If you’re buying a home from a relative or someone you have a business relationship with, FHA rules may require a 15% down payment. The good news is that certain exceptions or alternative loan programs could still help you buy with much less upfront.

FHA loans are a popular way to purchase a home with just a 3.5% down payment. However, there are some situations where the down payment may be higher. If you're buying property from a family member or someone you have a business relationship with, it may be considered an identity of interest transaction and require 15% down.

Key Takeaways

An FHA identity of interest transaction is one that involves family members or parties with an existing business relationship.

An identity of interest FHA loan requires a down payment of 15% in most situations.

If you meet one of the FHA identity of interest exceptions, you might qualify for a 3.5% down mortgage.

Other types of loans may have more lenient rules regarding identity of interest.

What Qualifies as an FHA Identity of Interest?

The Federal Housing Administration defines an identity of interest transaction as a sale between family members or in which the buyer and seller have an existing business relationship.

An identity of interest can occur with individuals and businesses, such as when an employee is purchasing property from their employer.

Some examples of an identity of interest could be:

A child purchasing a home from their parent

A business owner purchasing a home from their business partner

A tenant purchasing a home from their landlord

An employee purchasing a home from their employer

When discussing FHA-backed mortgages, the term identity of interest is typically used. Other types of loan deals more commonly refer to this as “non-arm's length transactions.”

The FHA places a greater focus on identity of interest loans because there’s a higher risk of fraud compared to an arm’s length purchase between two strangers. This could be anything from a seller inflating a property's value to a trusting relative, an employer pressuring their employee to purchase a specific home, or even the buyer and seller working together to defraud the lender.

Because of this potential for misconduct and the increased amount of work needed on these types of loans, many lenders may choose not to work with FHA non-arm’s length transactions at all. If you encounter this issue while applying for a loan, your best bet is just to shop around with other mortgage companies.

Implications of an FHA Identity of Interest

The biggest implication of an identity of interest FHA transaction is the increased down payment requirement. While most borrowers can get an FHA loan with just 3.5% down, identity of interest purchases generally have a higher requirement of 15%.

If you're purchasing the property you currently rent and pay a below-market rental rate, lenders may consider that an "inducement to purchase." This could require a larger down payment, even if you qualify for a 96.5% LTV loan. However, FHA guidelines cut out an exception to this rule when you’re purchasing the property from a family member or some other existing relationships.

You can also expect higher scrutiny on your home appraisal since the deal is likely off-market without competition from other potential buyers. In some scenarios, a lender may require a second appraisal to provide additional assurance of the property's true value.

If you are working out a deal to purchase a home in an identity of interest transaction, talk with your lender and go over the specifics to ensure an FHA loan is a practical option in your situation.

FHA Identity of Interest Exceptions

Even if you're purchasing a home from a family member or someone else you have an existing relationship with, you may still be able to get an FHA loan with just 3.5% down. Lender guidelines outline multiple FHA identity of interest exceptions that do not require a 15% down payment. These exceptions include:

Buying the primary residence of a family member

Working for a builder and purchasing a new or model home from your employer

In some cases, purchasing a home from your employer as part of a corporate transfer or relocation program

Purchasing the home you rented and lived in for at least six months

What Is an FHA Identity of Interest Form?

If you're purchasing a home with an identity of interest, it's essential that you let your lender know upfront. To take out your loan, you’ll need to sign the FHA identity of interest form, also referred to as an identity of interest certification.

This form provides an overview of what counts as an FHA non-arm’s length transaction and the resulting down payment requirement. It also asks you to certify whether you have an identity of interest with the property's seller.

Failing to properly disclose an existing relationship on the FHA identity of interest form could be considered mortgage fraud and result in severe civil and criminal penalties.

FHA Identity of Interest Alternative Loans

If you are trying to purchase in an identity of interest situation but do not have the necessary 15% down, you may still have other options. Not all types of loans address these non-arm's length transactions the same way, and other programs typically have more flexible terms than the FHA.

Conventional Loans

Conventional lender guidelines are much more relaxed than the Federal Housing Administration when it comes to identity of interest loans. Apart from some limitations on delayed financing and newly-built houses, you’ll encounter few identity of interest restrictions.

In most cases, to qualify for a conventional loan, you'll need a fairly strong credit profile and a maximum debt-to-income ratio of 45%. First-time homebuyers and those earning no more than 80% of their area’s median income can qualify for a conventional mortgage with 3% down while other buyers need 5%.

VA Loans

VA guidelines do not specify any restrictions on identity of interest transactions. Still, just like with all non-arm's length transactions, some VA mortgage providers may be unwilling to lend on these purchases. Sometimes, you may even be required to make a down payment, even though VA loans are typically 0% down.

Borrowers generally need to be veterans or active-duty servicemembers to qualify for a VA loan. While the program has no fixed credit score requirements, most companies have lender-imposed minimums ranging from 580 to 620.

USDA Loans

The USDA explicitly states that the agency "does not restrict non-arm's length transactions." Guidelines simply require borrowers to disclose any compensation they’re receiving – such as rental credit or sweat equity – to both the lender and property appraiser.

Like with VA loans, USDA loans have no required credit score for its rural development program, but lender minimums commonly range from 620 to 640 although obtaining a USDA loan with a lower score is possible.

