FHA loans make it possible to use rental income from a multifamily home to help you qualify — even if you're a first-time landlord. With the right property and a lender who knows the guidelines, rental income can be a powerful tool to boost your buying power.

Buying a duplex, triplex, or fourplex, or a single-family home with an accessory dwelling unit (ADU), is one of the most strategic moves you can make in real estate.

You become a homeowner and a landlord with one transaction.

But not every buyer knows about an FHA rule that could make it even easier to purchase a multifamily property than a single-family home.

FHA rental income guidelines in 2026 enable borrowers to use anticipated future rents on the property to boost their income and help qualify for an FHA loan.

In This Article:

How To Qualify More Easily Using Future Rents

First things first: the property must be a 2-, 3-, or 4-unit multifamily property. FHA does not allow you to use rental income on a single-family home unless there's an accessory dwelling unit (ADU) on the property.

You must also live in one of the units as your primary residence.

UPDATE: Recent FHA guideline updates now allow you to use income from a boarder/roommate to qualify for a single-family home loan in some scenarios. We'll go over the details of this program change a little further down.

The lender will use a formula to calculate the qualifying and add it to your employment income. You can then use a combination of employment plus rent to qualify.

Here’s how it works.

| FHA 1-Unit | FHA 2-Unit | |

|---|---|---|

| Home Price | $250,000 | $300,000 |

| Monthly Payment* | $2,200 | $2,500 |

| Other Debt Payments | $500 | $500 |

| Employment Income | $5,200 | $5,200 |

| Net Rental Income | N/A | $1,200 |

| Qualifying Income | $4,800 | $6,400 |

| DTI | 52% | 47% |

| Result | May not qualify | May qualify |

*Assumes FHA loan at an interest rate of 6%, 3.5% down payment, FHA upfront and annual MIP, property taxes, homeowners insurance, and HOA dues.

In other words, because of FHA rental income guidelines, you may be approved to buy a 2-4 unit property more easily than a single-family home.

How Do You Prove Future Income?

Proving future income on an FHA multifamily home isn’t as hard as it sounds. Here’s what you need.

If Units Are Currently Rented: Supply the lender with current lease agreements for the units you won’t be occupying. Ask your real estate agent to get this from the seller’s agent.

