To save for a down payment while renting, create a budget, find ways to reduce your rent, earn extra income, and cut expenses.

I remember when my wife and I bought our first house. Our oldest daughter was about to turn one-year-old, and we didn’t have a lot of extra money. We were just kids back then, really. But it was a big dream of ours, so we got creative about saving money. We liked the places we rented, but there was so much more we knew we could do with our own home. The day we moved in as homeowners was one of the proudest moments of my life.

As a mortgage broker and lender for over 22 years, it’s always amazing to me to see the unique strategies that so many of my clients have used to cut their expenses and bring in extra income to save for their first homes.

But I get it; saving for a home can be a huge challenge while you’re renting these days. Life is expensive, and it can be hard to set aside money when you’re already struggling to make your bills every month as it is.

The average rent-to-income (RTI) ratio was 28.1% in the first quarter of 2025, which is a slight improvement from its record high in 2022. But it still means that people are spending more than a quarter of their income just on rent. Add in other common expenses like energy bills, student loans, auto insurance, healthcare, transportation, and groceries, some of which have increased significantly in the last few years, and it’s not an easy time to save.

Let’s face it. It takes real discipline and careful planning to save for a home when you’re renting, especially if you live in a high-rent area. Still, I’ve seen determined clients do it time and time again. When they’re handed the keys to their first home, they never regret those short-term sacrifices. Experiencing the dream of homeownership for the first time is powerful and life-changing.

If it feels impossible, I promise you, it’s not. Not every idea below will fit your situation, but these 8 steps will get you on the right path to saving for your first home purchase while you’re renting.

