While renting comes with lower upfront costs than owing a mortgage, buying a home offers wealth-building opportunities and stability. The right choice depends on your timeline, finances and lifestyle.

The age-old question “Should I rent or buy?” is becoming harder to answer these days. Mortgage rates stuck around 7% according to Freddie Mac, and Bankrate says renting is cheaper than buying in all 50 of the largest U.S. metros. Many consumers who want to buy find themselves on the fence after considering their finances, lifestyle goals and long-term plans.

There’s no one-size-fits-all answer to this dilemma. The choice between renting and owning depends on multiple factors, including your current finances, career stability, family situations and personal preference. Some people love the flexibility and low-maintenance lifestyle of renting, while others enjoy the peace of mind of homeownership and building long-term wealth.

Which one is better for you?

Comparing Renting vs. Buying

Renting and buying each have pros and cons. And depending on your situation and life goals, one may make more sense than the other. Here’s a table comparing different aspects of each choice.

Aspect | Renting | Buying |

Monthly Costs | Generally lower | Initially higher (mortgage, taxes, insurance) |

Upfront Costs | Security deposit, first month's rent | Down payment, closing costs, moving expenses, maintenance |

Maintenance | Landlord's responsibility | Your responsibility |

Flexibility | Easy to relocate | Difficult and expensive to move |

Equity Building | None | Builds over time |

Tax Benefits | None | Mortgage interest, property tax deductions |

Stability | Lease terms, potential rent increases | Long-term stability |

Financial Comparison: The Real-World Costs of Each Option

The biggest factor to consider in the rent versus buy decision is the financial commitment. Buying involves significantly higher upfront costs but offers long-term wealth building, while renting has a lower financial barrier for entry but provides no way to build equity or long-term wealth.

Short-Term Costs: What You'll Pay Initially

Renting Costs:

Security deposit (typically 1-2 months' rent)

First month's rent

Application fees

Renter's insurance

Moving costs

Buying Costs:

Down payment (varies by loan program and personal savings, but minimums are 0%, 3%, 3.5% and 5% for most major loan types)

Closing costs (2%-5% of purchase price)

Homeowner's insurance

Property taxes

Mortgage insurance (if putting down less than 20%)

Moving costs

Utility turn-on fees and immediate maintenance

Adding everything up, think low- to mid-four figures to rent, and low- to mid-five figures to buy.

As Steve Hill, a broker associate with SBC Lending in Los Angeles, explains, "One of my big jobs is just showing people what 5% down, 3% down, 10% down, 15% down, all look like from a payment and down payment perspective, and a lot of times, people end up being okay with a lower down payment."

The myth that you need 20% down prevents many people, especially first-time buyers, from considering homeownership. Hill notes that private mortgage insurance (PMI) can be as low as $60 to $100 per month, which is far less expensive than many people assume.

Long-Term Impact

Owning can build equity and potentially lead to long-term financial gain, even though it comes with plenty of costs you have to cough up initially. Compare this to renting, which has a lower financial threshold but no opportunity to build equity; you’re paying your landlord’s mortgage and building their wealth.

The Renting Scenario

According to RentCafe, average rent in the United States for a 904-square-foot apartment was $1,761 in May 2025.

Renters face consistently rising costs with no equity building. However, they avoid maintenance costs and property taxes, and can invest the money that would go toward a down payment and closing costs.

The Buying Scenario

Homeownership offers equity building through both principal paydown and potential home-value appreciation.

