Refinancing can be an effective way to lower your monthly mortgage payments. It can also allow you to use your home's equity to fund improvements, consolidate debt, or meet other cash needs.

Securing a top-notch loan offer, however, can take some effort. That's why we've put together twenty money-saving tips to maximize your savings and help you get the best refinance rates possible.

1. Identify Your Primary Reason for Refinancing

Not all refinance loans are the same – there are a variety of different mortgage products designed for all sorts of needs. To find the best fit, you’ll want to identify your primary reason for refinancing.

Some of the most common reasons that homeowners refinance are to:

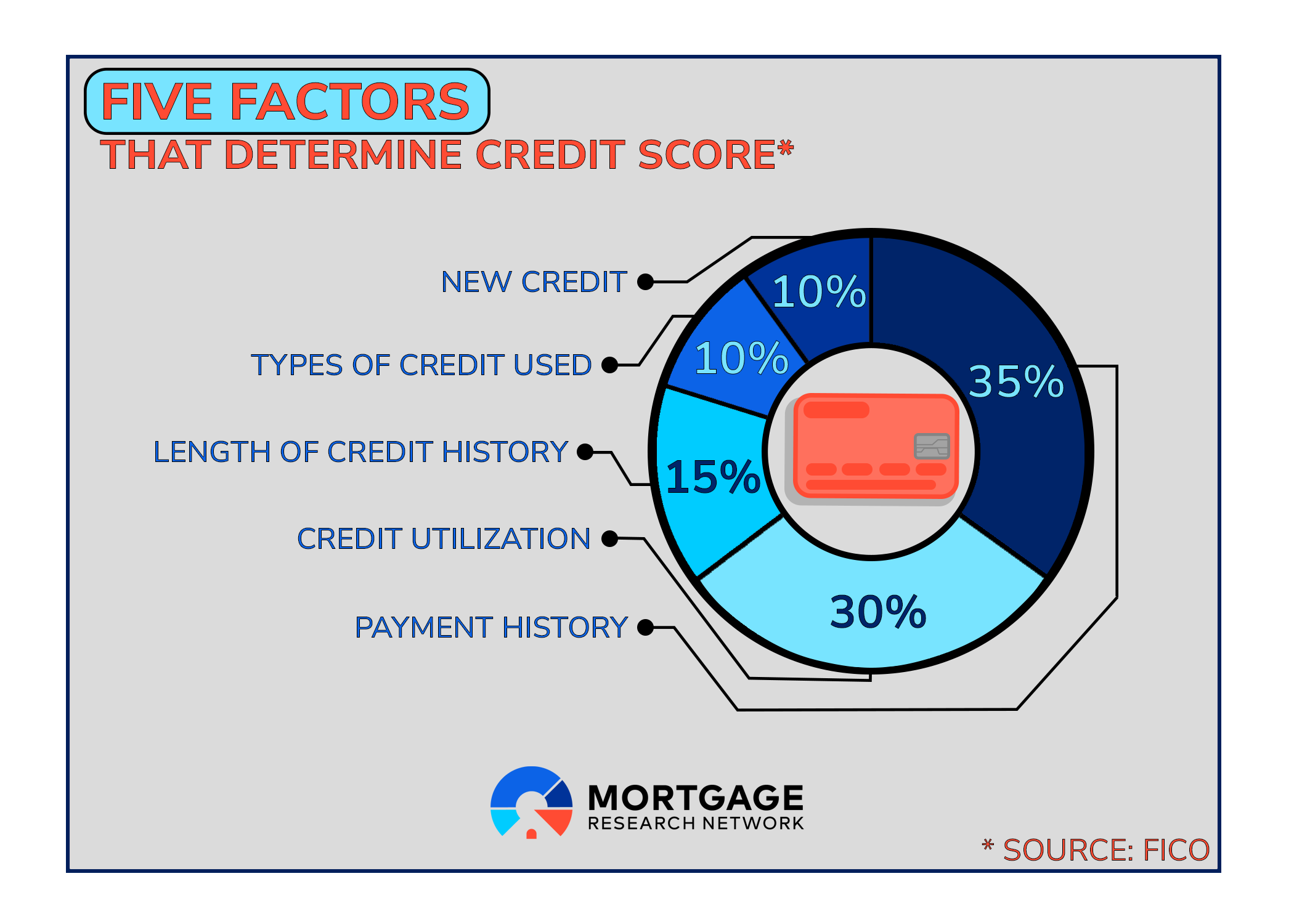

2. Review Your Credit Report for Errors

If it’s been a while since you’ve checked your credit, pull reports from all three bureaus and comb through them for errors. In a 2021 study by Consumer Reports, more than one-third of respondents found erroneous entries on their credit reports.