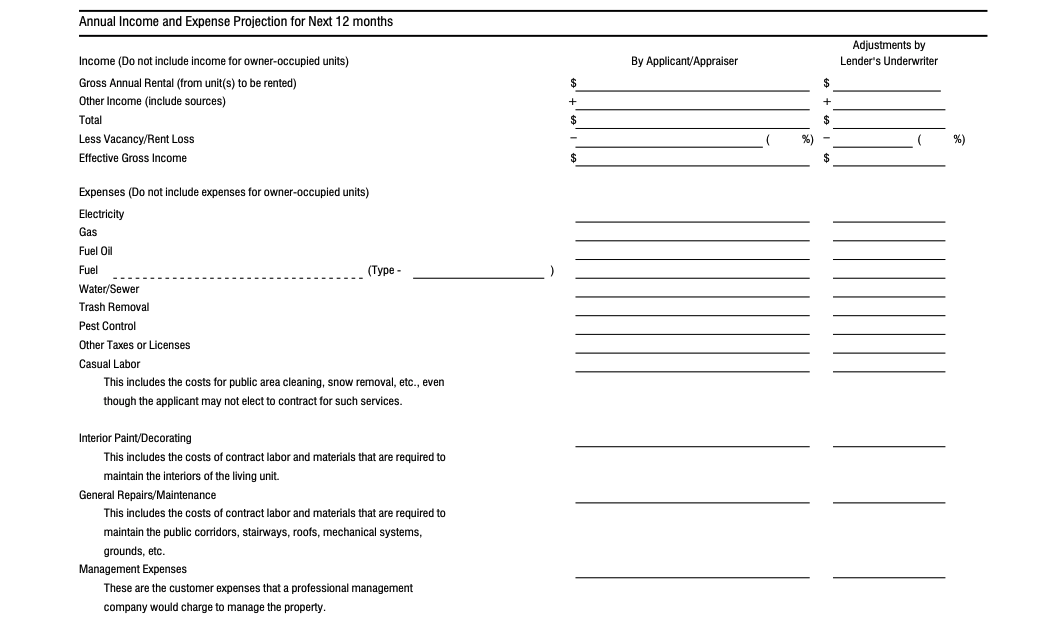

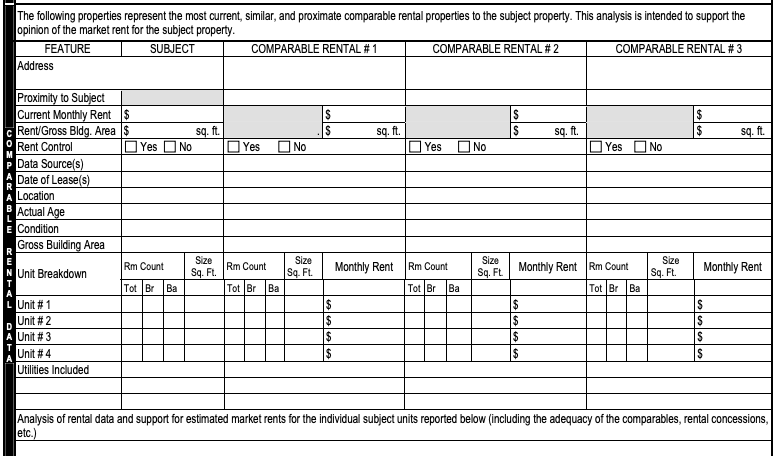

If Units Are Not Rented: The FHA appraiser will complete several reports, including an income/expense analysis (Fannie Mae 216/Freddie Mac 998) and a market rent analysis (Fannie Mae 1025/Freddie Mac 72).

From there, the lender uses the lesser of:

Projected income based on an income/expense estimate

75% of fair market rents

75% of actual rents

For example:

| Report | Rent amount | Net rent |

|---|---|---|

| Income/Expense Analysis | $800/mo | $800/mo (no deduction required) |

| Market Rent Analysis | $1,100/mo | $825 (75%) |

| Current Lease | $900/mo | $675 (75%) |

| Rental Income Used | $675 |

In the above example, the income/expense method is not reduced because it already factors in a vacancy rate.

The other two methods require a 25% reduction because the FHA assumes the property will be vacant 25% of the time, even though that’s very conservative. True vacancy rates in good markets tend to be more like 5-10%.

Maximizing Future Qualifying Rental Income

Take a look at the example above. You’ll note that you have to use 75% of the current rent to qualify, even if the unit might rent for more.

This is likely because the Department of Housing and Urban Development (HUD), the overseer of FHA, assumes you cannot or will not charge higher rent or evict current tenants to raise rent.

So one strategy is to find a multifamily property without existing tenants. These properties can be hard to find, though, so you may need to purchase one with existing leases in place.

Properties With Below-Market Rents

Some properties have long-term tenants paying well below market rent. This is a sign of mismanagement; the landlord didn’t keep up with local rental trends.

The tenants will never leave. One strategy (though it might sound heartless) is to declare that you will live in the unit with the lowest current rent. The tenant will have to move on. Then you can qualify (and make more money) from the higher-priced units.

This should be viewed as a business decision; you shouldn’t feel bad for displacing a low-paying tenant.

More About the Appraiser’s Reports

The appraisal rent analysis can seem daunting.

Operating Income Statement (Fannie Mae Form 216/Freddie Mac Form 998): If you’ve ever seen a “P&L,” or profit and loss statement from a business, this form is somewhat similar. It attempts to calculate income and expenses from each unit to arrive at a net cash flow. Here’s a small snapshot of this otherwise lengthy form.

Small Residential Income Property Appraisal Report (Fannie Mae Form 1025/Freddie Mac Form 72): This is similar to the single-family appraisal report, except it is specific to 2-4 unit properties. It reviews comparable rentals and sales in the area. Its purpose is to determine the market rent for each unit, as well as the value of the entire property.

