Mortgage Delinquencies Fall to Lowest Level of Pandemic, CoreLogic Says

The share of Americans who hadn’t paid their mortgages on time in July fell to the lowest level since the start of the pandemic, according to a CoreLogic report released on Tuesday.

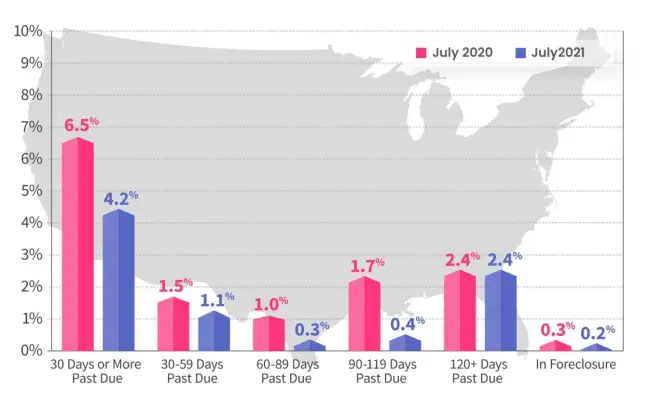

About 4.2% of all mortgages in the nation were in some stage of delinquency, meaning 30 days or more past due, in a tally that includes loans in forbearance, compared with 6.5% a year earlier, the report said. It was the lowest level since March 2020, the beginning of the Covid-19 pandemic in the U.S.

All U.S. states posted declines in July, led by a 3.9% drop in New Jersey, a 3.5% retreat in Florida, and a 3.3% decrease in Nevada, CoreLogic said.

Even if homeowners in forbearance aren’t able to become current on their loans, the nation is likely to avoid the type of foreclosure crisis seen in the wake of the 2008 financial meltdown, said Frank Nothaft, CoreLogic’s chief economist. Almost 10 million American families lost their homes to foreclosure between 2006 and 2014 in a tally that counts forced evictions as well as short sales in which lenders agree to let homeowners sell properties at a loss.

The difference this time is the amount of home equity held by most mortgage borrowers, Nothaft said. After the Federal Reserve began buying bonds in March 2020 to support the pandemic economy, mortgage rates tumbled to the lowest levels on record and home prices surged.

In May, the median U.S. home price increased at the record pace of 24% from a year earlier, according to the National Association of Realtors. In June, the annualized gain was 23%, in July it was 18%, and in August the increase was 15%, NAR said.

Between the increase in home values and the shortage of properties on the market, any borrower who can’t find a way to become current on their home loans after exiting forbearance should be able to sell, Nothaft said.

The average homeowner gained $51,500 of home equity in the past year as the value of their real estate rose, Nothaft said. That’s five times the average annual increase, he said.

“Even if loan modification or income recovery is unable to help delinquent homeowners become and remain current on their payments, the double-digit rise in home prices may help them avoid a distressed sale,” Nothaft said. “Homeowners with substantial home equity are far less likely to experience a foreclosure sale.”

The CARES Act passed by Congress in May 2020 gave homeowners with a government-backed loan the right to up to 12 months of forbearance – meaning a pause in loan payments – if they had experienced economic hardship because of the pandemic. Mortgage servicers were banned from sending negative data to credit reporting agencies and were not allowed to begin foreclosure proceedings.

In February, the Biden administration provided up to six additional months for some borrowers who entered forbearance on or before June 30. That means all Americans will have exited forbearance by the end of the year.

The government has laid out options for mortgage servicers to follow to bring mortgage holders current without creating an economic shock for families, such as rolling the past due amount into a junior loan paid off when the home is sold.

Kathleen Howley has more than 20 years of experience reporting on the housing and mortgage markets for Bloomberg, Forbes and HousingWire. She earned the Gerald Loeb Award for Distinguished Business and Financial Journalism in 2008 for coverage of the financial crisis, plus awards from the New York Press Club and National Association of Real Estate Editors. She holds a degree in journalism from the University of Massachusetts, Amherst.