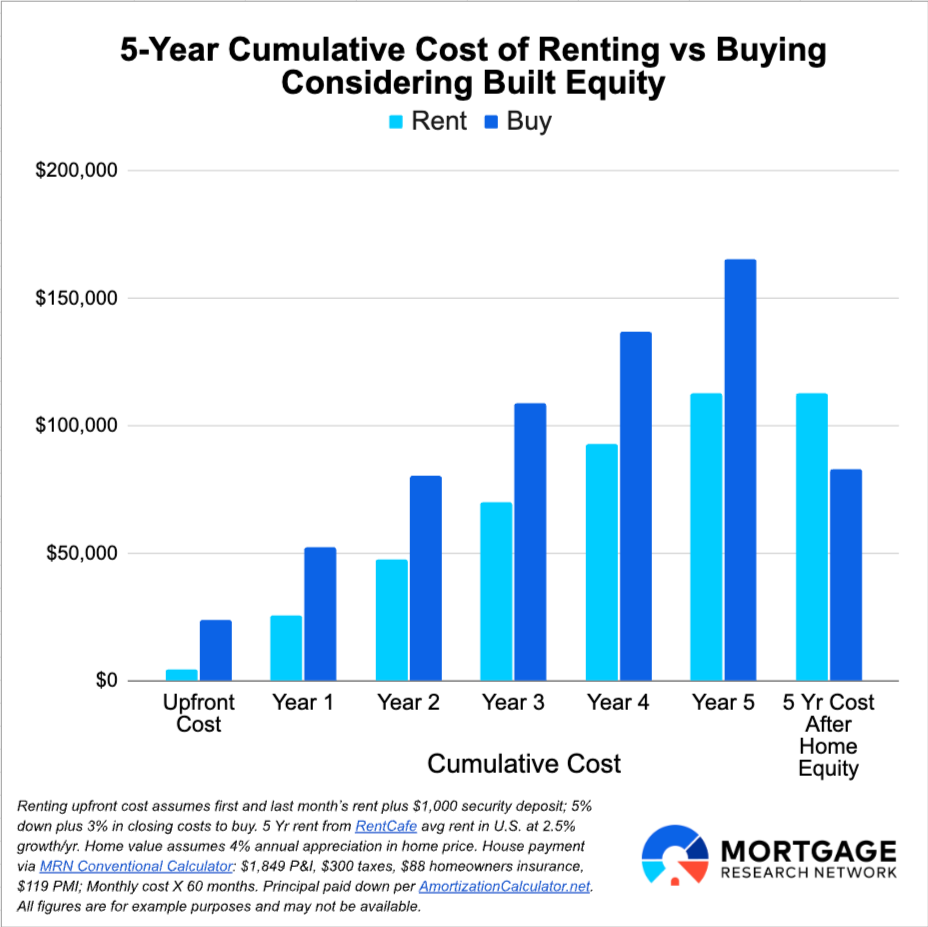

Consider this example: A $300,000 home with 5% down and a 6.75% interest rate would cost approximately $165,300 over five years, including down payment, mortgage payments, closing costs, PMI, homeowners insurance, and property taxes. However, with 4% average appreciation plus principal pay-down, you'd have around $82,450 in equity.

This leaves you with a total cost of buying, including equity built, of $83,000.

In contrast, renting the same property might cost around $112,600 over five years (using average monthly rent of $1,761 with 2.5% annual increases). But there would be no equity to offset the cost.

In the following chart, the upfront 5-year cost of owning is significantly more. But the true cost is less, considering principal pay-down and home price growth.

Rent | Buy | |

Home Price | N/A | $300,000 |

Upfront Costs* | $4,522 | $24,000 |

Monthly Cost** | $1,761 | $2,355 |

5-Year Cost*** | $112,600 | $165,300 |

Home Price Growth**** | $0 | $64,995 |

Principal Paid Down**** | $0 | $17,455 |

True 5-Yr Cost | $112,600 | $82,850 |

*Assumes first and last month’s rent plus $1,000 security deposit to rent and 5% down plus 3% in closing costs to buy. **RentCafe avg rent in U.S. Assumes 4% annual appreciation in home price. ***Calculations via MRN Conventional Calculator: $1,849 P&I, $300 taxes, $88 homeowners insurance, $119 PMI; Monthly cost X 60 months. ****Assumes 4% compounded home price growth per year. Principal paid down per AmortizationCalculator.net. All figures are for example purposes only.

There are, of course, scenarios where the cost comparison falls apart like if home prices drop. Additionally, if you sell the home after five years, expect to lose about 10% of its value in fees, or roughly $36,000 in this case. Buying still puts you about about $30,000 ahead after five years even assuming a sale, but assumptions can be wrong.

Owning Has Financial Benefits, But Shouldn’t Be Considered an Investment

Homeownership provides additional financial options during difficult times, while renting offers less flexibility if you struggle to make payments.

"You could rent out a spare bedroom or rent out the entire place and move elsewhere,” Hill says. “With a rental, you won't always have that flexibility; your landlord may not want to modify the lease, you may have to break the lease to move out."

Hill cautions against viewing real estate purely as an investment; look at the bigger overall picture.

"I'm not even sure if it's the best investment,” Hill says. “Even with prices going up 5% per year, subtracting inflation, it's a nice investment, it's consistent, it's stable... but I also try to dissuade people from viewing their home as an investment."

Lifestyle Flexibility

Outside of the financial considerations, renting versus buying comes down to lifestyle choices and preferences. Some people don’t have the appetite for the responsibilities involved in owning, and that’s OK. Let’s compare how each option looks from a lifestyle perch.

Renting Lifestyle

Renting offers unmatched flexibility for:

Career changes: Easy relocation for job opportunities

Life transitions: No long-term commitment if circumstances change

Travel and mobility: Freedom to move without selling property

Experimentation: Try different neighborhoods or living situations

Owning Lifestyle

Homeownership provides:

Stability: No unexpected rent increases or forced moves

Customization: Freedom to renovate and personalize your space

Community ties: Long-term investment in neighborhood relationships

Predictable housing costs: Fixed mortgage payments (excluding taxes and insurance)

The decision often comes down to your life stage and priorities. Those who think they might relocate within five years may choose to rent, despite the drawbacks.

Responsibility & Maintenance: Who’s Responsible?

