Interest rate is the percentage of your loan balance that your lender charges annually. APR represents the overall cost of borrowing, also taking into account other fees and expenses associated with your mortgage. Both are important metrics to consider when shopping for a loan.

While searching for a mortgage, it's common sense that you'll want to find a loan with a low interest rate. However, there's another number you should also be concerned with: the annual percentage rate (APR).

In short, the interest rate is the cost that you pay to a lender annually to borrow funds. The APR, on the other hand, also includes a majority of the other fees and expenses related to the loan. In most cases, APR provides a more comprehensive view when comparing different mortgage options and lenders.

What Is Interest?

Interest is the ongoing fee – represented as a percentage of your loan balance – that you pay to a lender in exchange for them financing your mortgage. Interest is charged for the duration of your loan and serves as the lender’s primary source of profit.

How Is Interest Calculated?

In most cases, interest costs for mortgages are calculated every month. This is done by multiplying your loan balance by your monthly interest rate, which is your annual rate divided by 12. For example, if you have a $280,000 balance on a mortgage with an interest rate of 7%, your interest costs for the month would be approximately $1,633 (280,000 multiplied by .07 divided by 12).

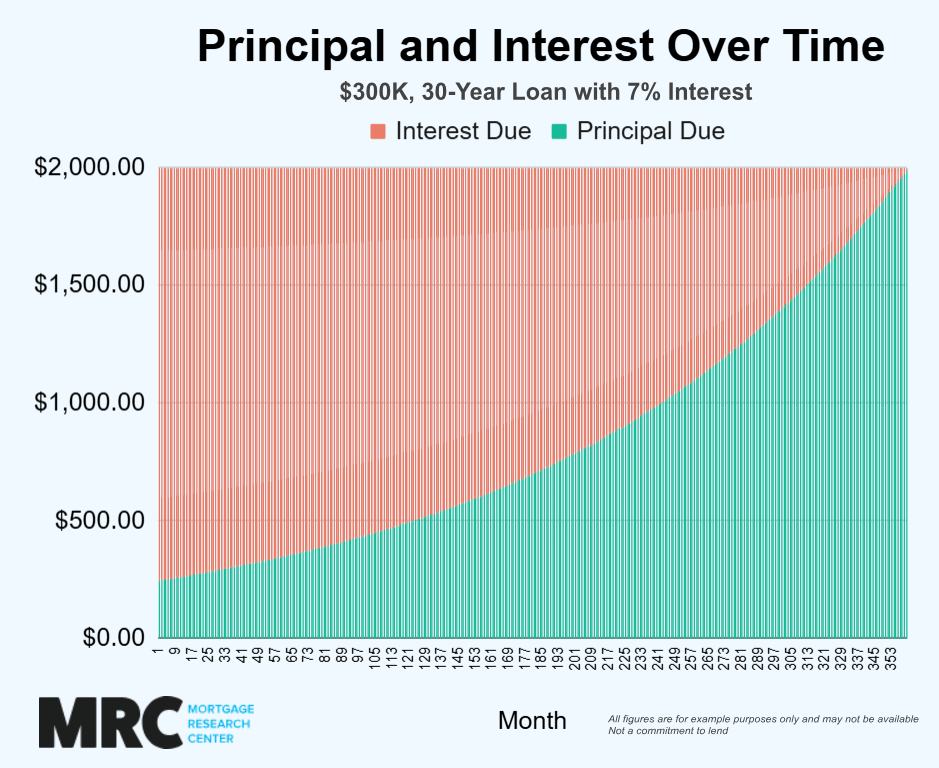

However, most mortgages are amortized, meaning that their overall interest costs are spread across the life of the loan, allowing for consistent monthly payments. This results in a significant portion of your payments being applied to interest costs in the early years of the loan. As the loan matures, the amount applied to the principal balance steadily increases.

Example: Say you're taking out a $300,000 30-year mortgage at an interest rate of 7%. In this scenario, you would have monthly principal and interest payments of about $2,000, or about $24,000 over the course of a year.

During the first year of repayment, $20,903 of this would be applied to interest, while only $3,047 would go towards your principal balance. However, during the final year of repayment, $23,067 would be applied to your principal and just $884 allocated to interest costs.

What Is APR?

A mortgage's APR is the overall annual cost of borrowing funds, including the interest rate and other expenses such as lender fees and mortgage insurance. A loan's APR will almost always be higher than its interest rate and tends to provide a more accurate comparison when evaluating different lenders or loan products.

How Is APR Calculated?

APR is calculated based on the interest paid on a loan, plus most of the other associated costs, which can include:

Origination fees

Administrative fees

Document prep fees

Prepaid interest

Lender discount points

Mortgage insurance

These additional expenses are combined with the interest and spread out over the life of the loan to show the true costs of borrowing funds.

Example: Let's say that you're taking out a $350,000 30-year mortgage at an interest rate of 6.5%. In this sample scenario, you'll incur $10,000 in applicable closing costs and spend $19,000 on mortgage insurance. These expenses equate to a total APR of around 7.2% which more accurately represents your total costs than simply looking at the 6.5% base rate.

The Differences Between Interest Rate and APR

The primary difference between interest rate and APR is that the interest rate shows the percentage that you're paying to the lender annually for the right to borrow funds. The APR also adds in the other costs associated with your mortgage.

However, keep in mind that both rates can be helpful in different scenarios, and neither by itself will give you a complete understanding when comparing different loan options.

For example, loans with a lower interest rate typically result in lower monthly payments when comparing similar mortgage products. If your primary concern is the amount you'll pay each month, comparing loans by interest rate can be a practical strategy.

