As a first-time homeowner, there’s a lot you’re going to need to learn about your new mortgage. These eleven topics will provide a strong foundation of knowledge to get you on the right track.

Becoming a first-time homeowner is an exciting experience. However, there's still a lot to learn about owning a home – and your new mortgage. That's why we've put together this list of 11 things to know after your mortgage closes that many new buyers aren't always aware of from the start.

1. When Is Your First Mortgage Payment Actually Due?

Your first mortgage payment is typically due on the first day of the month, the month following the next calendar month. For example, if your closing is May 10th, your first payment will likely be due on July 1st.

Unlike rent payments, which are paid in advance for the coming month, mortgage payments are paid in arrears for the previous month. Thus, you skip a month of payments as interest accrues the full month after closing. Interest accrued from closing to the end of the month is paid at closing, and called “prepaid interest” – one of the expenses listed on your Closing Disclosure.

Keep in mind that while the 1st of the month is the most common mortgage due date, your lender may have a different policy. Be sure to check the terms of the lending agreement and the First Payment Letter – included as part of your closing documents – to verify the date by which you're responsible for paying.

With some lenders, it may be possible to request that payment be due on a different date that better aligns with your pay schedule or cash flow needs. However, not all mortgage companies offer this option.

2. Who Do You Make Payments To, and Why Might It Change?

The company that you make your mortgage payments to will not necessarily be the lender that originated your loan. After closing, it's common for lenders to sell a mortgage to recoup their funds in order to issue future loans.

Plus, the company that owns your mortgage may choose to service it in-house or sell the mortgage servicing rights (MSRs) to another company. Mortgage servicing includes processing payments, managing escrow, handling customer service, and other aspects of loan management.

This means the company that owns your loan may not be the same one you make payments to. As a homeowner, your loan servicer is far more important, as it will be your point of contact for most anything related to your mortgage.

If your loan servicer changes, you can expect to receive a letter from both the old and new servicing companies. If you’re concerned about the authenticity of mail you receive about a servicing change, always contact your previous servicer for verification.

Note: If you have your mortgage on autopay and your loan servicer changes, you’ll need to set up autopay with the new company to ensure payments continue to be made on time.

3. What Happens When You Receive a “Notice of Mortgage Transfer/Sale”?

There’s no reason to worry if you receive a “Notice of Mortgage Transfer/Sale.” As we mentioned previously, mortgages are commonly sold shortly after closing to provide the originating lender with the funds needed to issue new loans.

In fact, your mortgage will likely be transferred multiple times throughout the life of your loan. This is a normal process and will not affect you, except that you may need to send your payments to a new servicer.

When your mortgage is sold or transferred, the new servicer cannot alter the terms of your loan. You're locked into the terms you agreed to at closing until you pay off your mortgage or refinance it into a new loan.

If you receive a new servicer as part of the mortgage transfer or sale, federal law grants you a 60-day grace period during which you can't receive late fees or negative marks on your credit if you accidentally remit your payment to the old servicing company.

This rule only applies, however, if payment is made to the previous provider, not if you fail to make your mortgage payment altogether.

4. Understanding Your Escrow Account

Your monthly mortgage costs include more than just principal and interest. You'll also be putting funds into an escrow account, which the lender uses to cover property taxes, homeowners' insurance, and mortgage insurance. This protects both you and your lender by ensuring that these items get paid on time.

In some cases, your escrow account may include homeowners association dues, though this is rare. Be sure to check out your mortgage agreement to verify whether you're responsible for paying these dues separately.

Federal law allows lenders to include a "cushion" in your annual escrow payments of up to two extra months' worth based on your anticipated escrow costs. This cushion protects the lender from an escrow shortfall if costs rise or escrowed expenses come due before you've made enough mortgage payments to cover them.

However, some states have laws that limit the escrow cushion to one or even zero months of payments, so be sure to check your state's regulations to understand how this may affect you.

5. Annual Escrow Analysis and Payment Adjustments

Your loan servicer will conduct an escrow analysis every year to verify that your escrow payments remain sufficient to cover your escrowed expenses, such as property taxes and insurance premiums.

