Having an underwater mortgage can make it difficult to refinance your loan or sell your home. However, you can still establish equity by making your monthly payments and waiting for property values to rise.

Home values surged in the early 2020s as historically low interest rates and the ability to work remotely increased demand in real estate markets across the country. Now, as many of these communities have transitioned into buyer’s markets, prices have dropped, leaving some homeowners underwater on their mortgages.

We’ll explore what it means to have an underwater mortgage, how being underwater can affect you, and the options you have for remedying it.

What Does It Mean to Be Underwater on a Mortgage?

Being underwater on a mortgage means that you owe your lender more than your home is currently worth. You may also see this referred to as having negative equity or being upside-down on your loan.

For example, say that a first-time buyer purchased a home in late 2022 for $400,000 using a 3% down conventional mortgage. They originally financed $388,000 and have consistently made their monthly payments since. Their current loan balance is $367,000.

However, their area has seen a sharp decline in property values, and their home is now worth just $350,000. Since they still owe their lender $367,000, they are underwater on their mortgage by $17,000.

How Do Mortgages Become Underwater?

Buying a home can be a strategic long-term investment. However, a declining market, missed payments, or simply selling too soon can leave you with negative equity.

Declining Property Values

The most common reason homeowners find themselves underwater on their mortgage is that property values have decreased in their area. According to the Federal Reserve, the median home sales price reached $442,600 in late 2022. By mid-2025, that median price had fallen to $410,800 – a decline of more than 7%.

Keep in mind, however, that’s a nationwide figure. Many markets, particularly in pandemic-era hot spots, have had home values retreat much further. Austin, Texas, for example, has seen prices drop more than 20% from their peak.

Missing Payments

Another way some homeowners become underwater is by missing mortgage payments, especially in the first couple of years of their loan. Because of amortization, a significant percentage of early mortgage payments go toward interest rather than reducing the principal balance.

For example, with a $350,000 30-year mortgage at a rate of 7%, only about $3,500 is applied to principal during the first year, while interest costs add up to more than $24,000.

When payments are missed, the accrued interest is added to the total amount owed, which can potentially lead to an upside-down loan.

Needing to Sell Too Soon

You may also find yourself underwater if you need to sell your home too soon after purchasing it. That’s because agent fees and other expenses can add up to as much as 10% – or sometimes more – of your property’s sales price.

Let’s revisit our earlier example of the first-time buyer who purchased a home for $400,000 with a 3% down payment and has a remaining mortgage balance of $367,000.

Even if home values had stagnated rather than declined, and they were able to sell for the $400,000 they paid, closing costs of 10% would bring their net earnings down to $360,000. This means that they’d need to come out of pocket for $7,000 to satisfy their mortgage.

How Do I Know if My Loan Is Underwater?

Worried that you may be underwater on your loan? Here’s how to find out:

Contact your lender and ask for your payoff amount: This is the amount that it would take to satisfy your mortgage in full. Your payoff amount is typically slightly higher than your remaining loan balance because it includes any interest accumulated for the current month, as well as any other fees that may apply.

Determine your home’s current value: For a ballpark estimate of your home’s worth, check out platforms like Zillow that use an automated valuation model to calculate current property values. An appraisal or comparative market analysis can provide a more accurate figure, although these options come at a cost.

Subtract your mortgage payoff from your home’s worth: If this difference is positive, you have built up equity in your home. If the difference is negative, your mortgage is underwater. Assessing your mortgage because you’re planning to sell? Make sure to account for fees and closing costs in your calculations.

The Impact of Being Underwater on Your Loan

The most significant impact of being underwater on your loan is that you may have difficulty selling your home or refinancing your mortgage without bringing additional cash to the table.

As we illustrated earlier, seller closing costs can often account for 10% of a home’s sales price. If you don’t have at least 10% equity, your proceeds may not be able to cover your seller expenses. This makes selling impractical unless you can come out of pocket for the difference.

Similarly, lenders are generally not going to let you borrow more than your house is worth to refinance your loan. Conventional lenders require at least 3% equity for a rate-and-term refinance, while FHA lenders look for at least 2.25%.

