During the mortgage underwriting process, your lender will examine your credit, income, assets, and the property. Preparation, transparency, and strong communication with your loan officer help keep approval on track.

Adam Godby (NMLS #2286643) is a Loan Officer and Team Lead at First Residential Independent Mortgage (NMLS #1907), a Springfield, Missouri-based national lender. Equal Housing Opportunity. First Residential is a registered DBA of Mortgage Research Center, LLC, an affiliate of Three Creeks Media.

Will your loan get approved? Mortgage underwriters have the final say. If obtaining a loan worked like a legal trial, the underwriter would serve as the jury.

To decide whether to approve your loan, underwriters have to scrutinize all the evidence.

The evidence, of course, includes your income, monthly debt, credit score, savings account balances, work history, rental history, home value, down payment size, and so on. All the data collected during the loan process gets laid out in front of the underwriter.

The Role of Underwriting — Beyond Pre-Approval

This trial comparison goes only so far. Unlike in a court trial, the mortgage borrower who goes through underwriting can know, before the trial begins, what verdict to expect.

A surprise verdict — that is, a surprise loan denial — can happen, especially if something changes in the loan file at the last minute. But a good loan officer won’t let a borrower stand before the jury unless they expect the jury to say yes to the loan.

You can’t always say this about mortgage pre-qualification or mortgage pre-approval. Pre-approval or pre-qualification often shows what should be true about a borrower’s finances. To fully approve a loan, underwriters go beyond what should be true. They take the extra steps to determine what is really true about the borrower’s financial profile and ability to repay the loan.

Or, to continue our legal trial analogy: Pre-approval can rely on circumstantial evidence. For example, a screenshot of a bank account balance may be good enough to get pre-approved. For underwriting, you will need to submit full bank statements. That way, underwriters can see the full context of the account balance and find out where the money came from.

Documents, Deadlines, and Deal-Killers — What Gets Scrutinized Most?

A jury will look for means, motive, and opportunity. Underwriters look for a different trio of factors: creditworthiness, income, and assets:

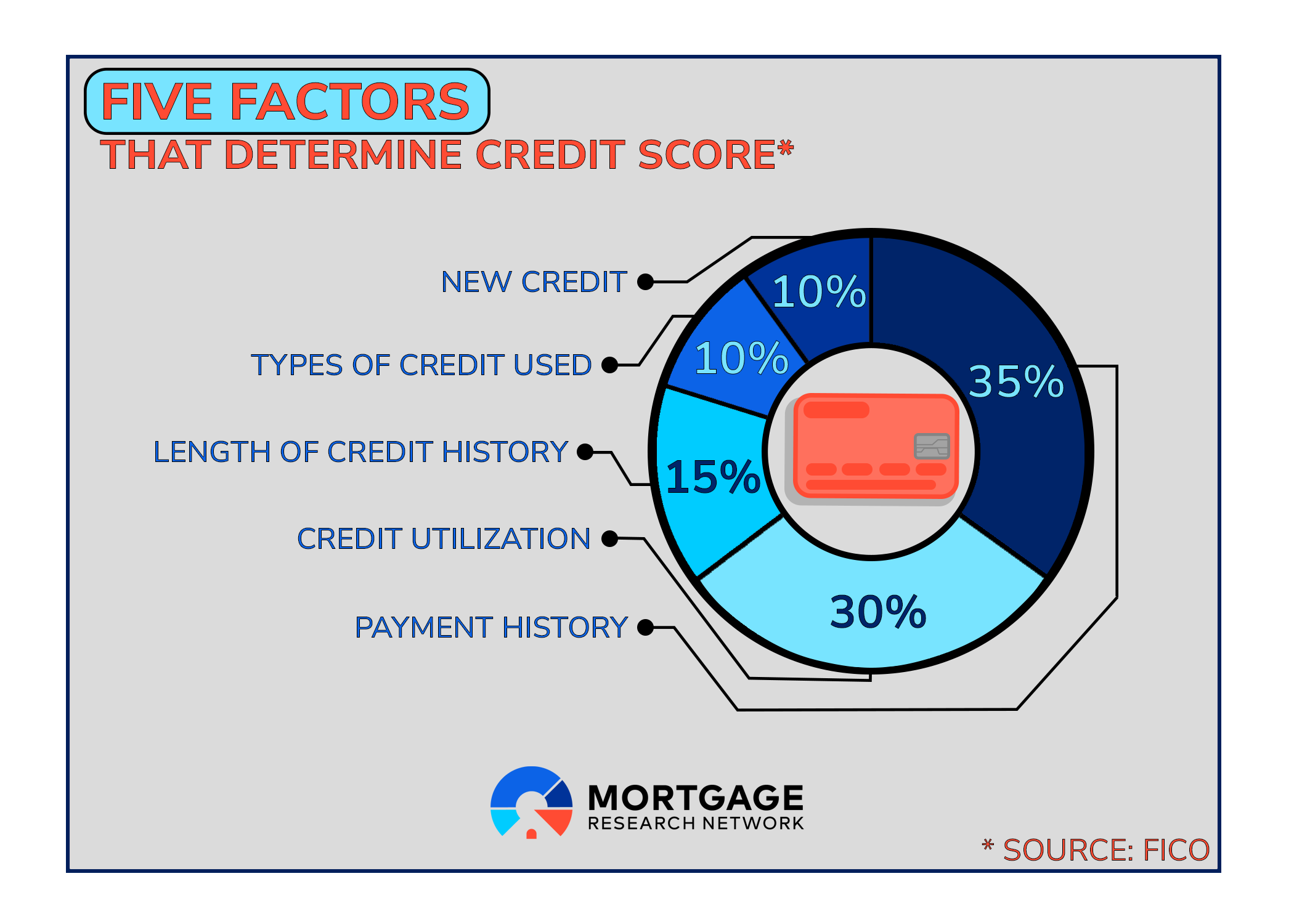

Creditworthiness

For mortgage approval, creditworthiness goes deeper than your credit score. Underwriters will look through your credit reports to scrutinize the data that builds your score.

Some people have an excellent credit score, but it’s based on only one credit card account. That’s thin evidence compared to a borrower who’s built excellent credit by successfully managing a variety of credit accounts for a decade.

Rent history can factor into creditworthiness, too, even though it doesn’t show up on a credit report.

Income

Underwriters dig deeper than W2 or pay stub numbers. They want to know how long you’ve been in your profession. They want to confirm you still have the job and that the earnings you’ve documented over the past two years are expected to continue.

For self-employed income, underwriters need to see income tax returns and profit-and-loss statements.

Not all income that’s been earned can be counted for the mortgage. See my article about the real story on debt and income here.

Assets

Underwriters need to know where your down payment money is coming from. If it’s from a gift, they need to make sure your generous relatives or friends won’t ask for the money back, adding to your monthly debt load. A letter from the donor can accomplish this goal.

Underwriters also need a sense of your overall financial health. For example, some borrowers have enough money in savings to cover the mortgage payment for a few months. They can weather a financial storm better than borrowers whose home purchase exhausted their funds.

If you have a healthy retirement account or own another piece of property, these assets can also strengthen a loan file.

Rule 1: Talk to Your Loan Officer Before Making Changes

Weaknesses in any of the three factors above can threaten loan approval, but your loan officer should know and address any problems before sending your file to underwriting.

When borrowers make changes without telling their loan officer first, bad things can happen. That’s kind of like not telling your defense attorney that you plan to take a plea deal.

Borrowers should speak with their loan officer before spending money from savings. This includes purchasing furniture or paying a deposit toward moving expenses. Also, talk to your loan officer before taking out a new line of credit, changing jobs, or even paying off a credit card. Doing any of these things can disrupt your case and jeopardize loan approval.

A Fourth Potential Deal Killer: The Home Itself

Creditworthiness, income, and assets tell underwriters about the borrower’s ability to repay the loan. But the home you’re buying has to qualify, too.

