Thirty-year mortgages offer lower payments and greater borrowing power. While 15-year loans save on long-term interest and help you build equity faster, many borrowers refinance, move, or pay extra toward their principal, reducing the 30-year loan’s true cost.

Adam Godby (NMLS #2286643) is a Loan Officer and Team Lead at First Residential Independent Mortgage (NMLS #1907), a Springfield, Missouri-based national lender. Equal Housing Opportunity. First Residential is a registered DBA of Mortgage Research Center, LLC, an affiliate of Three Creeks Media.

Fifteen-year mortgage terms look pretty good on paper. They’re set up to charge less interest over the long run than 30-year loans. They build home equity faster. They offer lower average mortgage rates.

With all this going for them, you might think loan shoppers would want 15-year loans instead of 30-year loans.

But that’s not what happens. I can think of one client, among the thousands I’ve helped buy a home, who came to me insisting on a 15-year loan.

Why are 30-year mortgages so popular, and is a 30-year term right for you? Let’s take a close look at these two types of loans to see how they really work.

Monthly Payment vs. Total Interest: The Core Trade-Off

Yes, the 15-year term charges less interest eventually, but the 30-year term costs less right now: Monthly payments on a 30-year fixed will be lower than the payments on a 15-year loan.

Those month-to-month savings matter more to most home shoppers, especially first-time buyers, than long-term costs.

What is the price difference per month? For a $300,000 loan at 6 percent interest, here’s how the payments (not counting property taxes, fees, and insurance) break down:

15-year term: $2,532 a month

30-year term: $1,799 a month

That’s a monthly difference of $733. By getting a 30-year loan, this homebuyer saves $733 each month and can put that money into savings or toward other expenses.

Borrowing Power: 15- vs 30-Year Terms

Paying less each month does more than just ease the budget. Lower payments increase mortgage eligibility. Getting approved for a mortgage depends so much on the borrower’s income and monthly debt, including the new mortgage payment.

So lower payments allow bigger mortgages, and bigger mortgages, of course, allow people to buy more expensive homes.

For example, if your budget, based on your documented income and monthly debt, allowed for $1,800 a month toward principal and interest on a mortgage loan, you could either:

Borrow $300,000 over a 30-year term at 6 percent and pay $1,800 a month in principal and interest

Or, borrow $214,000 over a 15-year term, also at 6 percent, and pay the same $1,800 a month in principal and interest

That’s a difference of $86,000 in borrowing power just by stretching the debt across an extra 15 years. Borrowers I work with tend to prefer getting a nicer house for the same monthly payment.

In some housing markets, this can make the difference between buying a turnkey home and buying a home that needs a lot of work. In any market, investing in a more valuable asset can bring more long-term advantages.

But Borrowers Should Still Know Long-Term Interest Costs

Buyers who want the lower payments and increased borrowing power of a 30-year loan should also understand the tradeoff: more interest in the long run.

Let’s go back to our example, the $300,000 loan at 6 percent interest. This is the borrower from above who saved $733 a month by choosing the 30-year loan instead of a 15-year term.

If this borrower stayed on schedule with the loan, here’s what they’d pay in interest before paying off the home:

15-year interest paid: $155,683

30-year interest paid: $347,515

The 30-year loan costs $191,832 more in interest than the 15-year loan. That’s the core tradeoff of getting a longer term.

Quoted Costs Don’t Have to Be Actual Costs

Debt-sensitive homebuyers may get frazzled by the cost of 30-year borrowing. After all, in our example above, the interest due on a 30-year loan costs more than repaying the loan’s principal. From that point of view, you’re paying for the same home twice.

Or maybe not.

There’s a reason these kinds of articles include lots of “ifs,” “whens,” and other kinds of disclaimers. It’s because these quoted interest costs — like the costs in your Loan Estimate and Closing Disclosure — show costs for one kind of borrower: the kind who repays the loan exactly as scheduled. On a 30-year loan, that means making 360 consecutive on-time payments until the balance reaches $0.

In reality, few borrowers do this. Most people refinance the loan or sell the house and move, usually within eight to 10 years. The few who do stay in the home for 30 years may pay off the mortgage earlier, cutting into these quoted interest costs.

The Power of Paying Off the Loan Early

So, back to our example, a $300,000 loan at 6 percent over 30 years. If you remember, paying this loan off as scheduled adds $347,515 in interest to the $300,000 principal.

Here’s how much interest you’d pay if you sold the home or refinanced the loan early:

After 3 years: ~$53,000 in interest paid on the loan so far

After 5 years: ~$87,000 in interest paid on the loan so far

After 7 years: ~$120,005 in interest paid on the loan so far

Let’s say you decide, after three years, to sell the home and buy a larger house. Assuming you made on-time, scheduled payments for those three years, you paid about $53,000 in interest. That’s an average of about $1,472 a month.

Meanwhile, over those three years, the house has appreciated, increasing in value from $315,000 to $355,000. The loan balance is down to about $288,250. That means you could sell the home for $355,000, pay off the $288,250 loan balance, and still have almost $67,000 in profit.

The $53,000 interest paid was a good investment. Even after paying a Realtor commission and some other closing costs, you’d have enough left from the $67,000 you cleared to make a nice down payment on a more expensive property.