Based on their analysis, the amount you're required to contribute to escrow may vary from year to year. This means that even if you have a fixed-rate mortgage, your monthly payments could change.

After your loan servicer has conducted its analysis, you will receive an Annual Escrow Analysis Statement that highlights both your escrow activity for the previous year and the projected summary for the coming year. It will also specify whether your mortgage payments will change and, if so, what the new amount will be.

In some cases, your Annual Escrow Analysis Statement may point out either a surplus or a shortage in your escrow account. This occurs when your escrow payments were not in line with the actual expenses for the previous year.

In the event of a surplus, you'll typically be refunded the excess by check from your servicer. If there's a shortage, you can either pay the difference as a lump sum or have it divided evenly and added to next year's escrow payments.

6. Grace Periods, Late Fees, and Credit Reporting

If you miss your mortgage payment due date, you'll generally have a grace period before your loan servicer assesses any penalties. In most cases, the grace period is 15 days, although that can vary by lender. Make sure to review your loan agreement to confirm your individual late-payment grace period.

For example, suppose your mortgage payment is due on the 1st, and you have a 15-day grace period. In that case, you can make your payment up to the 15th of the month without incurring a penalty. On the 16th, your lender would charge a late fee, which commonly ranges anywhere from 2% to 6% of the payment amount.

Even if you're late on your payment, though, it may not necessarily have a negative impact on your credit. That's because even if you're outside of the grace period, lenders typically do not report late payments to credit agencies unless they are at least 30 days past due.

If your mortgage payment gets lost in the mail or accidentally sent to the wrong place, reach out to your loan servicer and explain the situation. In many cases, they may be willing to waive the late fee, particularly if this is the first time it has happened.

7. Setting Up Automatic Payments and Online Access

After closing on your loan, you'll receive information from your lender about how to set up your online account. In some cases, this will be included in your closing documents. Other times, it may take a few weeks to receive the instructions in the mail.

Also, remember that if your loan servicer changes, you’ll need to create an online account with the new company. The welcome letter from your new servicer should outline how to do so.

While you can make manual mortgage payments online, by mail, or by phone, many borrowers opt to enroll in autopay so their payments are made each month automatically. Some lenders may offer a slight discount for doing so.

Even if you're using autopay, however, it's essential to keep an eye on your monthly mortgage statements. If an issue arises and your payment doesn't go through, you will still be responsible for any fees and penalties, and it could potentially get reported on your credit. Regularly monitoring your statement helps resolve any problems as quickly as possible.

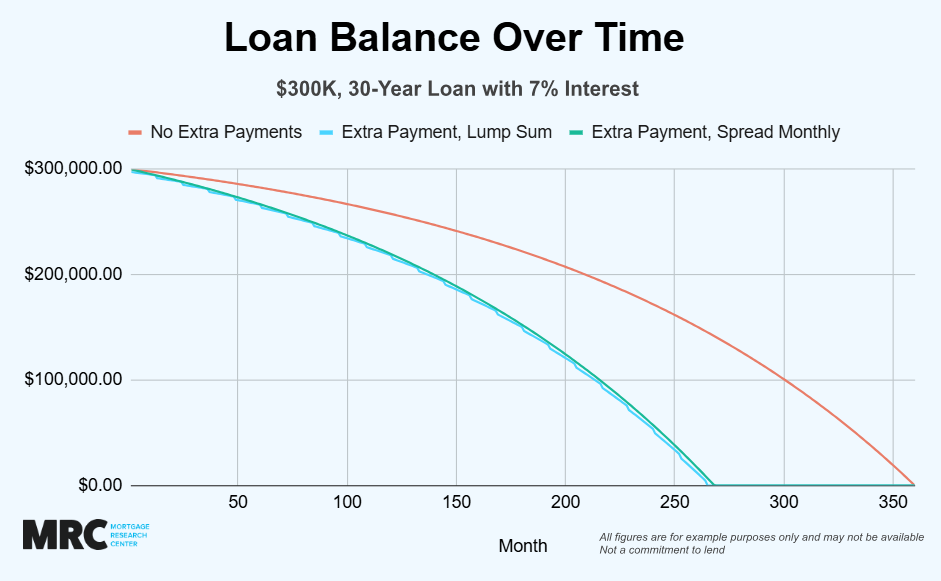

8. Making Extra Payments: Principal-Only vs Regular Payments

Looking to pay your mortgage off sooner? In addition to your monthly payment, you can make extra payments to reduce your principal balance. However, the process for doing so can vary by company.