For example, the home has to be worth enough money to support the loan. The home appraisal, ordered during the underwriting process, helps determine whether this is true. For instance, a lender can’t approve a $350,000 loan to buy a home that appraised only at $325,000, even if you’re under contract to pay more.

If the home doesn’t appraise high enough, you may need to renegotiate a new price with the seller.

The home also has to go through a title search to make sure the owner has the right to sell it. Recently, I had a client whose loan got declined because the home, it turned out, was tied up in probate. The seller didn’t have the right to sell it.

Fortunately, this example worked out OK for the buyer. The owner allowed them to rent the home for a few months while the probate issue got sorted out. But it doesn’t always end this well.

Conditions and Conditional Approvals

After the loan file goes to underwriting, it’s common for borrowers to receive conditional approval. Conditionally approved means the loan can move forward if certain conditions are met.

Those conditions can include:

Successful appraisal and title search, as described above

Completing the FHA home appraisal process, which includes an inspection to make sure the home is safe and ready to be lived in

The sale of another home

Receiving a down payment gift and/or gift letter from the donor

Final verification of income or assets

Getting homeowners insurance

Submitting other documents

All conditions must be cleared before the loan can move forward.

Getting homeowners insurance or selling another home should be simple. You were going to do that anyway. But not every condition is easy to clear. For example, underwriters may ask for 12 months of rent history to strengthen a thin credit file. But what if the borrower paid rent in cash each month and the landlord isn’t responding to their request for records? Or what if the landlord has died and didn’t leave behind clear documentation?

This kind of stuff happens. It has happened to people I’ve worked with. In these scenarios, we may need a Letter of Explanation to tell underwriters why a condition can’t be met. No matter what, it’s essential to communicate throughout the process.

Speed, Communication, and Getting to the Finish Line

For whatever reason, some borrowers treat their loan officer, and their mortgage lender in general, like an adversary. They act like the lender is a strict teacher, and they’re the kid in the back of the room who tends to misbehave.

That’s not how this relationship between lender and borrower works. Loan officers and underwriters want to approve mortgages that help people become homeowners. But they also have to follow federal law and make responsible loans. Lenders won’t ask for anything they don’t actually need.

I’m the type of loan officer who’s proactive. I go the extra mile, and sometimes even farther, for my borrowers. But I can’t want loan approval more than you do. To keep loan approval on track, homebuyers must respond promptly to requests for information. If underwriters ask for additional documents, start gathering them right away. There’s usually no reason to wait a day or two.

Also, always ask questions. If you feel like the loan officer is forgetting something important, don’t let it go. If you're unsure about something, ask. It’s better to find out about problems before underwriting begins.

I’m the type of loan officer who’s proactive. I go the extra mile, and sometimes even farther, for my borrowers. But I can’t want loan approval more than you do.

The Future of Underwriting — AI, Automation, and Risk Tolerance

Automation isn’t new in mortgage underwriting. Fannie Mae, Freddie Mac, and government-insured loan programs have been using automated underwriting systems since the late 1990s.

But like the rest of the economy, artificial intelligence is elevating automation in mortgage underwriting to a new level. Many mortgage lenders are now launching AI-based initial underwrites. Some lenders have already been using AI for pre-approvals and the initial phases of underwriting for a while.

This means algorithms are helping gather documents and analyze data. With some lenders, AI is answering simple questions from borrowers.

Having AI handle routine tasks could free up human loan officers and underwriters to focus on more complicated inquiries.

For Successful Underwriting, Communication Always Matters

Whether underwriting happens with AI, a desktop underwriting program, or manual underwriting by a human, one thing always matters: good communication between borrower and lender.

Your loan officer should be your advocate both before and during the underwriting process. Your job as a borrower is to answer all your loan officer’s questions and provide all the evidence that supports your case.

That’s the best way to get the right verdict — loan approval and homeownership — as quickly as possible.