An important disclaimer: Not every home is guaranteed to appreciate on this schedule. Historically, homes have appreciated by about 3 to 4 percent a year on average, but results vary by location. Sometimes, housing markets cool off, and prices stay about the same for a few years.

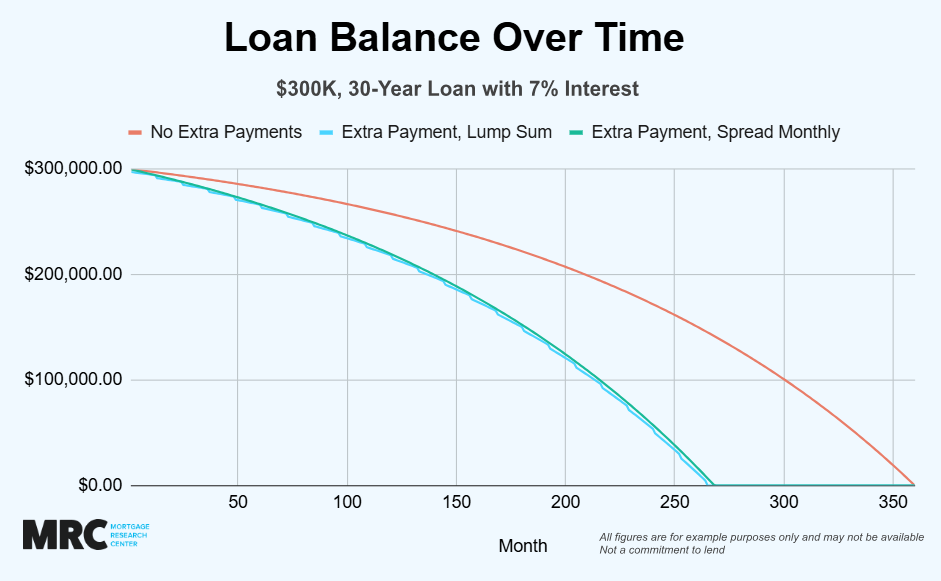

The Power of Paying Extra on the Loan

What if you plan to stay in the home for 30 years or longer? You can still dodge the 30-year loan’s full interest load by making extra payments on the loan’s principal.

To be clear, you’ll make the loan’s regular payments on schedule, but also pay extra on principal each month or each year.

For instance, could you pay:

$200 extra on principal each month? Doing this each month will shave $91,174 off the total interest on the loan. Plus, the home will be paid off six years and nine months early.

$400 extra on principal each month? This cuts total interest charges by $142,127 and pays off the loan almost 11 years early.

$733 extra a month? Does this number seem familiar? It was the difference between the payments on a 15-year and a 30-year loan in our examples above. Making an extra payment in this amount each month effectively turns the 30-year loan back into a 15-year loan. The loan is paid off in 15 years, and you’d save about $192,000 in interest.

Most 30-year borrowers couldn’t pay an extra $733 a month on a 30-year loan, at least not for a while. But any extra amount on principal, when paid consistently, can create big savings.

The Real Difference Between 15- and 30-Year Loans: The Minimum Payment

A loan term of any length lays out a plan. What you do with that plan creates your reality.

The most concrete number on your Loan Disclosure will be your monthly payment amount. This is the amount you’ll need to pay to keep the loan current. That’s the real difference between a 15- and a 30-year mortgage. The 30-year loan requires a lower monthly payment.

For many borrowers, a 30-year loan offers the best of both worlds: the security of lower payments in case they lose their job or face unexpected expenses, along with the flexibility to pay extra, making deep cuts in long-term interest costs.

My Favorite Method for Paying Extra on a 30-Year Loan

My favorite way to pay extra on a mortgage loan? Sneaking in an extra payment each year that you may not even know you’re making. This method works especially well if you get paid every two weeks instead of once a month.

Here’s what to do: Split your monthly mortgage payment into two installments. If you owe, for instance, $2,200 a month, you’d set aside $1,100 out of each paycheck.

Since you get paid every two weeks, and there are 52 weeks in the year, you’ll be making 26 half-payments a year. Those 26 half-payments turn into 13 full payments spread over 12 months. That’s where the extra payment comes from.

Applying this to our sample loan of $300,000 at 6 percent would cut six and a half years off the loan term and save almost $89,000 in interest.

Wealth Building Is the Goal. Payments Are the Path

A 15-year mortgage is set up to build wealth faster by paying down mortgage debt sooner and with less money going toward interest. But a 20-, 25-, or even 30-year loan can build wealth faster, too, when borrowers pay enough extra on principal.

Regardless of what term they use, I encourage my clients to take an honest look at their budget so they can make better-informed decisions about how they spend their money each month.

Someone who learns they’re spending, say, a few hundred dollars a month at Starbucks might decide to cut their coffee trips in half and put the savings toward the mortgage principal each month, which can have a huge impact on future wealth.

And if you’re still not sure whether to go with a 15-year, a 30-year, or a different term, you probably need more information. Ask your loan officer to help compare your choices. If your loan officer isn’t interested in this conversation, I’d recommend finding a loan officer like me who wants to help clients understand how to build more wealth.