Renting: Minimal Responsibility

As a renter, you’re typically not responsible for:

Major appliance repairs

HVAC system maintenance/repairs

Roof repairs

Plumbing and electrical issues

Property upkeep and landscaping

This freedom from having to maintain a home (and the costs involved) can save renters thousands of dollars annually and reduce the stress of unexpected repair bills. However, it also means you’re at the mercy of your landlord’s timeline to make repairs.

Buying: Full Ownership Responsibility

Homeowners must budget for:

Annual maintenance: 1% to 3% of the home’s value annually

Major repairs: Roof replacement, HVAC systems, appliances, water heater, etc.

Unexpected issues: Plumbing emergencies, electrical problems

Regular upkeep: Lawn care, pest control, seasonal maintenance, etc.

Financial experts recommend setting aside at least 1% of your home's value annually for maintenance and repairs, but you may need to save more depending on your home’s size and condition. On a $400,000 home, that's $4,000 per year just for upkeep.

Market Conditions & Timing

Keep in mind that all real estate is local, so what’s happening nationally might not be what local markets are seeing. Consult with a local real estate agent to get a better sense of what’s happening in your area and what times of year offer you the best chance of scoring a better deal on a home.

Here’s a quick overview of national housing conditions:

The U.S. weekly 30-year fixed mortgage rate dipped to 6.85% as of June 5, according to Freddie Mac data. This is only 14 basis points lower than the same week a year ago. Meanwhile, Fannie Mae predicts mortgage rates will end 2025 and 2026 at 6.3% and 6.2%, respectively.

Rent growth moderated to 0.4% year over year in May, with the national median monthly rent at $1,398, up $5 monthly compared to April but down $6 from a year ago, according to the June 2025 Apartment List National Rent Report.

The U.S. median existing-home sales price reached $414,000 in April, up 1.8% from a year ago, according to data from the National Association of Realtors.

Total housing inventory, or homes available on the market, was 1.45 million units at the end of April, NAR reported. That’s up 9% month over month and 20.8% from 1.2 million a year ago.

The current housing market is a mixed bag depending on where you live. While sellers have long held the upper hand, the tide is starting to change in favor of buyers as home-price growth moderates and more inventory comes on the market in places that were once hotbeds of buying activity (Florida and Texas, for instance).

"Home sales have been at 75% of normal or pre-pandemic activity for the past three years, even with seven million jobs added to the economy," NAR Chief Economist Lawrence Yun said in a news release. "Pent-up housing demand continues to grow, though not realized. Any meaningful decline in mortgage rates will help release this demand."

"At the macro level, we are still in a mild seller's market," Yun said. "But with the highest inventory levels in nearly five years, consumers are in a better situation to negotiate for better deals."

Timing your home purchase isn’t an exact science; your timeline likely depends on personal factors, such as a job transfer, a life event or the start of a new school year. Also, timing your purchase to mortgage rate movements is tricky, too, because if you wait for rates to come down dramatically, you might be waiting for a while. Meantime, home prices could go up, Hill says.

“I would never let the decision of whether or not to buy a particular home rest 100% on an interest rate, because based on home price, it's going to be $100 to $200 or $300 a month,” Hill says. “The home that you buy is a much bigger decision."

Personal Goals & Stability

Most housing experts recommend staying in a home for three to five years to make your purchase financially worthwhile. This timeline allows you to:

Recoup closing costs through home-price appreciation.

Build meaningful equity.

Avoid frequent transaction costs.

Making the leap to homeownership also involves evaluating your personal goals and where you’re at in life. It’s also an emotional decision in a lot of ways.

Use a Rent vs. Buy Calculator

Before making your decision of whether to rent vs. buy, use online calculators (such as Freddie Mac’s tool) to compare costs based on your specific situation. Input factors like:

Local home prices and rent costs

Expected length of stay

Down payment amount

Current mortgage rates

Property taxes and insurance costs

Maintenance estimates

While a rent vs. buy calculator can help you crunch numbers and evaluate the costs, it’s merely a starting point in your journey. The best way to determine if you can afford to buy a home and qualify for a mortgage is to reach out to a local mortgage lender who can walk you through your options.

Which Option Is Right for You?

Consider Buying If You:

Have stable income and employment.

Want to put down roots in area for a few years or long-term.

Have adequate emergency savings after down payment and closing costs.

Are comfortable with maintenance and upkeep.

Take pride in ownership.

Consider Renting If You:

Plan to relocate within a few years.

Have unstable income or employment.

Want flexibility over building equity.

Don’t want maintenance responsibilities and costs.

Value freedom to relocate and not be tied to one place.

The Hybrid Approach

Some people benefit from a combined strategy:

Rent while saving for a larger down payment.

Buy a multi-unit property and live in one unit while renting others to help cover costs and build equity.

Rent in expensive markets while owning investment property elsewhere.

Conclusion: Rent or Buy With Confidence

The decision to rent or buy comes with trade-offs for each choice. Take an honest self-assessment of your financial situation, lifestyle priorities and long-term plans.