Is an Underwater Mortgage Always a Problem?

Having an underwater mortgage is not necessarily always a problem. While it’s not ideal to owe more than your home is worth, if you don’t plan to move and can continue making your monthly payments, you’re unlikely to be impacted by the negative equity.

Options for an Underwater Mortgage

Currently underwater on your mortgage? Let’s take a look at your options, particularly if you’re having trouble making your payments, and the impact that each may have.

Build Equity Organically

As we’ve already mentioned, if you don’t need to sell and can continue making your monthly payments, your best option is to keep paying on your loan and build your equity organically.

The further you are into your loan term, the greater the portion of your payments that are applied to your principal balance. Over time, you’ll begin to build equity faster.

Also, declining markets are only temporary. Eventually, home values will rise, and waiting out the current dip will allow you to overcome your negative equity through appreciation.

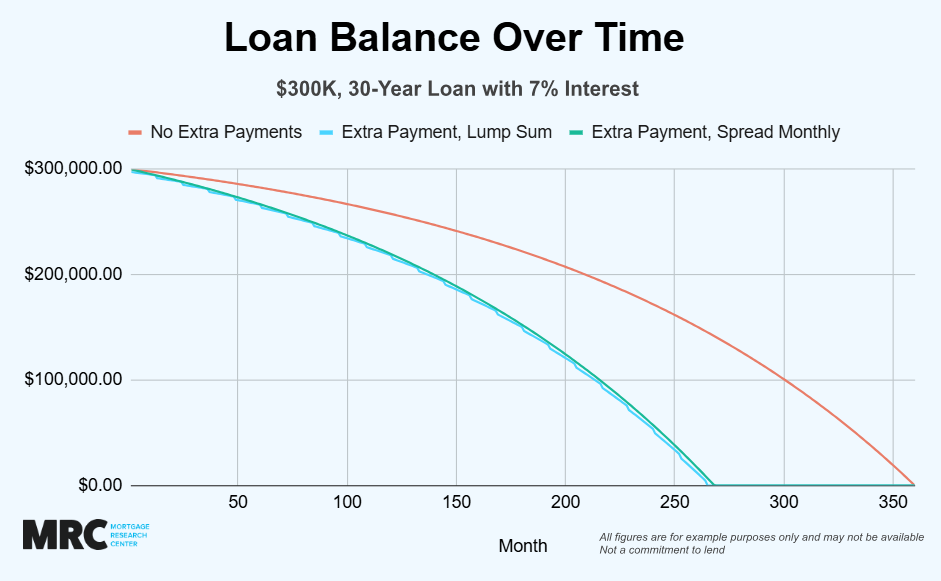

Make Extra Payments

Making extra payments toward your mortgage can be a practical method for reducing your principal balance and paying off your loan sooner, but it can also help you get out of an underwater mortgage at a pace that works for you and your budget.

If you’re planning to make additional payments on your underwater loan, be sure to reach out to your lender and request that the extra amount be applied to your principal. While some mortgage providers may do this automatically, many will simply apply the overpayment to your next month’s bill if you fail to contact them first.

Cash-In Refinance

A cash-in refinance involves you contributing a lump-sum payment toward your mortgage as part of the refinancing process. By paying down your loan, you’re converting your cash into home equity, which can get you out of an underwater mortgage and allow you to meet lender equity requirements.

A cash-in refinance can be a practical option for homeowners who have funds available and would like to adjust their loan terms, such as securing an interest rate lower than what they’re currently locked into. In addition, reducing the amount you owe will cut your overall interest costs, saving you money over the life of your loan.

Streamline Refinance

Have interest rates dropped since you purchased your home, but having little to no equity is preventing you from refinancing and lowering your payments? If you have a government-insured loan backed by the FHA, VA, or USDA, you may still be in luck.

These mortgage programs each offer streamline refinances that let you reduce your interest costs without requiring a new appraisal or valuation. In fact, you may not even need to reverify your earnings, making this an ideal option for homeowners who have also seen their income decrease.

