Veterans United Home Loans is a registered DBA of Mortgage Research Center, LLC, an affiliate of Three Creeks Media.

If you've been shopping for a home lately, you've almost certainly experienced the frustration of watching mortgage rates move in ways that seem random or inexplicable. One week a rate looks manageable; the next, it's jumped by enough to add hundreds of dollars to your potential monthly payment. What's going on behind the scenes?

Afifa Saburi, a Capital Markets Analyst at Veterans United Home Loans, recently broke it all down on the Real Estate Update podcast, offering a rare inside view of the financial system that quietly shapes what homebuyers pay every month.

The Two Markets That Affect Your Rate Every Day

Most first-time homebuyers think of the mortgage process as a transaction between themselves and their lender. That's true, but it's only half the picture. Saburi explains that there's actually a two-tiered system at work.

"The primary market is the borrower looking to buy a home; they need a mortgage, so they come to a lender," Saburi says. "The thing that connects that whole process to the secondary market is the rate sheet."

Here's how these two markets work in plain terms:

- The Primary Market is what most buyers are familiar with. You approach a lender, they check your credit, income, and other financial details, and they offer you a mortgage rate. That rate sheet is the visible face of a much larger system.

- The Secondary Market is where the real action happens. After your lender originates your mortgage, they typically sell it – often to government-sponsored enterprises like Fannie Mae or Freddie Mac – which then bundle many mortgages together and sell them to investors as mortgage-backed securities (MBS). This allows lenders to keep making new loans rather than running out of capital.

As Saburi puts it: "All of that is determined by supply and demand in the secondary market. There are buyers for mortgage-backed securities, and the MBS market has historically been a very liquid market. That liquidity, the buying and selling of mortgage bonds, is essentially what determines the cost of that rate."

In other words, the rate you receive is not simply a number your lender picks. It's a reflection of what investors in the global bond market are willing to accept on that given day.

Understanding Your Rate: Par, Buy-Down, and Premium

If you've ever wondered why one borrower gets a lower rate than another, or why your lender offered to let you "buy down" your rate, this is the mechanism behind it.

Saburi explains: "The benchmark is essentially the par rate, the rate that would cost you zero. Then you go below that rate, you would have to pay to buy down your rate, and then you could go above to premium, which essentially you get a credit for locking in that rate."

Here's what that means in practice:

- Par rate: The rate at which neither you nor the lender pays anything extra. This is the baseline.

- Below par (buying down your rate): You pay an upfront cost, called discount points, to secure a lower interest rate. This can save money over the long run if you stay in the home long enough.

- Above par (premium pricing): You accept a higher interest rate in exchange for a lender credit, which can be used to offset closing costs. You pay less upfront but more over time.

Which option is best for you depends on your financial situation, how long you plan to stay in the home, and current market conditions. A trusted loan officer can help you run the numbers.

Why Inflation Makes Mortgages More Expensive

One of the most important lessons from Saburi's analysis is how global events and economic forces ripple into your mortgage rate.

Inflation is one of the biggest drivers. When prices rise broadly across the economy, the purchasing power of money falls. For lenders and bond investors, this is a problem: if they lock in a fixed return today and inflation climbs, the money they receive in the future will be worth less than they planned for. To protect against this, they demand higher interest rates.

Saburi illustrated this with a real-world example from a period of rising economic tension: "Historically, when oil prices rise, it translates to higher inflation. The market was like, 'Okay, we're going to have to price in this inflation,' which means a higher federal funds rate, which means higher interest rates."

This chain reaction – geopolitical event, oil price spike, inflation fears, higher rates – can play out in a matter of days. When inflation is high, lenders require higher interest rates to offset the declining value of future mortgage payments. For a first-time homebuyer not watching the financial news, this can feel like rates moved for no reason at all.

The good news is that the relationship cuts both ways. Saburi noted that shortly after inflation fears spiked, the market shifted its thinking:

"Today, it's a different sentiment because the market is saying, 'Yes, oil prices cause inflation, but they could also cause a slowdown to the economy.' If the economy is slowing down, then the Fed is not going to hike... that is resulting in better mortgage rates. Historically, any sort of fear of a slowdown of an economy or recession leads to lower mortgage rates."

