Understanding the various aspects of the purchase agreement allows buyers to manage risk, negotiate effectively, and move from making an offer to closing with confidence.

A purchase agreement is the contract that spells out the terms that the buyer and seller agree to in a real estate transaction. It’s sometimes referred to as a purchase and sale, a purchase contract, or a real estate sales contract.

This contract will contain the property address and description, the purchase price, and the closing date. It also includes key terms and conditions of the sale, including any contingencies, clauses, or riders to the contract. Those details can be almost more important than the boilerplate contract.

In New York City, the part of New York where I practice, attorneys draft the contracts of sale. As I tell my clients, I am not an attorney — but I can direct you to the things you’ll need to think about in your purchase agreement.

Purchase Contract Quick Definitions

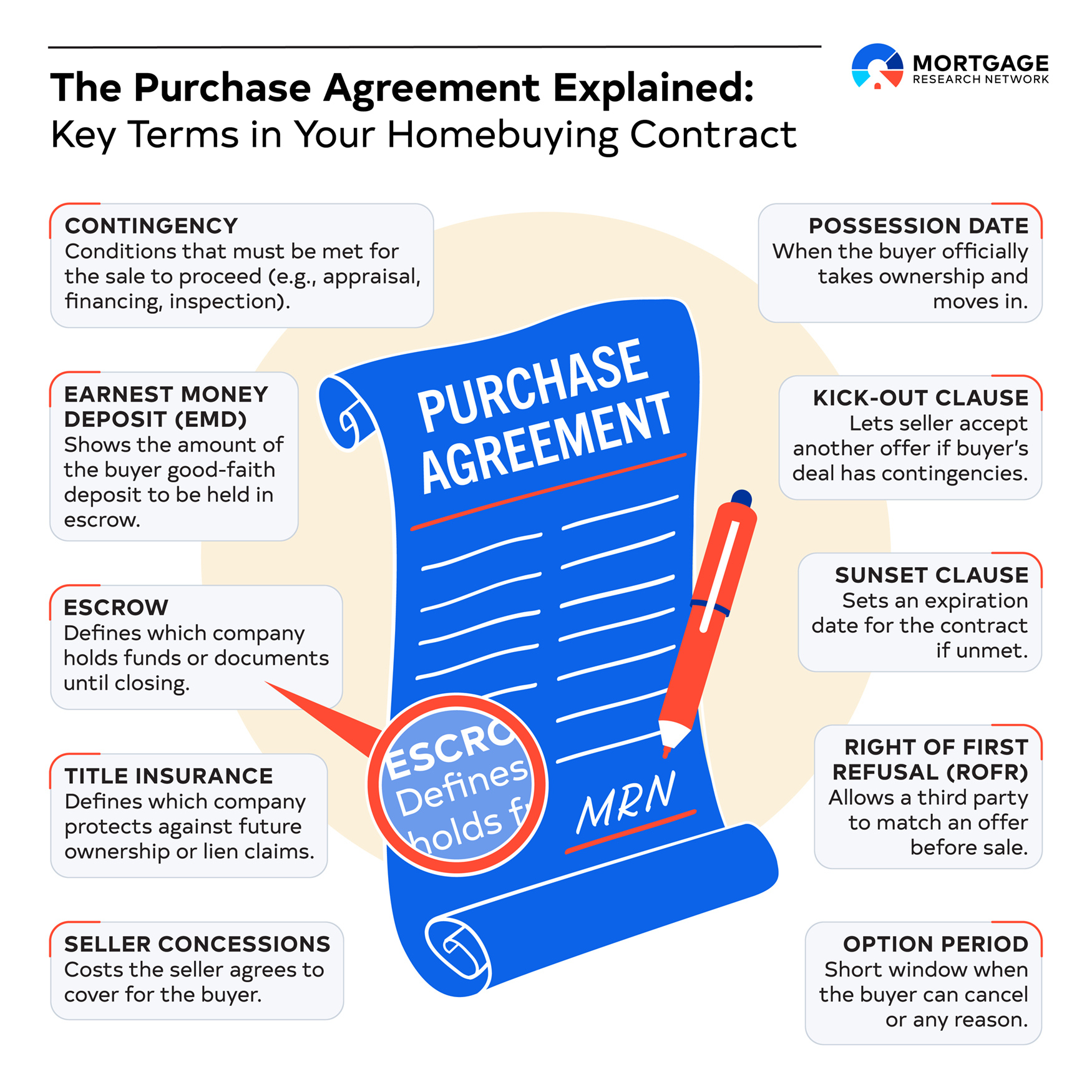

Contingency – Conditions that must be met for the contract to proceed (e.g., financing, inspection).

Earnest Money Deposit (EMD) – A buyer’s deposit to show good faith; held in escrow.

Escrow – A neutral third party holds funds/documents until closing conditions are met.

Title Insurance – Protects against future legal claims on the property’s ownership.

Seller Concessions – Costs the seller agrees to pay on the buyer’s behalf (e.g., closing costs).

Possession Date – When the buyer takes legal and physical possession of the home.