Thankfully, lenders understand that credit report errors are commonplace. Simply having an error won’t disqualify you from refinancing, but you may need to prove that it’s inaccurate. You can dispute errors on your credit report before you apply, but you may not want to do so if you’re planning to refinance in the near future.

3. Improve Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a key factor in how lenders assess your risk level. DTI is calculated by dividing your debt obligations by your income. For example, if your monthly income is $4,000 and your debt obligations are $1,500, your DTI is 37.5%

Different types of refinance loans have different maximum DTIs. However, with a lower ratio, you’re more likely to be approved.

| Type of Refinance Loan | Maximum Debt-to-Income Ratio |

|---|---|

| Conventional | 45% |

| FHA | 56% |

| VA | 50%* |

| USDA | 41% |

*VA guidelines set no maximum debt-to-income ratio but expect lenders to impose limits ranging from 41% to 50%.

4. Reduce Your Credit Utilization

Your credit utilization ratio is an integral part of your credit score, accounting for 30% of your score under the FICO scoring model. Credit utilization represents the percentage of your total available credit that you’re currently using.

For example, if you have a limit of $25,000 across all credit cards and a current balance of $5,000, your credit utilization is 20%.

As a rule of thumb, you should maintain a credit utilization ratio below 30%. Aim for utilization under 10% for the absolute best credit score and resulting refinance rates.

5. Compare a Minimum of Three Different Lenders

Homeowners frequently jump at the first rate they see that’s lower than their current one. However, this usually means paying more than they need to, even if their payments are less than before.

To ensure you’re getting a good deal on your refinance, compare a minimum of three different lenders. Once you’ve found the best quote, send it to the other brokers or loan officers (as well as your current mortgage company) for them to compete against.

6. Pay Attention to Closing Costs

Interest rates get the most focus, but there’s more to choosing the best refinance than just comparing rates. Pay attention to refinance closing costs, as some lenders will have higher fees than others.

For a more accurate comparison, look at a loan’s annual percentage rate (APR). APRs consider closing costs and other expenses not included in the advertised interest rate.

7. Know Your Break-Even Point

Determining your break-even point is a large part of deciding whether it’s even worth refinancing. This is the amount of time it takes for your cumulative monthly savings outweigh your loan costs.

For example, if refinancing will save you $150 per month and cost $6,000 in closing fees, your break-even point is 40 months – more than three years. If you plan to sell your home or pay off the loan before then, it may not be worth refinancing, regardless of how low the rate is.

8. Avoid “No Closing Cost” Refinances

Many lenders offer a “no closing cost” refinance where you’re not required to pay anything out of pocket. However, in this scenario, lenders either tack the expenses onto your principal balance or charge a higher interest rate in exchange for covering loan costs.

While this can be a practical option for homeowners with limited savings, you should plan to pay the closing costs yourself if you want to get the best possible refinance rate.

9. Negotiate Lower Loan Costs

Remember how we mentioned that not all lenders charge the same amount at closing? When it comes to some of the costs – particularly origination charges like application and underwriting fees – you can negotiate with the lender to reduce their rates.

Not everyone will be willing to haggle on these fees, but asking never hurts. If you’re shopping around with multiple mortgage companies, leverage your best Loan Estimate to negotiate with the other lenders.

10. Purchase Lender Discount Points

Purchasing lender discount points allows you to buy down your interest rate. One discount point costs 1% of your loan balance and, as an estimate, will lower your interest rate by around 0.25%. However, the exact rate reduction will vary by lender.

Before paying for points, calculate your break-even point and make sure it’s worthwhile. For example, if buying $4,000 in points reduces your monthly payment by $75, you would need to keep the mortgage for at least 54 months to come out ahead.

