Home loans backed by the United States Department of Agriculture (USDA) let borrowers purchase rural residences with no money down and lower interest rates than many other types of mortgages. However, obtaining a USDA loan requires a few extra steps, including ensuring the property meets all USDA appraisal requirements.

This guide covers everything you need to know about the USDA home appraisal requirements, including precisely what appraisers look for and your options if the home doesn't meet the program's minimum standards.

Key Takeaways

The home you’re purchasing must meet USDA appraisal requirements to be eligible for a USDA-backed mortgage.

The appraisal includes a site visit to inspect and document the home’s characteristics and then market research to establish its appraised value.

Minor problems uncovered during the inspection can be remedied by the seller prior to closing.

Major issues, like a cracked foundation or environmental hazards, may prevent you from using a USDA loan.

The USDA-required appraisal differs from a home inspection, which can provide a more in-depth look at certain aspects of the property.

What Is a USDA Loan Appraisal?

Part of the USDA loan process involves having the property you want to purchase appraised to verify its value and ensure it meets minimum USDA requirements. Your lender will order the appraisal once you have a home secured under contract.

The USDA appraisal process involves two aspects: an on-site visit and market research.

During the site visit, the appraiser conducts a basic evaluation of the property and its features. They also document details of the home, such as its square footage, the number and size of bedrooms and bathrooms, and the quality of the materials used in construction.

The appraiser checks to see that the home is also free of health or safety concerns.

After their site visit, the appraiser researches how similar properties are selling in your local real estate market. By looking at comparable homes that have recently sold and that are currently for sale, the appraiser can estimate a reasonable market value for the home you're buying.

They then submit their appraisal report to your lender with support for their value estimation and details of any deficiencies regarding USDA appraisal requirements.

How Is It Different from a Conventional Appraisal?

Appraisals for conventional loans primarily focus on determining the market value of the home and do not have a pass/fail outcome. In contrast, USDA appraisals establish the home's value and assess whether the property meets specific safety and livability standards. As a result, a USDA appraisal can lead to a pass/fail outcome based on the property's condition.

Are the USDA’s Safety and Livability Standards Hard to Pass?

Most well-maintained homes meet the USDA’s safety and livability standards. The appraisal ensures the property is free from major health or safety hazards, like faulty wiring, structural issues, or problems with the water supply. However, older or neglected homes may require repairs to meet these requirements.

What Happens If My House Doesn’t Pass the Appraisal?

If the property you want to buy does not meet USDA home appraisal requirements, you may still be able to proceed with your purchase. This typically requires the seller to complete the noted repairs or modifications prior to closing, although there may be some cases where funds can be put into escrow for work to be completed after the sale.

Appraisal vs Inspection: What is Required for a USDA Loan?

An independent licensed professional must appraise all homes purchased with a USDA mortgage. The appraiser is required to conduct a basic inspection to verify that the property meets USDA appraisal requirements.

This process is different from a home inspection completed by a qualified home inspector. Home inspections involve an in-depth examination of the property's features and mechanical systems, which can provide peace of mind that the house you're buying is free from significant issues and give you a point to negotiate if it’s not.

Obtaining a home inspection is not required for a USDA loan, but it is usually in the buyer’s best interest to do so.

| USDA Appraisal | Home Inspection |

|---|---|

| Completed by a licensed home appraiser | Completed by a licensed or qualified home inspector |

| Determines the value of the property | Does not assign value |

| Examines electrical and plumbing systems | Inspects electrical and plumbing systems in detail |

| Ensures that heating and cooling systems are functional | Checks the various components of heating and cooling systems and estimates remaining life |

| Verifies other aspects of the home meet basic USDA appraisal requirements | Verifies other aspects of the home meet comprehensive inspector standards |

What are USDA Appraisers Looking For?

What exactly are the USDA home appraisal requirements the appraiser checks during their visit? Here’s a comprehensive list of the guidelines that the property must meet:

Homes must be located in an eligible rural area.

Homes must be modest – defined by the agency as something a low- or moderate-income buyer could afford.

The property must be predominantly residential in use and appearance.

There cannot be any active income-producing buildings such as barns, silos, or other agricultural facilities.

Land cannot be leased or used to generate income, although minor sources of revenue such as a billboard, cell tower, or solar panels may be allowed.

The land value cannot exceed 30% of the property’s total appraised value.

Accessory dwelling units are permitted but not when used as a source of rental income.

Properties must have direct access to a paved or all-weather road.

There should be proper site drainage with no water pooling around the home.

The structure must be sound with no foundational issues.

There should be no apparent structural deterioration, such as cracking in load-bearing walls.

Roofs must be free of leaks and have a maximum of three layers of roofing.

Exterior siding must be free of damage and missing panels.

Crawl spaces must be accessible where necessary.

The home must have access to safe, potable water; wells are allowed but require a water quality analysis.

The home must have appropriate sewage disposal, with septic systems free of visible problems.

Heating systems must be functional and appropriate for the home.

Air conditioning is not required but must be functional if present.

Electrical systems must be sufficient to power the home and free of hazards, such as fraying or exposed wires.

Plumbing must be functional with proper drainage throughout the home.

Hot water must be working and accessible.

There cannot be any evidence of unrepaired termite damage or active infestations.

Homes built before 1978 must be free of chipping or peeling paint.

Stairs and some steps must have appropriate handrails installed.

The property should be free from potential environmental hazards.

