A cash-out refinance lets you convert your built-up home equity into a lump sum of cash. And it could be a fantastic time to do just that. While mortgage rates have crept up slightly in recent months, they’re still lower than they were throughout most of last year, and far below their late 2023 peak.

But who are the best cash-out lenders to work with? Not all providers are the same – some are more likely to offer great rates, a painless application process, and top-notch customer service.

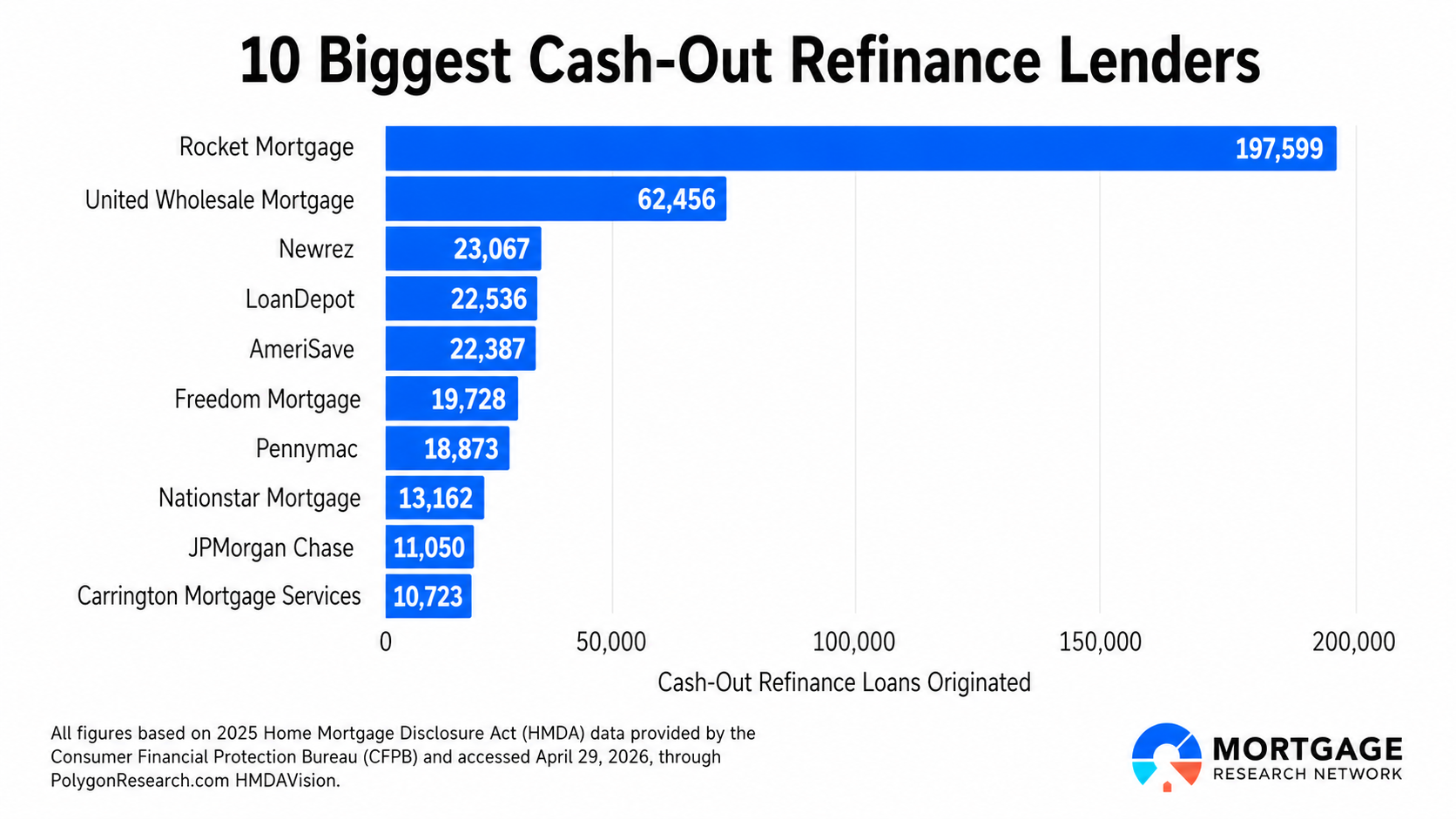

In some mortgage shoppers’ books, bigger is better. That’s why Mortgage Research Network has analyzed the latest Home Mortgage Disclosure Act (HMDA) data for 2025 through Polygon Research's HMDAVision and compiled a list of the ten biggest cash-out refinance lenders by the number of loans they originated in 2025 .