Your lender may offer an option in their online portal to make a principal-only mortgage payment. This is often the simplest way to ensure your extra payment gets applied to your principal balance.

Frequently, though, you will need to contact your lender and explicitly request that your additional payment be designated toward your unpaid principal.

Occasionally, you may even be able to just make a larger-than-required payment, with your lender applying the excess to your balance. That's not common, though, so it's vital to check with your loan servicer for their specific extra-payment policies.

If you fail to meet the lender's requirement for designating principal payments, the additional funds will likely just be applied to the following month's mortgage payment.

Another option for paying your mortgage down faster is to set up bi-weekly payments instead of monthly. This payment schedule allows you to make the equivalent of 13 monthly payments per year instead of 12.

As with principal-only payments, however, it's important to speak with your lender about this plan, as they may otherwise reject your bi-weekly payments for being "partial."

9. Tax Documents and Year-End Statements

Your loan servicer will send you a Form 1098 – Mortgage Interest Statement – every year for your taxes. The IRS requires lenders to send this statement out by January 31st. It may either be sent by mail or made available in your online portal.

Form 1098 will include your personal information, the address of your home, your outstanding loan balance, and any interest and mortgage insurance premiums you’ve paid for the previous year.

This is helpful because borrowers who itemize their taxes can deduct their mortgage interest. While temporarily suspended in 2021, homeowners who meet income requirements will also be able to deduct mortgage insurance premiums beginning again in tax year 2026.

Another applicable deduction that you can claim is lender discount points. These are points that you likely paid at closing to buy down your interest rate. Most of the time, this deduction is spread across the life of your mortgage. However, if you meet specific criteria, you can deduct them in full during your first year of home ownership.

Keep in mind, however, that you may only deduct these mortgage costs if you itemize your tax deductions. For some homeowners, it may make more sense to claim the standard deduction. Be sure to speak with a tax professional to determine which option is best for you.

10. What to Do if You Have Issues or Disputes With Your Servicer

Suppose your loan servicer makes an error with your mortgage balance or charges you an inaccurate penalty or fee. In that case, federal law gives you the right to dispute the issue and requires the loan servicer to investigate.

However, you must follow the proper procedure by sending a Qualified Written Request to the company's customer service or error correction mailing address.

Note: This address will likely differ from where you send mortgage payments, so make sure to contact your loan servicer to verify you have the correct address. Your lender is not required to respond to written requests sent to the wrong place.

Your Qualified Written Request must include your name, address, loan number, and a detailed description of the disputed issue. Loan servicers are required to acknowledge your request within five business days and, in most instances, respond in full within 30 business days.

If your loan servicer does not respond within the allotted timeframe, or if you believe they are incorrect in their final decision, you can escalate your complaint to the Consumer Financial Protection Bureau (CFPB) either online or by phone.

11. Keeping an Eye on Interest Rates

Finally, make sure to monitor how mortgage interest rates are trending regularly. If rates have dropped since you took out your loan, you may be able to refinance and reduce your payments and overall interest costs.

For conventional loan holders, there's no waiting period to do a rate-and-term refinance. The same applies to FHA rate-and-term refinances for current FHA borrowers. Other types of government-backed refinances – particularly streamline refinances – may have waiting periods that vary by program.

Refinancing will mean incurring new closing costs, however, so make sure to speak with a lending professional who can help explain your break-even point – the length of time it will take for the potential savings to outweigh these upfront expenses.

Understanding Your New Mortgage

As a first-time homeowner, it's normal to have questions about aspects of your loan. The eleven topics covered in this article will provide a strong foundation for understanding your mortgage. Still, they may not cover every situation you could face.

The best advice? If there’s ever anything that you’re unsure of, just reach out to your lender and ask!