Homeownership can seem out of reach for many people in today’s real estate market, often due to the upfront costs associated with purchasing property. While low down payment options do exist, buyers can still need tens of thousands of dollars on hand to close on the average home.

However, one unique option can help make homeownership a reality with next to no required down payment and closing costs subsidized by the federal government: the HUD Homes $100 Down program.

What Are $100 Down HUD Homes?

The U.S. Department of Housing and Urban Development (HUD) is a government agency that oversees the Federal Housing Administration (FHA).

One of the core functions of the FHA is to improve housing accessibility by insuring mortgages for borrowers who may otherwise have limited options for obtaining an affordable home loan.

When a homeowner defaults on an FHA-insured mortgage and is foreclosed, the lender is compensated for its losses, and HUD takes ownership of the property.

However, HUD does not want to hold onto these homes. The agency’s top goal is to make housing more accessible, so it offers HUD-owned foreclosure homes to qualified buyers for just $100 down.

Finding $100 Down HUD Homes

After HUD has taken ownership of a property and cleared it for sale, the home is then listed by a nearby HUD-approved real estate broker. In most cases, HUD-owned houses can be found on local Multiple Listing Service (MLS) platforms.

It can often be difficult to identify these $100 Down HUD Homes among the sea of other listings, though, so the agency has made it simpler for buyers to find available properties in their area through the HUD Homestore.

On the front page of the HUD Homestore website, you will see a map like the one below. Shaded states have available HUD homes for sale.

Keep in mind that there may not be many homes available near you. Foreclosures of all kinds – including HUD-owned homes – are currently hard to find due to a strong economy and high homebuyer demand. Because of rapid appreciation in recent years, most people who can no longer pay their mortgage simply sell on the open market.

Act Quickly for the Best Chance at Finding Quality HUD Homes

Due to the affordability of HUD homes and the $100 Down HUD Home program, some buyers watch the HUD Homestore website daily for new listings. When a desirable one appears, their real estate agent makes an offer immediately.

But here’s another reason you may need to act quickly: There’s an initial 15-day period in which only owner-occupant offers are accepted. After that, investors and cash buyers, including those from out of state, can swoop in to grab these deals.

Homebuyers who are patient but able to act quickly will eventually find a home to submit an offer on.

How To Make an Offer on a HUD Home

Making an offer on a HUD home is a little different from making an offer on standard properties you see on the open market.

If you’re serious about purchasing one of these homes, your first step is to find a HUD-approved real estate agent. Only HUD-approved agents can submit offers. You can search for an agent in your area on the HUD website, or your current agent can go through the process to become HUD-approved.

Next, here’s what to do:

- Get pre-approved for a loan from an FHA lender that offers the $100 down program – not all mortgage companies do, so be sure the lender you apply with does.

- Watch for homes that are within your price range and geographic area you’re interested in living.

- When a suitable property appears, examine its condition. Foreclosures can come in all shapes. If repairs are needed, make sure you are comfortable doing the work yourself or paying for the improvements.

- Have your HUD-approved agent submit a full-price offer – offers below the listing price are not eligible for the $100 Down HUD Homes program.

- Wait to see if HUD accepts your offer. HUD does not accept offers until the 10th day after a property is listed to expand the opportunity to a larger number of owner-occupant homebuyers.

- If your offer is accepted, your next step is to submit your earnest money deposit (EMD), which is typically 1% of the home’s price up to $2,000.

👉Stay ahead of the market with the Mortgage Research Network Podcast.