Kick-Out Clause – Allows a seller to accept another offer if the current buyer has contingencies.

Sunset Clause – Common in pre-build sales; sets a time limit for contract fulfillment.

Right of First Refusal (ROFR) – Gives a third party the option to match an offer before a sale proceeds.

Option Period (used in states like Texas) – A window when the buyer can back out for any reason.

General Homebuying Definitions Mentioned in the Contract

Appraisal – An independent property value assessment; tied to financing and renegotiation.

Closing Costs – Fees paid at closing; may include lender fees, title insurance, and taxes.

More About the Terms Every Buyer Should Know

Contingencies

Contingencies are conditions that need to be met before the contract can be legally binding.

If the contingency isn’t met, you can back out of the purchase agreement. The wording of a contingency is very important, and if you misunderstand what it says or otherwise don’t fulfill it properly, it’s going to cause you some pain.

There are several different types of contingencies:

That the home appraises for at least the sale price

The inspection doesn’t reveal significant issues

The title is clear

The financing goes through

There might even be a home sale contingency, where the home sale depends on whether the buyer’s home sells first. If it doesn’t, the deal falls through.

Earnest Money

Earnest money is like a deposit that the buyer puts down to demonstrate that they’re negotiating in good faith. The money goes into an escrow account, and when the deal is complete, it gets applied to the buyer’s closing costs and/or their down payment. If they back out, they lose the money. The exception is if their reason for backing out is covered by a contingency.

Closing Date & Possession

The third part of the contract spells out what is basically the transfer of ownership from the seller to the buyer. This includes things like the closing date, which is the date the sale is settled, and the possession date, which is when the buyer can move in and take possession of the home. These can be the same date, or they can be two different dates, depending on the needs of the buyer and the seller.

Specialized Clauses That Matter

Beyond the basics of the purchase contract, you may need more detailed clauses and contingencies to protect both parties.

Financing Contingencies

When you are talking with your attorney or your Realtor, make sure that the language in your agreement reflects conditions of your financing. You need to know what things you need to do (or not do!) as you're getting closer to the closing. Like, please don't change jobs. Don't go out and buy a car. Those are things that are going to materially affect your financing, and that could have an effect on your ability to close the deal.

I joke about it, but I did have a transaction where my clients were financing with a large bank. I was a little skeptical from the beginning, because one of the buyers had just switched jobs. Lo and behold, we got closer to closing, and there needed to be additional money to be put down. And so the buyers scrambled, and liquidated some things, and got a little help from their parents. And then the bank still said they wouldn't fund the loan. So we had to switch banks very quickly at the last minute.

The irony of it is that the other of the pair of buyers in the transaction worked for this bank. When these people bought their next property, they did not even think about going to that bank for financing, even though the buyer still worked there. It just wasn’t worth the hassle.

Title, Survey & HOA Clauses

Your purchase agreement may contain clauses relating to the title. Clear title means the property is free of liens and encumbrances. Sometimes people do work, and they don't close out permits, and then there’s a lien on the property. That's a big one. Any changes or modifications that may have been completed, you want to be sure that those are properly accounted for.

There may be a survey clause in the purchase agreement. Survey clauses give the buyer the right to obtain a formal survey on the property, which lets them confirm boundary lines and any easements or encroachments they need to be aware of.

Then there are HOA clauses, which allows the buyer to review the documents of the homeowners association before they buy the property. Everyone’s heard an HOA horror story; this clause gives buyers a way to see what they’re in for before they purchase.

Sunset and Kick-Out Clauses

These clauses put a timer on the transaction. They are meant to keep the seller’s options open.

With a sunset clause, there’s an expiration date on the agreement. If the conditions aren’t met by that date, the agreement expires.

A kick-out clause allows the seller to keep showing the house after receiving an offer with contingencies. You might see this with offers that have a home sale contingency; this clause lets them “kick out” the offer in favor of a later offer with no contingencies.

Right of First Refusal (ROFR)

As someone who works all the time with condo and co-op boards in New York City, I see a Right of First Refusal clause frequently. The way that condo association bylaws are written is that the condo board has the right of first refusal. It's generally pretty rare for condos to exercise that right because they essentially have to step into the transaction and meet all the terms, price, and everything else that the original buyer and seller agreed to.

Common Pitfalls & How Experts Advise Buyers

One of the challenges to homebuying is that there are so many nuances and steps in the process. It's really important to ask as many questions as you can of all of the professionals who are involved in the process with you. If they're not willing to answer your questions, maybe you're working with the wrong people.

One of the most common pitfalls is not understanding the terms of your purchase agreement. Another is not understanding when a closing is going to happen, and what you need to do for the closing.

It's really important to ask as many questions as you can of all of the professionals who are involved in the process with you. If they're not willing to answer your questions, maybe you're working with the wrong people.

Avoiding Trouble With a Walk-Through

Never, ever skip a walk-through before closing. Oh boy. Do not, do not skip the walk-through.

