements, you won’t be able to use the funds towards your conventional loan.

Some lenders may have non-conforming products that allow gift funds from unrelated donors, but they won’t be conventional loans.

3. Your donor is your real estate agent or an interested party.

If your donor is your real estate agent or an interested party to the transaction, you can't use their down payment gift funds. Anyone who benefits from the sale of the property is considered an interested party and can only contribute closing cost credits per the terms of your loan.

For lending purposes, the property’s seller is not considered an interested party if they’re otherwise an eligible donor and not affiliated with any other interested party.

Down Payment Gift Tax Implications

Most individuals will not face tax implications by providing or receiving a down payment gift. Taxes are technically the responsibility of the donor. However, the IRS offers annual and lifetime exclusion limits, eliminating the burden in most cases.

As of 2025, donors can provide an annual tax-free gift of $19,000 per recipient. A married couple providing a down payment gift to their child could give $38,000.

Gift funds that exceed the annual limit count towards the donor's lifetime exclusion. That is currently $12.92 million. Actual tax burdens don’t begin until that lifetime limit has been reached. All that being said, check with a licensed tax professional before filing.

Required Personal Contributions

For most purchases, gift funds can be used to cover the entirety of your down payment and closing costs. This is always the case with conventional loans on a single-unit primary residence.

For second homes and primary residences with 2-4 units, however, you’ll need to provide 5% from your own funds if your total down payment (including gifts) is less than 20%. This requirement is lowered to 3% with HomeReady and Home Possible Loans.

There is one exception to the personal contribution rule. If gift funds are received from an eligible donor who has been living with you for at least 12 months and plans to live with you in your new home, they can be used to cover any required personal contribution.

Buying a Home With Down Payment Gift Funds

Gift funds can be one of the most effective ways for buyers – especially those purchasing their first home – to meet down payment and closing cost requirements. Thankfully, down payment gift guidelines make it simple to use funds from any relative or otherwise eligible donor when obtaining a conventional loan.

If you have someone willing to provide you with money to help purchase a home, contact a lending professional to figure out exactly how far your down payment gift funds can get you.