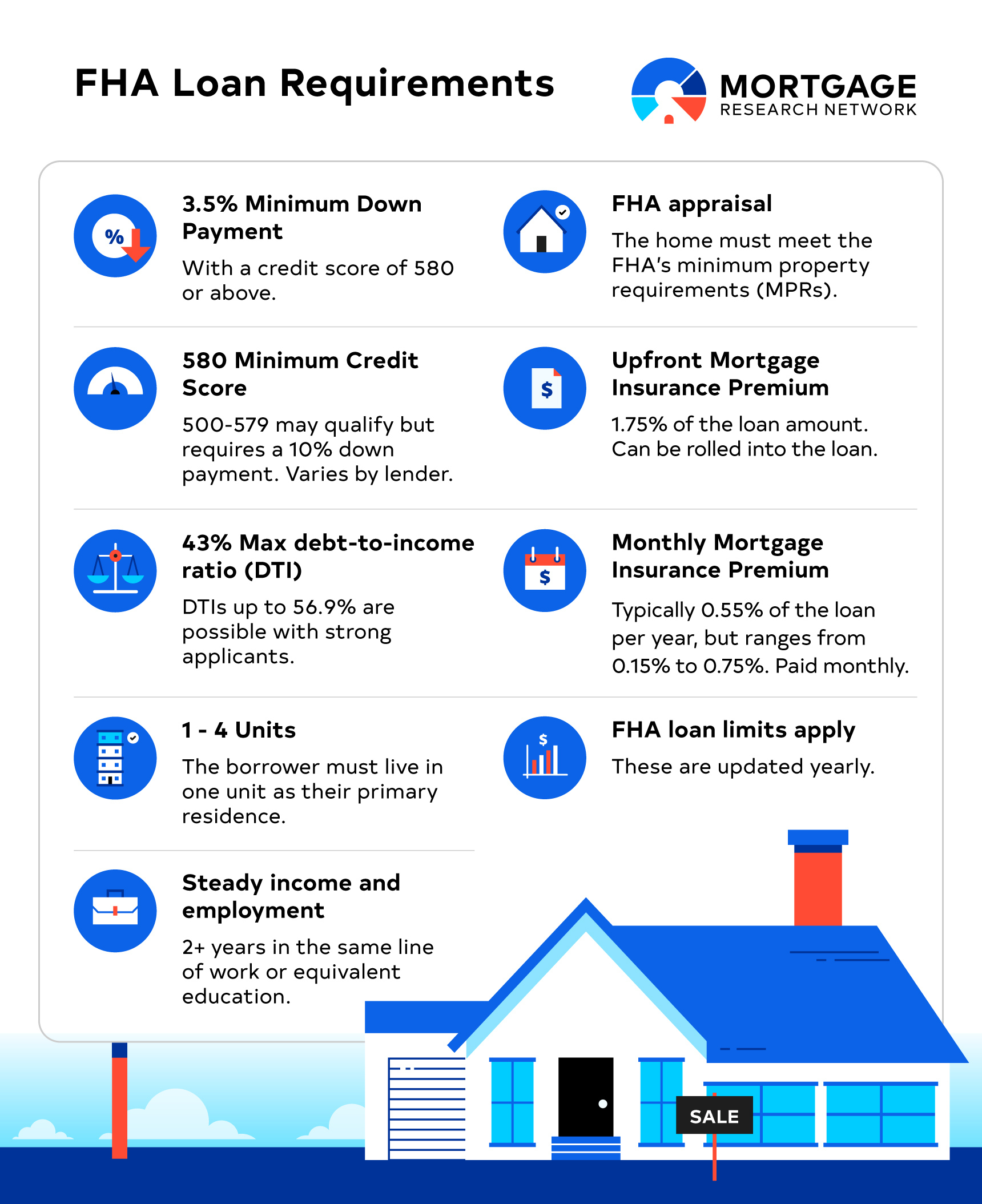

Who Qualifies for the $100 Down Program from HUD?

Just about anyone who qualifies for a standard FHA loan is eligible for the $100 down program.

This means that you must have:

- A minimum credit score of 580 or higher

- A debt-to-income ratio of 56.9% or lower

- Plans to occupy the property as your primary residence for at least one year

- Sufficient funds to cover the $100 down payment and closing costs, which are typically 2-5% of the home’s price (although HUD offers a 3% closing cost credit)

- Two years of consistent employment/income history

- No bankruptcies or foreclosures within the past two years.

In addition, you must meet any other applicable FHA requirements and have not purchased another HUD home within the previous two years.

Compared to other types of mortgages, FHA loans are among the easiest to qualify for. Even if you don’t think you could ever own a home, the $100 down program could make you a homeowner.