For homebuyers, this means paying attention to major economic headlines is not just for Wall Street traders. Those headlines can shift your borrowing costs within weeks.

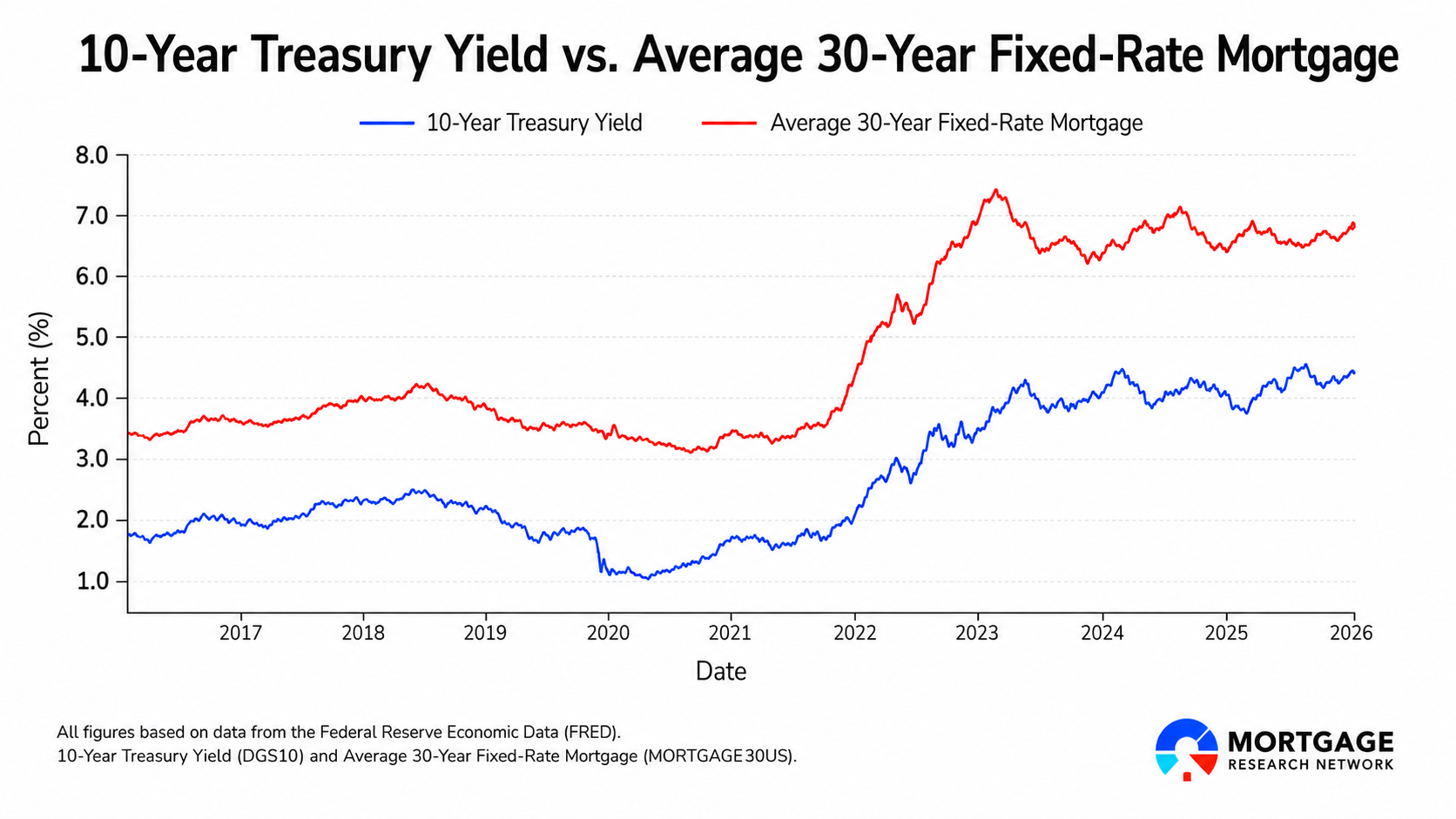

The 10-Year Treasury: The Hidden Benchmark for Your Mortgage

One of the most useful things any homebuyer can learn is the relationship between mortgage rates and the 10-year U.S. Treasury yield. You do not need to be a financial expert to track this number – it is publicly available and updated daily.