I like my clients to do a walk-through the day before or the day of closing if possible. Say you're doing the walk-through three days before and something goes wrong the morning of the closing. Then you don't discover whatever it is that’s wrong until you're moving in. There's all of this back and forth trying to clear it up. Whereas, if you're doing the walk-through the night before or the morning of the closing and an issue comes up, then sure, your closing is going to take a little longer, but you'll be in a better position to resolve the issue.

I have my clients walk through before the contract. We test to make sure things are working, so that we know at the time of the contract everything is, in fact, working. Then, if we go to the walk-through before the closing and things are not quite working, we have a baseline that something went wrong at some point.

Note the Warranties

When you are buying from a developer, it’s important to understand your warranties. This matters for appliances, sure. But the big potential costs are when substantial defects come into play. That happens a lot in New York, whether you're buying in a new development, or if you're buying a resale. You see things that may come up in those first couple of years that a building is operational. If there are issues, the original sponsor will have the responsibility to address them.

Getting the Best Purchase Agreement Terms

There are a few strategies I find to be effective for negotiating successful deals.

Find Their Motivation

I often like to see if we can understand what the other party’s motivations are. One of my favorites is finding out when and where they're moving to. I have had clients who will almost always accept a lower offer if there's flexibility on timing for what they need to do and when they need to move. If someone will give them a little bit longer of a closing timeline, and it aligns with the needs of the client, then they would almost always accept that slightly lower offer.

Be Flexible on Timing

I think timing is one of the biggest strategies, because one of the biggest stressors is the actual moving process, moving from one place to another. So if we can, I like to eliminate the need for a client to live somewhere else temporarily, and then move their things into storage, and then out of storage, and then move them into a new place.

Avoid that, and you have saved that client a lot of additional stress and money. So they may certainly be interested in adjusting their pricing accordingly.

Ask for Incentives or Concessions

If you’re financing, ask for a seller to pay down the points on your mortgage. This is often a good strategy versus asking for a price reduction.

Sometimes this is something I say to my seller clients, too. “Look, you are trying to achieve X price. You can either lower your price, or we can offer a buyer incentive.” That could mean paying points. Or it could mean paying their taxes for the first year, or making an HOA concession.

After Signing: Staying Agile Until Closing

Even though you are in contract, that does not mean that you are in fact going to close on the property. A great example of this is Olivia Dunne. She apparently was in contract to buy the apartment where Babe Ruth once lived and was turned down by the board.

There was a point in the video where she says something to the effect of, “Well, a week before I was supposed to get the keys, I got turned down,” and I'm thinking to myself, “Well, I'm a little worried that you maybe did not fully understand the framework of a co-op purchase.”

I always tell my clients, until you get approved by the Board, there is no “this is the day I'm supposed to get my keys.” It doesn't work that way. You have to have co-op board approval.

Check Everything

Even when there’s no co-op board or condo association involved, you still need to stay on your toes. Stay in communication with your agent and your mortgage lender. Check all of the outlets, all of the faucets, all of the drains.

When my clients were buying an apartment in Brooklyn, part of the building that they were looking at had outdoor spaces, and they ended up with a section of the roof that is exclusive to them. And so when we were doing the walk-through I was asking, “Okay, so how does drainage work here, and what does that look like?” Because I knew my clients, and I knew they would frequently use that space. I was worried that if something ever happened, they would be responsible. What was their responsibility for the part of the roof that they owned, versus the rest of the public roof?

Now that he’s the owner, he reminds me of that every time that we're out there for a big barbecue. Just the other weekend he said, “I always remember you made us ask about the roof drainage,” and I said, “Yeah, because it's very important.” He laughed, because he's now on the board. He says whenever he’s in board meetings now, he says, “Well, what would Nikki tell us to think about if she were here?”

Legal Support & When to Bring In an Attorney

As I said before, I am not a lawyer. Depending on where you live and the laws of your city or state, you may need a real estate attorney to help you draw up a purchase agreement.

I always say to people, make sure that you make time to talk with your professional. You’re working with a lawyer, they’re the professionals who can talk you through everything. Same as when you’re working with a real estate agent. Schedule a time, have a conversation, and walk through it, line by line, and ask your questions.

If someone's not willing or they're really irritated by your questions, again, that means you’re working with the wrong people. If there’s no clarity from your conversations, keep asking. I worry when people say they’ve been trying to get answers from this person, and they either don’t get the answers or don’t understand the answers. You have the right to understand what’s going on.

The Purchase Contract Is Your Foundation

A good purchase agreement sets the foundation for a successful closing. You’ll know exactly what’s expected of you, and what you can expect from the seller. Combine that with a knowledgeable real estate professional — whether that’s an agent like me, or a real estate attorney, or both — and you will have the insights and information you need to buy with confidence. Remember, we’re here to help you. It’s literally what we do.

I would hope that one of the things that will continue to happen, especially because now buyers have to sign agreements with their brokers, is that buyers are being more specific and methodical about who they're working with and why they are working with them. I hope that they have trust in the person they're working with because all of us have different strengths in the ways that we communicate. You want to find the team that’s the right fit, so that the whole thing can go smoothly.