How To Buy a $100 HUD Home That Needs Work

Just like any foreclosure, HUD homes may be in disrepair. One important aspect of making an offer is to make sure you are okay with doing some work yourself after closing or paying a professional to make improvements.

However, some properties are not financeable with a standard FHA loan as-is due to their condition. In this scenario, you can finance repairs into your mortgage using the FHA 203k home improvement loan.

On the listing, you will see one of three codes for the home’s condition:

- IN – Insurable by FHA. No repairs needed to qualify for a standard FHA mortgage.

- IE – Insured with Escrow. Repairs under $5,000 are needed, which can be financed using the FHA Repair Escrow program

- UI – Uninsurable. This means you need an FHA 203k loan to bring the home up to FHA standards

If the home requires financed repairs, make sure the home price plus repair budget is within your pre-approved loan amount.

How Much Money Do I Need for the $100 Down Program?

Though the program requires just a $100 down payment, there are additional closing costs. However, HUD contributes up to 3% of the home’s price to help reduce the buyer’s upfront expenses.

Here’s an estimate of costs with the HUD Homes $100 Down program compared to the standard FHA loan for a property not owned by HUD.

| $100 Down Program | Standard FHA | |

| Home price | $290,000 | $300,000 |

| Repairs financed | $10,000 | $0 |

| Down payment | $100 | $10,500 |

| Closing costs | $9,500 | $9,500 |

| HUD contribution | -$8,700 | -$0 |

| Est. Cash to close | $900 | $20,000 |

In this example, the $100 down home requires just $900 to close. But if this person purchased an open-market home with an FHA loan, their cash to close would be closer to $20,000.

Check your $100-down eligibility.

Pros and Cons of the $100 Down HUD Homes Program

Purchasing a HUD home for $100 down can be a practical path to homeownership for many prospective buyers, but this program may not be right for everyone. Here are some of the pros and cons to consider.

Pros

- Low down payment of just $100 compared to other low-cost programs, which require 3% to 3.5% of the purchase price.

- HUD provides up to 3% of the sales amount as closing cost assistance, which can reduce your upfront expenses to just 1% or 2% of the total price.

- FHA interest rates tend to be lower than conventional loans, especially for borrowers without excellent credit.

- The low down payment requirement allows you to save your funds for other expenses like repairs and moving costs.

Cons

- The program only applies to HUD-owned homes, and the number of nearby available properties may be limited.

- Since HUD-owned homes are foreclosures, many have been neglected, and repairs are often needed.

- Buyers will need to meet the minimum eligibility requirements that apply to all FHA loans.

HUD Homes $100 Down Program FAQ

Still trying to decide if the $100 Down HUD Homes program might be right for you? Here are answers to some of the most frequently asked questions

Do You Have to Be a First-Time Homebuyer to Get a HUD Home for $100 Down?

No, you do not need to be a first-time homebuyer to get a HUD home for $100 down. However, you must not have purchased another HUD property within the past two years and be able to meet the eligibility requirements for an FHA-backed loan.

How Much Money Do I Need in the Bank for the $100 Down HUD Homes Program?

You will need $100 for the down payment, plus closing expenses. HUD covers up to 3% of the home’s price in closing costs, though, so you’ll only be responsible for paying the rest, which is typically 1% to 2% of the purchase price.

What Is the Catch to the $100 HUD Homes Program?

There is no catch. HUD wants to offload its foreclosed properties to owner-occupants who will live in them. As such, it offers these homes for $100 down and covers up to 3% of the home's price in closing costs. The only "catch" is that there are currently not many homes available, so buyers who want to use this program must be patient and watch for new listings daily.

Are $100 Down HUD Homes Offered at a Discount?

HUD often offers these homes at below-market prices. This discount, combined with just a $100 down payment requirement and subsidized closing costs, eliminates many barriers for prospective homebuyers. Keep in mind, though, that offers with a $100 down payment must be made at the full asking price.

The $100 Down Program Could Make You a Homeowner

There are not many programs on the market today that offer zero down or close to it. But thanks to HUD’s goal of making homeownership more affordable, many people are buying properties with very little out-of-pocket, using the HUD Homes $100 Down program.