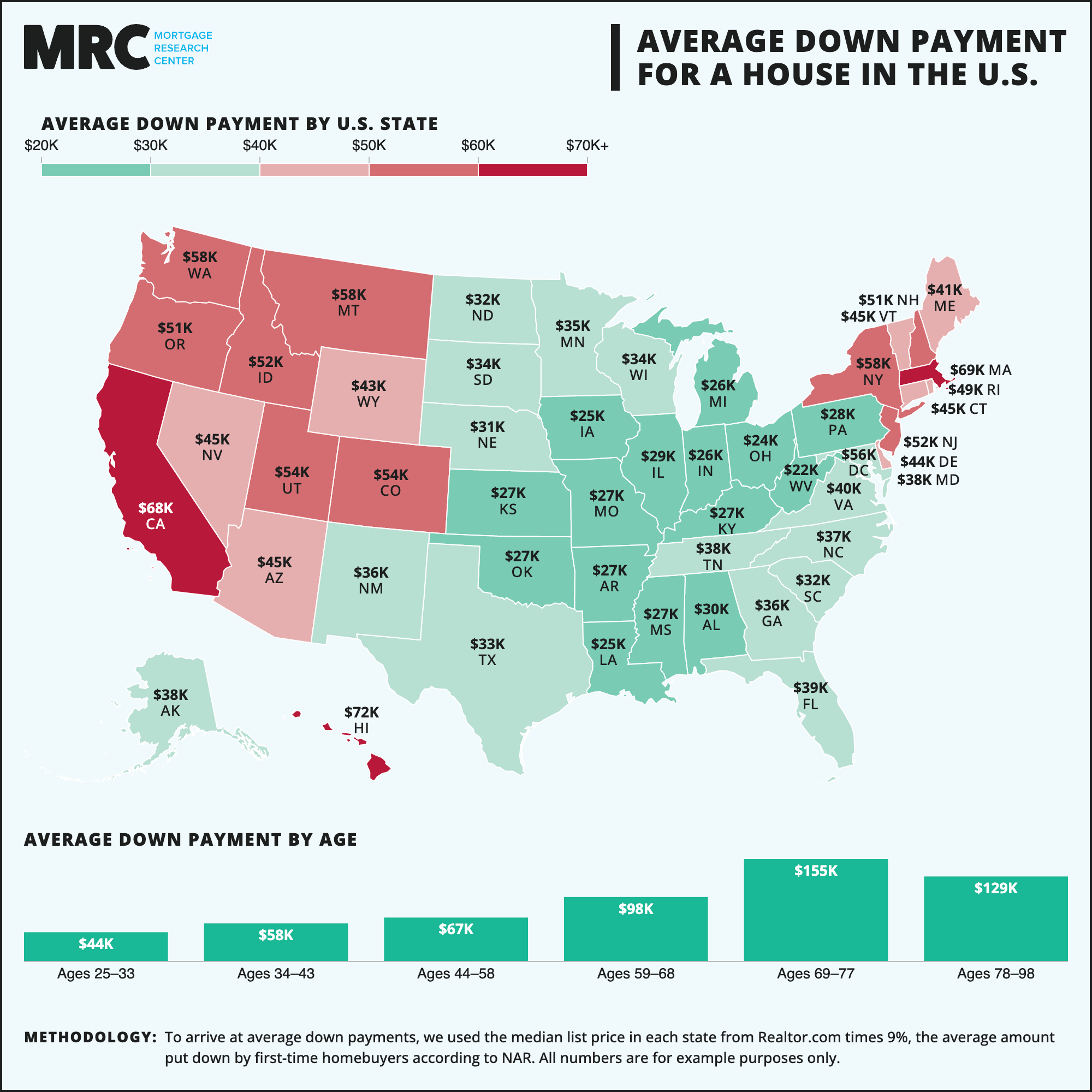

1. Set a Goal for Your Savings

The first step on your home buying journey is to figure out how much you want to save. The average first-time homebuyer down payment in 2024 was 9%. But you don’t have to put down that much if you don’t have the funds available.

Depending on the type of loan program you go with, your upfront costs can be different when it comes to covering your down payment and closing costs:

Conventional: A first-time homebuyer can usually qualify for as little as 3% down, and in some cases, less, if they qualify for a special lender program.

FHA: 29% of first-time homebuyers go with this type of loan and the minimum down is 3.5%.

VA and USDA: These programs have very specific eligibility requirements, but if you meet them, you can get into a home with no money down at all (and only closing costs to take care of).

Keep in mind that everyone is coming from a different starting point. Some things to think about:

Do you have any money saved already, or are there funds you could tap into?

Is there anyone who could help you with gift money towards a home purchase?

What are your current debts, rental costs, and income?

Are you barely scraping by or do you have some cushion to shuffle around a few priorities on a temporary basis?

Do you think you might be in a situation where you could qualify for a special loan program or buyer assistance to help you reduce the amount of your savings goal?

How you answer these questions will give you an idea of what to expect when it comes to the price range of the home you can afford and how long it might take you to build up your savings. This is where working with an experienced loan officer who uses online calculators will help you come up with a realistic home savings goal.

2. Create a Budget

Once you have a number in mind, you’ll want to get to work on your budget so you can identify ways to boost your savings right away. Also, don’t let that word, budget, scare you. It doesn’t have to be this big, terrible, restrictive thing. Think of it as the opposite. It’s a key factor on your roadmap to freedom, and a path to your future.

So, what’s the best way to get started on a budget? Search on your phone for the top-rated budget apps or try exploring YouTube to find out how to set up an old-fashioned budget spreadsheet. Don’t worry about getting too far into the weeds. You only need to know two main things:

Your total monthly income, which is everything you earn.

Your total monthly expenses. Include fixed bills like rent and car payments, and look back over the last couple of months to add up your average spending on other expenses like groceries, dining, and entertainment.

Once you see exactly where your dollars are going, you might be shocked to find out you’re spending way more than you thought on certain categories like dinners out, subscriptions, or other areas. Those discretionary categories are where you can do some trimming.

Some ideas:

Scale back your nights out to a couple of times per month instead of twice per week.

Shop around and negotiate rates with cell phone carriers and insurance providers.

Change your grocery shopping approach. Stick to a specific dollar amount each week and put a pause on random spending.

Watch out for those Uber Eats and Door Dash food delivery costs. They can add up quickly. Instead, invest in a crockpot, Instant Pot, or get a pressure cooker on Amazon. Find 5-ingredient or super simple recipes to throw in before your day begins so dinner is ready to go in the evening.

What About High-Rent Areas?

If you’re living in a high-rent area, it can feel like you’re running uphill. A recent 2025 Elliman Report shows that renters in New York City were paying a median rent of $4,571, a record high.

Renters dealing with exorbitant costs might have to consider moving somewhere with lower rents, or make major lifestyle changes if they are serious about savings for a home.

Some ideas:

Consider getting a roommate to share expenses. If you’ve got a room in your apartment that you could sublease to somebody (and if it's OK with the ownership), that could be a great way to reduce your monthly rent.

Moving back in with your parents. This isn’t possible for everyone, but it’s a creative strategy that could help you meet your savings goals at a much faster rate. If they have the space and it won’t harm your relationship, it might be worth a conversation.

Negotiating rent. If you rent in a private home, could you offer to take on some maintenance tasks for a reduction in your rent?

Temporarily moving to a less expensive area. Brainstorm the pros and cons of this approach to decide if it’s worth doing.

Some of the above strategies might be out of your comfort zone, but shooting for big goals isn’t always easy. It may cause you some temporary discomfort, but when you reach your savings goal, you’ll be glad you stuck your neck out and made the necessary sacrifices.

3. Open a Special Savings Account

If you are manually transferring leftover funds into a savings account, it’s not likely that you’ll be successful. The key to building savings is to be consistent over time and leave the money alone, so it can grow.