Saburi references this relationship when discussing how mortgage spreads behaved during a period of market stress: "Treasury yields, specifically the 10-year, did rise, but mortgage spreads – which determine cost and then feed into mortgage rates – actually got worse than Treasuries did."

Why does the 10-year Treasury matter so much? Since mortgages last longer than shorter-term lending products, they require a long-duration benchmark -- and the 10-year Treasury note lasts about as long as the average homeowner actually holds a mortgage before selling or refinancing.

In practical terms, lenders set mortgage rates based on the 10-year Treasury yield, typically adding 2 to 3 percent on top to ensure that mortgage-backed securities remain attractive to investors.

While mortgage rates and the 10-year Treasury yield often move together, Saburi's key insight is that mortgage rates can sometimes diverge from Treasury yields, particularly when investors become nervous about credit or prepayment risk in the mortgage bond market.

Mortgage bonds carry an extra layer of risk associated with repayment and credit risk – known as default risk – which Treasury bonds do not carry since they are essentially guaranteed by the government. When investors perceive more risk in the mortgage market, they demand a higher return, which pushes rates up even if Treasury yields haven't moved.

For the homebuyer, the practical takeaway is this: keeping an eye on 10-year Treasury yields gives you a reasonable real-time signal for where mortgage rates are heading. If yields are rising, expect rates to follow. If yields are falling, rates may ease – though the movement may be delayed or smaller than you hope.

What Happens When Big Buyers Enter the Market

Saburi highlighted one specific event that had a direct impact on mortgage rates: the announcement that Fannie Mae and Freddie Mac would be permitted to purchase $200 billion in mortgage-backed securities.

"This was a new buyer that had exited the market ever since the GFC [Global Financial Crisis], so them stepping back in and buying these bonds would be a positive for mortgage rates," Saburi explained.

This is a great illustration of basic supply and demand. When there are more buyers for mortgage-backed securities, prices for those bonds go up. Higher bond prices mean lower yields, and lower yields feed into lower mortgage rates for borrowers.

Saburi did add an important nuance: the timing and structure of those purchases matters. "If they were to do it all at once, yes, we would see an immediate big reaction. But it's likely that they will spread that out. It also depends on whether or not the agencies actually hedge those bonds. If they don't hedge those bonds, it would help mortgage rates, but if they're hedging those bonds, then it kind of offsets the benefit of buying."

The big-picture lesson: government and regulatory actions can meaningfully move mortgage rates, but the effects are not always immediate or certain. This is another reason why timing a mortgage decision around waiting for a specific rate target can be a risky strategy.

Why Rates Are So Volatile Right Now

If you have noticed that mortgage rates seem to jump around more than they used to, you are not imagining it.

Saburi described the rapid back-and-forth in vivid terms: "Watching how the market reprices risk – going from thinking we're in an inflationary environment to a recessionary environment in a week's span – is very interesting. And honestly, just watching how resilient the mortgage market has been considering all that's getting thrown at it."

This volatility has real consequences for buyers. High mortgage rates, which can add hundreds of dollars a month in costs for borrowers, have reduced purchasing power for many prospective homebuyers.

One of the most honest things any mortgage professional can tell you is that no one can predict the exact path of mortgage rates. Heightened mortgage rate volatility may present opportunities for would-be homebuyers to take advantage of temporary lows, but on average, rates are expected to remain elevated. Rather than trying to time the market perfectly, smart buyers focus on what they can control.

What This All Means for You as a Homebuyer

Understanding the forces behind mortgage rates won’t give you the ability to predict exactly where they will go. But it will help you make smarter, less reactive decisions during the homebuying process.

The mortgage market is complex, and it can feel like it is working against you. But as Saburi put it, there is reason to appreciate the market's resilience: even when geopolitical shocks, inflation scares, and economic uncertainty hit simultaneously, the machinery that funds American homeownership keeps running. Your job as a buyer is to be prepared, stay informed, and be ready to move when the timing is right for you.