Biggest Cash-Out Refinance Lenders by Loans Originated in 2025

The ten biggest cash-out refinance lenders for owner-occupied homes accounted for nearly 47% of all cash-out refinances last year. These mortgage companies may not provide the lowest quotes in every situation, but they’ve certainly established themselves as the largest cash-out refinance lenders for a reason.

| Rank | Lender | Cash-Out Refinances in 2025 | Market Share |

|---|---|---|---|

| 1 | Rocket Mortgage | 197,599 | 23.77% |

| 2 | United Wholesale Mortgage | 62,456 | 7.51% |

| 3 | Newrez | 23,067 | 2.77% |

| 4 | LoanDepot | 22,536 | 2.71% |

| 5 | AmeriSave | 22,387 | 2.69% |

| 6 | Freedom Mortgage | 19,728 | 2.37% |

| 7 | Pennymac | 18,873 | 2.27% |

| 8 | Nationstar Mortgage | 13,162 | 1.58% |

| 9 | JPMorgan Chase | 11,050 | 1.33% |

| 10 | Carrington Mortgage Services | 10,723 | 1.29% |

1. Rocket Mortgage

Rocket Mortgage is the nation’s biggest cash-out refinance lender, leading the pack by a considerable margin. Their 2025 originations accounted for a whopping 23.77% of the total cash-out refinance market, with over three times as many loans issued as the second-largest lender.

Their secret? It may be the company's position at the forefront of mortgage tech. Their AI-powered Rocket Logic platform utilizes more than 10 petabytes of proprietary data to streamline the cash-out refinance process; the system has reportedly helped Rocket Mortgage reduce closing times by 25% since 2022.

2. United Wholesale Mortgage

Ranking second with around 7.5% of all cash-out refinances, United Wholesale Mortgage (UWM) is a wholesale lender with a nationwide network of independent mortgage brokers. Unlike most other lenders on our list, they don’t deal directly with consumers.

While UWM may be second in the number of cash-out refinances, with 62,456, it remains the largest wholesale mortgage lender in the nation. According to their website, United Wholesale Mortgage funds conventional cash-out refinances with a credit score as low as 620 through their mortgage broker partners.

3. Newrez

Founded in 2008 as New Penn Financial, Newrez offers cash-out refinances nationwide through a network of third-party brokers. It also attracts borrowers through its retail locations and website as a direct-to-consumer lender. In 2025, Newrez closed 23,067 cash-outs across all channels.

Newrez has grown in recent years through industry acquisitions like Caliber Home Loans and Computershare Mortgage Services. Earlier this year, Newrez announced its newest AI initiative: a strategic investment in HomeVision to develop an AI-powered solution to accelerate mortgage underwriting.

4. LoanDepot

LoanDepot is a direct lender that, according to its website, funded a grand total of nearly $26.5 billion in mortgages in 2025. For the year, it was the fourth-largest cash-out provider, originating 22,536 loans.

LoanDepot has boosted its performance through the implementation of its proprietary platform, “mello,” which simplifies the cash-out refinance process by directly verifying employment, income, and assets. The company boasts that mello lets borrowers close their mortgages in as few as eight days.

In addition to ranking 4th for cash-out refinances, LoanDepot ranked as the 10th-largest VA mortgage lender in 2025.

5. AmeriSave

Atlanta-based AmeriSave has financed nearly 750,000 mortgages, totaling $130 billion in home loans, since its founding in 2002, according to the its website.

AmeriSave offers loans in every state except New York and boasts a typical closing time within 31 days on cash-out refinances, of which it completed 22,387 in 2025. The company advertises that it offers cash-out refinances to homeowners with credit scores as low as 620.

6. Freedom Mortgage

Freedom Mortgage works directly with consumers, as well as through a nationwide network of affiliated mortgage brokers. The company is also a major loan servicer, claiming to service more than 2.5 million mortgages, representing a total of over $625 billion in residential loans.