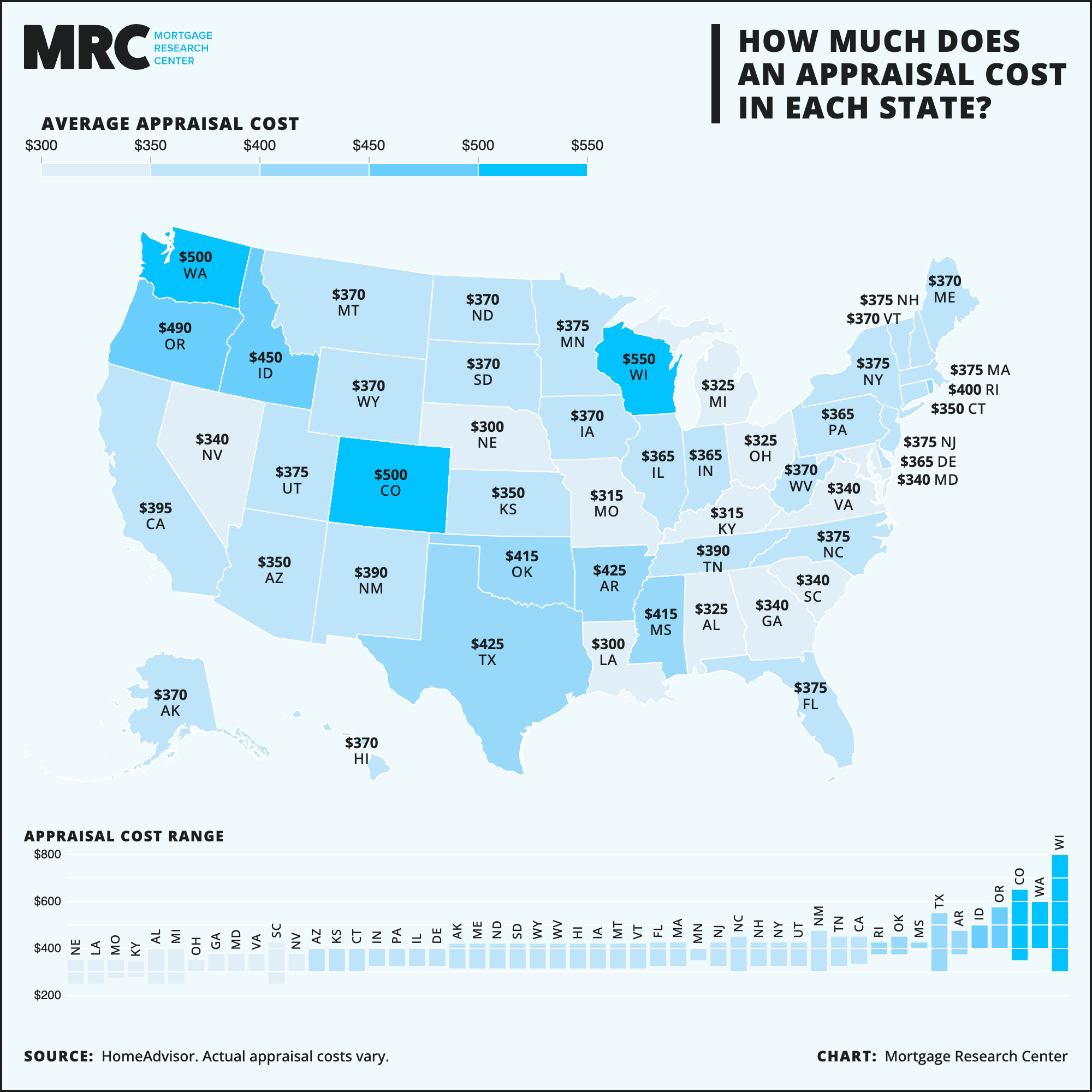

How Much Does a USDA Appraisal Cost?

Since USDA appraisals require the appraiser to conduct a light inspection to verify that the property meets the program’s minimum eligibility requirements, fees are typically slightly higher than a standard appraisal.

Actual costs will vary by location, but most USDA appraisals tend to run between $500 and $900. For USDA Direct loans, which are funded by the agency rather than an independent lender, the appraisal cost is currently fixed at $775.

USDA Appraisal FAQs

Still unsure about the USDA home appraisal requirements? Here are answers to some of the questions that buyers most commonly ask.

Who Pays for the USDA Appraisal?

Homebuyers traditionally pay for the USDA appraisal, although you might be able to negotiate seller concessions to cover some of your closing costs. It may also be possible to obtain closing cost assistance and get reimbursed for the price of your appraisal at closing, so long as it was not paid by credit card or through a short-term loan.

What Happens If My House Is Valued Too Low or Too High?

If the USDA appraisal on your home comes in higher than your contract price, then you're in good shape. Keep in mind, however, that even with a higher valuation, the property can still not meet USDA appraisal requirements.

If the home you want to buy is valued too low, you’ll likely need to negotiate a lower sales price, come up with a larger down payment, or walk away from the deal if neither option is possible.

How Long Is the USDA Appraisal Good For?

Once a USDA appraisal is completed, it stays good for 180 days. This remains true even if you switch USDA lenders midway through the process, as long as the initial lender agrees to transfer the appraisal. Lenders can also extend the appraisal for up to one year with an appraisal update report.

Should I Get an Inspection in Addition to the Appraisal?

You are not required to get a home inspection with a USDA loan, but doing so is likely in your best interest. While your appraiser will ensure the property meets basic USDA appraisal requirements, the process will not be as detailed as a complete home inspection. Hiring a home inspector can help uncover problems that may not be found with just an appraisal.

Does the Home You’re Buying Meet USDA Appraisal Requirements?

USDA loans allow borrowers to buy property in eligible rural areas with no money down, but homes must meet USDA appraisal requirements to qualify. Thankfully, most properties meet these requirements, and those that don't can often be remedied in time for closing.

Sometimes, though, a home may not be eligible for a USDA loan. If you have a property under contract that can't pass the USDA home appraisal requirements, consider applying with a conventional lender who may still be able to fund your loan.