11. Shorten Your Loan Term

If your number one goal is to reduce your interest rate and slash the amount you spend on interest over the life of your mortgage, consider shortening your loan term. Generally, the longer your mortgage repayment period, the higher your interest rate.

In some scenarios, refinancing to a 15-year mortgage can result in rates as much as 0.8% lower than a 30-year loan. Payments will be higher with a shorter loan term, but if you’re substantially reducing your current interest rate, the added costs may be less than you’d think.

12. Eliminate Mortgage Insurance

You’re paying for mortgage insurance if you currently have an FHA mortgage or a conventional loan with less than 20% equity. Eliminating mortgage insurance can lower your monthly payments even more than lowering your rate.

If you have at least 20% equity in your home, refinancing your existing conventional or FHA loan could save you hundreds each month.

See if you’re eligible to eliminate mortgage insurance. Find a lender here.

13. Explore Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) have garnered a bad reputation, but they can be a powerful tool for savvy homeowners seeking the best refinance rates.

ARMs usually have an initial introductory period with lower interest costs than fixed-rate loans. Sometimes, borrowers who plan to sell or refinance again before their rate changes can lock in savings with a low-cost adjustable-rate mortgage.

14. Look Into Bad Credit Refinances

Refinancing can be challenging if you’ve encountered credit problems – especially if your score has dropped considerably since you initially took out your loan. Plus, the lower your credit score, the higher the rates you’ll encounter with most mortgage programs.

Luckily, some bad credit refinance options can offer significant savings compared to standard conventional loans.

15. HomeReady and Home Possible Refinances

Lower-income borrowers who earn no more than 80% of their area’s median income may qualify to refinance through the Fannie Mae HomeReady or Freddie Mac Home Possible programs.

These loan options allow you to refinance with as little as 3% equity while waiving the price adjustments added to most conventional loans. For the majority of homeowners, this equates to lower interest rates. Borrowers with 10% equity or less will also benefit from reduced mortgage insurance costs.

16. Use Equity to Consolidate Debt

Cash-out refinances usually come with higher interest rates than simple rate-and-term refinance loans. Still, using your built-up equity to consolidate outstanding debts could save you big each month.

Refinancing high-interest credit card debt (often at rates of 30% or higher), paying off an auto loan, or consolidating a HELOC or other second mortgage could give you a lower blended interest rate and simplify your monthly bills.

17. Consider a Renovation Refinance Loan

If you’re thinking about cashing out equity to complete repairs or make major improvements to your home, consider a renovation refinance loan.

Rates for rehab loans are generally lower than those for cash-out refinances. Plus, the amount you can borrow is based on your home’s completed value, not its current appraisal.

There’s more red tape in using the money than with a cash-out refinance. But if you plan to spend the funds to enhance your property anyway, the savings from a renovation refinance loan can be well worth the effort.

18. Maintain Sufficient Equity in Your Home

Most mortgage companies will allow you to cash out as much as 80% of your property’s appraised value when refinancing. This is the maximum loan-to-value (LTV) ratio permitted for conventional and FHA-backed cash-out transactions.

However, the more equity you leave in your home, the better the rates they’ll offer you. If you’re borrowing the maximum amount allowed, expect to get quoted higher than if you kept your LTV at 75% or below.

19. Negotiate With Your Current Lender

It’s easier to keep customers than to attract new ones, so if your current lender knows you’re shopping around, they’ll be more open to negotiating refinancing costs.

Refinancing with your current lender can simplify the application process, speed up your refinance, and reduce the amount you’ll need to bring to closing.

Armed with the best estimate from at least three different mortgage companies, ask your lender to beat the competing interest rate and closing costs to retain your business.

20. Lock In Your Low Refinance Rate

Interest costs have come down from their peak in 2023, but there’s still plenty of volatility in the market. Mortgage rates rarely stay consistent from day to day and may be much different when you apply for a mortgage than when you close four to six weeks later.

With a rate lock, you are guaranteed the interest rate you agree to, even if market prices rise by the time your loan closes. But remember: locking in your mortgage rate generally entails a fee or interest increase of its own.

Finding the Best Refinance Rates

If you’re ready to move forward with your refinance, finding the lowest rates is as easy as beginning the application process. By applying with at least three lenders, you can make sure that you’re getting the best refinance rates possible.

To get started, check today’s rates and get in touch with reputable lenders.