So what’s the best way to do that?

Open a high-yield savings account (HYSA), keep it separate from your regular bank, and automate a set amount or percentage of your income into that account every paycheck or each month.

Automating it means you won’t notice it, and as a result, you’ll be less likely to touch the money. HYSAs also help you earn some decent compound interest to accelerate your progress. Earmark this account for your home purchase only, and make sure to keep it separate from your emergency fund, or other savings accounts.

Save the high-risk investing in the stock market for another time, when you have extra money to invest and have the means to hire a qualified advisor.

4. Find Ways to Earn Extra Income

Though you may make a set amount at your job, there are other ways to increase your income that you may not have thought of, like these:

Starting a side hustle. Drive Uber or Lyft, buy items for low cost at a thrift store, fix them up and then resell them on Facebook Marketplace, or use your knowledge and skills to make things with your own hands and sell them online.

Ask for a raise. If you can show specific ways you’ve added value to your job position, you could make a good case for a pay raise. If your boss says no, ask what you could do to earn one in the next 6 months and set some goals to go above and beyond and try again. Just be sure to base it on the value you’ve added to the company, not how much you need it. That’s much more effective! Or if you have the type of job that offers overtime, let your supervisor know that you'd like to pick up extra shifts for a while. This isn’t a long-term solution, but a temporary one, and it’s nice to have the option available.

Sell your stuff! Go through every area of the home you’re renting, and see what you have that could be worth something—that you don’t mind getting rid of. A lot of us have way too much clutter, and we've forgotten what we even own. See what the going rate is on Facebook Marketplace or eBay. Or, if you have larger assets like cars, boats, or RVs that can be sold, those could rapidly reduce the amount of time you need to hit your savings goal.

5. Cut Major Expenses Wherever You Can

While smaller budget cuts do add up, taking a pause on the big-ticket spending makes even more of an impact on your savings. If you're used to vacationing a few times a year, switching to budget-friendly travel or cutting down your trips will help a lot.

Also, make sure to look at your transportation. Can you downgrade or sell your car? If you’re in a big city, will switching to public transportation at least a few days a week help you save on gas and tolls?

It’s okay to start saying no or scaling back on some things. You can politely decline if you’re invited to a wedding or event for someone you aren’t close to and you know it will involve extra expenses. Or make the choice to go, but give a thoughtful card instead of buying a gift, and wear something you already own. You could also pass on those playoff tickets and get some friends together to do a watch party with potluck game-day food instead.

If you have high-interest debt, a consolidation loan can help you lower your monthly payments, save on interest, and free up extra funds to put into savings. I recommend checking with your financial advisor before you move forward on this, though. Debt consolidation loans can be tricky and confusing, and people can get taken advantage of.

6. Use Windfalls Wisely

People rarely think of planning for windfalls, but it’s crucial that you do. Without a plan in place, it’s easy to forget your goals and priorities, and before you know it, the money slips through your fingers, and it’s gone.

Aside from consistently automating your savings, the second best way to save is having a plan for windfalls. Whether you get a tax refund, a work bonus, or a monetary gift, having a rule in place on how to allocate “found money” can help you avoid spending it all haphazardly.

Decide now and commit yourself to putting a percentage of every windfall straight into your home savings fund, while still leaving some cash to enjoy.

7. Stay Motivated and Track Your Progress

Saving for a home can take several months or a few years, depending on your situation. Celebrating (without going too crazy) when you reach mini milestones along the way can help you stay motivated.

If you meet or exceed your monthly goal for three months straight, allow yourself a small splurge like seeing a concert, going for a massage, or going out to your favorite restaurant.

8. Remember—This Won’t Last Forever!

If you’re at the beginning of this journey, it might feel like you have to make sacrifices for the rest of your life. That’s overwhelming, and it can tempt you to want to give up. But I promise you, once you start seeing savings build up, you'll get momentum going, and it won’t feel as difficult. Keep your savings goal in front of you where you can see it every day, and stay disciplined in working towards it, even when you have setbacks.

One day, you’ll look back when you’re in your first home, and you’ll be so thankful you stuck with your goal and made your dream a reality. When you’re a first-time homeowner, this amazing thing happens where you start to build equity and things begin to feel a little easier. While rents will unfortunately continue to go up for everybody else, your mortgage payment will stay fixed (and hopefully, your income will increase, too).

Eventually, interest rates might dip, and you can refinance. Or maybe down the road you can sell and use your home-value profit toward a lower-cost mortgage on your next home.

I remind my clients regularly that homeownership is one of the best wealth builders out there. You just have to get past that first major hurdle—and that’s saving and qualifying for your first home. Once you do, and especially if you continue with the strong financial habits you built while you were saving, you can set yourself up for a lifetime of happy homeownership.