On their website, Freedom Mortgage advertises VA and FHA cash-out refinances for homeowners with credit scores as low as 550. Conventional cash-outs are available for credit scores of 620 and above.

7. PennyMac

Since its founding in 2008, PennyMac boasts having worked with more than 5 million homeowners. When it comes to cash-out refinances, the company ranks seventh, with 18,873 loans and 2.27% of the market last year.

According to their website, PennyMac holds an A+ rating from the Better Business Bureau and has serviced more than $700 billion in overall loans.

8. Nationstar Mortgage

Nationstar Mortgage ranked eighth last year with a total of 13,162 cash-out refinances originated. While the company primarily operated under its better-known Mr. Cooper brand name, Nationstar and the rest of Mr. Cooper Group were acquired by Rocket Mortgage in late 2025.

9. JPMorgan Chase

With a history dating back more than 225 years, JPMorgan Chase is one of the largest and most well-known financial service companies in the United States. While its residential mortgage business accounts for only a small fraction of its overall revenue, the company issued an impressive 11,050 cash-out refinances last year.

In addition, JPMorgan Chase ranked as the largest lender for residential purchase loans over $1 million in 2025.

10. Carrington Mortgage Services

Rounding out the list of the biggest cash-out refinance lenders in 2025 is Carrington Mortgage Services, with a total of 10,723 of these loans completed. The California-based company, which specializes in helping borrowers with challenging credit profiles, reports serving more than 1.8 million customers since 2017, according to its website.

Why Use a Cash-Out Refinance?

A cash-out refinance allows you to replace your existing mortgage with a larger one and receive the difference, minus closing costs, as a lump sum to use however you prefer.

The most common reason borrowers opt for a cash-out refinance is to fund home repairs or improvements, but you can also use your built-up equity to:

- Consolidate high-interest credit cards

- Purchase a second home or investment property

- Pay off an auto loan

- Wrap in a second loan or HELOC balance

- Eliminate student loan debt (you may even qualify for lower rates)

Cash-Out Refinance Programs

Most large lenders offer an assortment of cash-out refinance programs designed to fit different types of homeowners. The three most common that you'll encounter are:

Conventional Cash-Out Refinances

Conventional cash-out refinances follow the guidelines established by Fannie Mae and Freddie Mac. While there's no set minimum credit requirement, some lenders may look for a score of 620 or higher. However, the cost for homeowners on the lower end of the credit spectrum will likely be higher than with other cash-out refinance programs.

Conventional cash-outs let you tap up to 80% of your home's equity.

FHA Cash-Out Refinances

Designed for homeowners with less-than-perfect credit, FHA cash-out guidelines allow you to qualify with a credit score as low as 500. Most lenders, however, have their own higher minimums.

As with conventional loans, an FHA cash-out refinance lets you borrow up to 80% of your property's current appraised value. If your home is worth more than it was just a few years ago, you may be eligible to access a substantial amount of cash.

VA Cash-Out Refinances

VA cash-out refinances are available to current and former U.S. military members with eligible service history. VA guidelines set no minimum credit score, although most lenders will have score requirements ranging from 580 to 620.

With a VA cash-out refinance, you can withdraw up to 100% of your home's current value, although many lenders opt to cap loans at 90%.

Is Now a Good Time to Consider Cash-Out?

The best time to do a cash-out refinance is when you can simultaneously lower the interest rate on your loan. But most homeowners have interest rates much lower than what’s available today.

However, if you need to access a large amount of funds, it may still be worth taking a higher rate on a cash-out refinance. It’s also worth considering a second mortgage, such as a home equity loan or home equity line of credit (HELOC).

Rates are down from their 2023 peaks. If you've purchased your home since mid-2022, you may be able to qualify for a cash-out refinance at a rate comparable to or lower than what you currently have. This is especially true for homeowners who have since significantly improved their credit score or built considerable equity in their property.

Find the Best Cash-Out Refinance Lender

We've covered the ten biggest cash-out refinance lenders by loans issued, but even though they account for almost 47% of all cash-out refis, there are plenty of other great mortgage providers out there. The best cash-out refinance lender for you may even be a lower-volume originator.

All figures based on 2025 Home Mortgage Disclosure Act (HMDA) data provided by the Consumer Financial Protection Bureau (CFPB) and accessed April 29, 2026, through PolygonResearch.com HMDAVision.