Unfortunately, there is currently no conventional streamline refinance option, so you must already have a mortgage through one of the federally backed programs to qualify.

Loan Modification

If you’re facing financial hardship, your lender may be willing to change the terms of your mortgage through loan modification. This can involve adjusting your repayment term, interest rate, or even your principal balance to make your housing costs more affordable.

Loan modification can be an alternative to refinancing for homeowners who are underwater on their mortgage and unable to refinance through traditional channels. Keep in mind, though, that lenders are not required to agree to a modification, and those who do will typically only do so after you’re already behind on your payments.

Forbearance

Loan forbearance is another option for homeowners facing a temporary financial hardship and who are unable to refinance due to low or negative equity. With forbearance, your mortgage terms remain the same, but your lender allows you to pause your payments for a set number of months.

While loan forbearance can offer a temporary reprieve, your loan will likely become further underwater as you’ll still be responsible for the accumulating interest. You may also need to establish a repayment plan for the missed payments once forbearance ends.

Short Sale

When you’re underwater on your mortgage, selling your home is a challenge. However, if you need to move or are positive that you will no longer be able to continue making your monthly payments, you can ask your lender to approve a short sale.

In a short sale, your lender agrees to accept less than you currently owe on your loan, meaning that you would not need to bring additional cash to the closing table.

Short sales, however, will negatively impact your credit and can prevent you from obtaining another mortgage for several years. In addition, some lenders may pursue a deficiency judgment, which could leave you on the hook for the difference between the sales price and the full loan balance.

Deed in Lieu

If you’re behind on your mortgage and are unable to sell because you’re underwater, another option is to offer your lender a deed in lieu of foreclosure. Unlike a short sale, which involves putting your home on the market and selling to a third party, a deed in lieu is used to transfer ownership of the property directly to the lender.

Settling your loan with a deed in lieu will also negatively impact your credit and prevent you from obtaining another mortgage in the immediate future. However, the consequences are typically less severe than an actual foreclosure, and extenuating circumstances may even help shorten the wait.

In most cases, deed in lieu is only an option when you’re severely behind on your payments, and foreclosure is inevitable. For lenders, accepting a deed in lieu allows them to avoid the often expensive foreclosure process.

Bankruptcy

If you’re underwater on your mortgage and facing foreclosure, but want to keep your home, filing for bankruptcy will prevent your lender from taking further action while your case is reviewed by the court.

Chapter 7 Bankruptcy

Chapter 7 bankruptcy involves liquidating your assets to satisfy your debts for less than the full amount you owe. Under Chapter 7, you could be ordered to sell your home, although in this scenario, you would not be responsible for owing a deficiency judgment.

Chapter 13 Bankruptcy

Under Chapter 13 bankruptcy, you would establish a three to five-year repayment schedule to bring you current on your mortgage and keep you in your home. This can be a practical option for homeowners who are underwater due to missed payments, allowing them the opportunity to rebuild equity.

Strategic Default

A strategic default is a calculated decision to stop paying on your mortgage, even if you’re financially able to continue making payments.

Following the housing crash of 2008, strategic default became a common strategy for homeowners who were severely underwater on their mortgages, defined as having a loan balance more than 125% of a property’s value. According to the National Association of Realtors, 2.8% of residences are presently severely underwater.

It’s never recommended, though, to initiate a strategic default. I will have negative consequences on your credit and may leave you open to a deficiency judgment, particularly if you have other assets that the lender could pursue.

It may seem that you will never break even on your investment, but plenty of severely underwater homeowners in 2008 saw their property values triple since.

In Conclusion

Being underwater on your mortgage – meaning you owe more than your home is worth – is not ideal, but it is unlikely to impact your day-to-day life if you don’t plan on moving and can continue making your mortgage payments.

However, an underwater mortgage may pose an issue if you find yourself in financial hardship, making it difficult to refinance your loan or sell your home. If you currently have negative equity and are concerned about your mortgage payments, contact your lender, explain the situation, and ask about your personalized options.