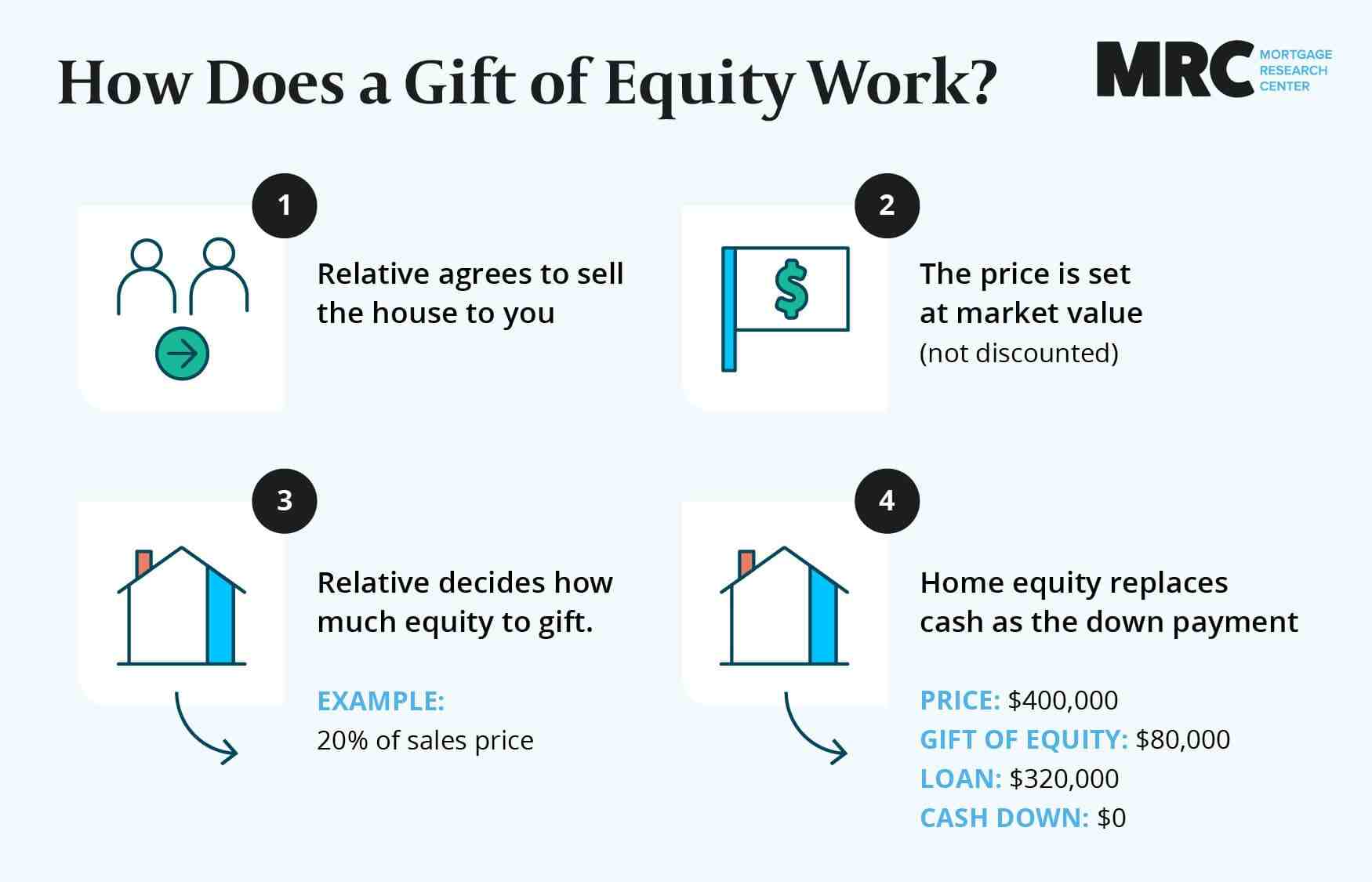

Gifts of Equity

If the home’s seller is willing to gift you equity in the property, you may be able to use this amount to cover some or all of the down payment requirement of your loan. For example, suppose you're purchasing a $300,000 home from your aunt, who offers you a $30,000 gift of equity. This amount will be credited to you at closing, effectively representing a 10% down payment.

Note that gifts of equity must be actual gifts – no kind of repayment or compensation is allowed.

Frequently Asked Questions About Identity of Interest

Still wondering how identity of interest FHA loans work and how your mortgage might be impacted? Here are answers to some other commonly asked questions.

What Is the Maximum LTV for Identity of Interest?

FHA loans are limited to a maximum LTV of 85% when there is an identity of interest. For buyers, this equates to a 15% required down payment. However, you may be able to buy with just 3.5% down if you’re purchasing the home you’ve rented and lived in for at least six months, a family member’s primary residence, or through a corporate relocation program.

Does an Identity of Interest Disqualify You From an FHA Loan?

No, a transaction with an identity of interest does not disqualify you from an FHA loan. You will, however, likely need a larger down payment of 15% and can expect underwriters to give your loan additional scrutiny.

What Is the FHA 85% Rule?

The FHA 85% rule is a reference to the maximum LTV on identity of interest loans. This rule means when there is a familial or professional relationship between a borrower and a home’s seller, FHA-backed mortgages are limited to 85% of the property’s appraised value.

Bottom Line on Identity of Interest FHA Loans

Because of the potential risks associated with identity of interest transactions, the FHA requires borrowers to come up with an increased down payment of 15% in most cases. However, there are exceptions to this rule, but other types of mortgages may sometimes provide more practical alternatives.

To find out how much you need to put down, both with an FHA identity of interest loan and through other programs, apply with an experienced and reputable local lender.