On the other hand, if you’re concerned with the other costs and fees associated with the mortgage, choosing a loan with a lower APR will typically be the better value, assuming the underlying interest rates are comparable.

| Interest Rate | APR |

|---|---|

| Illustrates the ongoing amount paid to borrow funds | Shows the total cost of your loan on an annual basis |

| Does not include closing costs, fees, or mortgage insurance | Includes nearly all costs associated with your mortgage |

| Better for comparing monthly payments | Better for comparing overall costs |

| Typically lower than the APR | Typically higher than the interest rate |

How Do These Affect Different Loans?

Some types of loans will have a more pronounced difference between the interest rate and APR than others. Let's examine some real-world examples of how these two metrics may vary for some common mortgage programs.

FHA Loans

Although FHA interest rates tend to be low, the costs associated with these mortgages – including the mortgage insurance premium – contribute to an APR that's often higher than that of other types of loans. At time of writing, the average 30-year fixed FHA purchase loan comes with an interest rate of 5.59% and an APR of 6.8%, a spread of 1.21% according to Rate Update.

Note: all stated rates are for example purposes only and sourced from Rate Update. See current average rates on our latest daily rate article.

VA Loans

VA loans, on the other hand, do not require ongoing mortgage insurance. They do, however, have an initial VA funding fee ranging from 1.25% to 3.3% for most buyers. Today's current VA purchase loan average interest rate on a 30-year fixed-rate mortgage is 5.66% with an APR of 5.8%, representing a 0.14% difference.

USDA Loans

USDA loans have upfront and ongoing guarantee fees, which serve to ensure the ongoing viability of the USDA mortgage program. Rates for USDA purchase loans are even lower than with the FHA or VA right now, with an average interest rate on a 30-year mortgage of just 5.55% and an APR of 5.69%, a difference of 0.14%

Conventional Loans

Conventional mortgages have no upfront mortgage insurance premiums and only require ongoing mortgage insurance for borrowers financing less than 80% of their property’s value.

As rates are slightly higher on conventional purchase loans since they aren't backed by the federal government, today's average 30-year conventional mortgage has an interest rate of 6.32% and an APR of 6.35% - a spread of just 0.03%

How to Lower Your Interest Rate

Interest rate typically provides a good representation of a loan's monthly payments. Taking out a loan with a lower interest rate generally results in lower monthly costs compared to a comparable mortgage at a higher rate.

Let's explore some of the most effective strategies for securing a favorable interest rate.

Improve Your Financial Profile

Your overall financial profile, which includes your credit score, debt-to-income ratio, and other risk-defining factors, has a major impact on the interest rate you qualify for. According to a sample study, the Wall Street Journal reports that borrowers with a credit score of 620 would pay an average of 0.78% more in interest than those with a score of 780 or higher.

Shop Around With Multiple Lenders

Interest rates can vary significantly based on the lender you choose to work with. To help ensure you're receiving the best loan offer possible, get pre-qualified with a minimum of three different mortgage providers. Plus, having multiple loan estimates allows you to use the most favorable to negotiate the rate with the other companies and force them to compete for your business.

Purchase Lender Discount Points

Lender discount points are upfront fees paid to your mortgage company in exchange for a lower interest rate. In most cases, one discount point costs 1% of your loan amount and results in an interest rate reduction of approximately 0.25%.

Keep in mind, however, that while lender discount points will lower your rate, the expense will still be factored into your APR.

Choose a Shorter Loan Term

Loans with a shorter repayment term typically come with lower interest rates, as they involve less overall risk for the lender. As of the time of writing, the average 30-year conventional fixed-rate mortgage has an interest rate of 6.32%. That average rate decreases to just 5.45% when financing your purchase with a 15-year loan.

How to Lower Your APR

Generally speaking, the most effective tactics for lowering your APR will be the same as those used to lower your interest rate. That's because your quoted interest rate has the most significant impact on your overall APR. By reducing the interest rate you qualify for, you'll typically lower your APR as well.

When it comes to your APR in particular, though, the two best strategies will be to:

Shop Around With Different Lenders – Lender fees and closing costs will impact your APR, and different lenders may offer loans with different APRs, even if the nominal interest rate is the same. When shopping around for a loan, you can also use competing quotes to negotiate lower lender fees, resulting in a lower APR.

Consider Different Types of Loans – As we covered earlier, different types of loans will have different fees, which can impact the spread between the quoted interest rate and the total APR. VA and USDA loans typically have some of the lowest APRs, while FHA loans tend to have the highest average APRs. For most borrowers, however, conventional mortgages remain a popular option.

Questions to Ask a Lender

Asking the right questions can provide you with a much better idea of the overall picture when shopping around and comparing loans. Here are some of the most important things that you should ask each lender you speak with.

Do you offer any loan programs with better rates specifically for first-time homeowners?

Does the rate you offer require the purchase of discount points, and if so, how many?

Are you willing to match lender fee quotes from another mortgage provider?

Can I lock in my rate, and if so, what will the cost be, and how long will the rate lock be in effect?

Are there any straightforward steps I can take to improve my financial profile and qualify for a lower rate?

Key Points to Remember

Your interest rate is the percentage of your loan balance that you’ll pay to your lender annually in exchange for borrowing funds. Your APR, which takes into account your interest rate, also includes other fees and expenses associated with the loan.

Generally speaking, the APR provides a better picture of the overall cost of a mortgage, while the interest rate is more indicative of a loan's monthly payments. Both, howev