Using Boarder/Roommate Income to Qualify for a Single-Family Home

Recent changes to FHA rental income guidelines mean that you can now use rental income from a roommate or boarder to help you qualify for a single-family home, even if it does not have an ADU.

There are some requirements, however, that will need to be met for this type of income to qualify:

- The boarder must have already been living with you for a minimum of 12 months

- You must be able to provide proof of receiving rental payments for at least 9 of the past 12 months

- You must submit evidence that the boarder's current address is the same as yours

- There must be a written agreement outlining the rental terms and stating the boarder will continue to live with you in your new home

It's also important to note that rental income from a roommate or boarder can make up no more than 30% of your total qualifying income amount.

Rental Income From Another Property

FHA rental income guidelines can be split into two different categories:

Rental income from the property you’re buying (the “subject property”)

Rental income from a different property you own and collect rent from

FHA rental income guidelines can get very muddy when it

comes to rental income from another property. To keep things clear, this

article only covers the guidelines for rental income on the subject

property you plan to buy.

A “Gotcha”: The FHA Self-Sufficiency Test

More is not always better when buying a multifamily home with FHA financing.

Recently, HUD started requiring the FHA self-sufficiency test for 3- and 4-unit properties. This rule doesn’t apply to duplexes.

The requirement states that the property must generate sufficient rental income to cover its full payment. Since home prices and interest rates are much higher than they were just a few years ago, it’s becoming increasingly difficult to get a property to pass the test.

You may want to keep things simple by looking for a duplex rather than a triplex or quadplex.

My Lender Says I Can’t Use Future Rental Income To Qualify

Your lender may say you can’t use future rental income to qualify for an FHA loan. If this happens, shop around for a different lender.

This is an example of a “lender overlay,” or when a lender imposes additional rules on top of existing FHA guidelines. The FHA permits borrowers to use future rental income, and it shouldn't be too difficult to find a lender that allows you to do so.

Additional Considerations

Remember that owning a home is a significant financial responsibility. Becoming a landlord at the same time carries even more obligations.

Sure, you have to fix things when they break, which requires some financial reserves.

But a landlord has to deal with tenants and potential headaches if tenants don’t hold up their end of the deal.

What if your tenant can’t pay rent due to a job loss? Do you let it slide? At what point do you re-establish rules? These situations will come up, guaranteed. And because your tenant shares a wall with you, issues can be even thornier.

The upside is that you'll be building lasting wealth with your real estate investment. As long as you go into it with realistic expectations, protect your interests with lease agreements, and treat it like a business, becoming a landlord can pay off.

FHA Rental Income Guidelines FAQs

Here are answers to some of the most frequently asked questions about FHA rental income guidelines.

Do I Need Landlord Experience to Count Future Rental Income for FHA?

No. FHA guidelines state that you can count future rents toward income even without landlord experience. If your lender tells you otherwise, they are imposing additional rules on top of FHA guidelines, called overlays, and you should shop around for another mortgage company that can get you approved.

Can I Qualify for an FHA Multifamily Loan With No Employment Income?

In nearly all scenarios, no. It's highly unlikely that the rental income alone will be enough to qualify you for the property. Employment income will be the majority of qualification income; rental income is only a supplement. You should plan to need a healthy employment income to get approved for an FHA multifamily loan.

Is Buying a Multifamily Home With FHA Financing "House Hacking"?

Yes. Buying a multifamily home, living in one unit, and renting out the others is known as “house hacking.” The strategy is to live in the property for 12 months (the minimum requirement), then convert the entire property into a rental. Using an FHA loan gets you into a rental property with a small down payment.

How to Apply

Applying for an FHA multifamily loan is just like applying for any other home purchase.

When you apply for an FHA loan, your lender will verify your income, employment, assets, liabilities, and credit score and history. The lender will determine a maximum loan amount and issue you a pre-approval letter you can use to shop for properties.

Once you find a home and get your offer accepted, the lender will work with you to close the home purchase.