It's possible to get a mortgage with a lower credit score, but it's much easier to get approved if you work on your credit.

The average U.S. credit score reached a record high of 715 last year, according to Experian, rising five points from 2020. But, even that’s not a score that likely would get you approved for a traditional mortgage.

Typically, mortgage lenders are looking for a credit score of at least 720, said Tony Smith, a real estate broker who serves on the Conventional Financing and Policy Committee of the National Association of Realtors.

However, for borrowers who don’t meet that minimum, there are several government mortgage programs that accept lower credit scores.

Government Mortgage Programs

They include home loans guaranteed by the United States Department of Agriculture (USDA), the Federal Housing Administration (FHA) and the Veterans Administration (VA), as well as some backed by federal mortgage institutions Fannie Mae and Freddie Mac.

“580 can get you through the door for an FHA loan,” John Ammar, a Caliber Home Loans senior loan consultant, said in an interview. “They have more favorable rates for lower credit scores.”

FHA loans for home purchases also help borrowers who aren’t flush with cash since they require down payments of only 3.5% instead of the 5% to 20% typically required by conventional loans.

If a borrower’s credit score is in the 500-579 range, an FHA loan on a home purchase is still possible, but the borrower must put 10% down at closing, according to the FHA underwriting manual. Borrowers in this range don’t have to make a down payment when refinancing existing loans, though, Ammar said.

Requirements for loans backed by Fannie Mae and Freddie Mac are more demanding. “Even with a 620 or 680 credit score, there’s a chance you won’t be approved by Fannie and Freddie’s underwriting standards,” Ammar said. “They have some of the strictest underwriting standards in the industry.”

Besides meeting minimum score requirements, a borrower must meet Fannie and Freddie’s other conditions, including a debt-to-income ratio below 45% and other credit variables, Ammar said.

» Tip: Looking to buy soon? Set yourself up for having your offer accepted on a home by getting preapproved for a mortgage prior to your home search.

Credit Repair Options

What’s the best way to build a better score before applying for a mortgage? It depends if the borrower is establishing credit for the first time or is trying to fix some credit mistakes.

Establishing credit isn’t difficult. Retail store credit cards can be a good place to start, said Ammar. Consumers can use the card for a small purchases and pay it off right away, to show they are creditworthy.

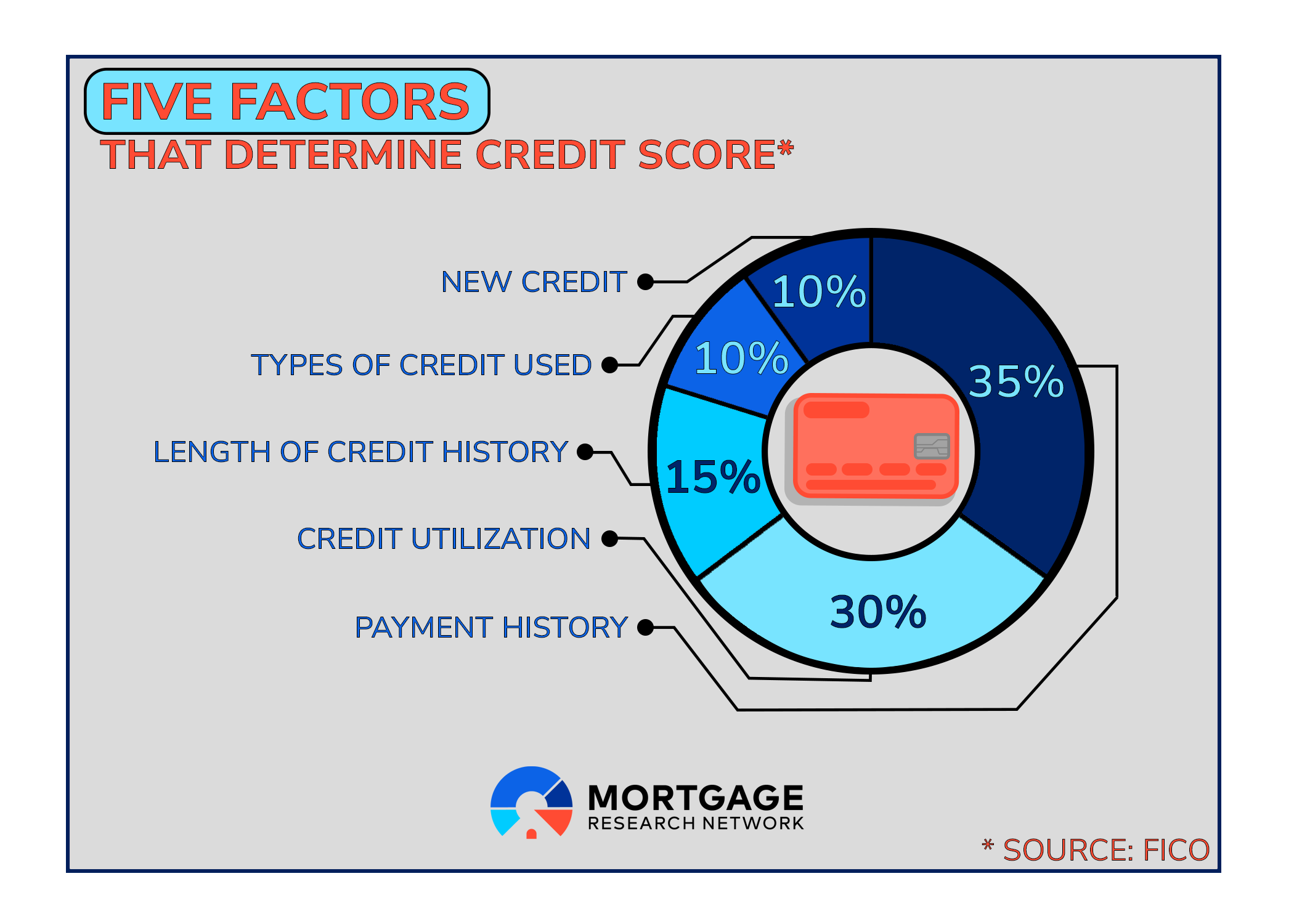

FICO, a predictive scoring model created by Fair, Isaac and Co., calculates credit scores based on the following components:

- Payment history (35%)

- Amounts owed relative to limits (30%)

- Length of credit history (15%)

- Types of credit used (10%)

- New credit (10%)

But these percentages are rough, and a lender might use another scoring model.

What about poor credit?

“Bad credit is fixable,” Ammar said. “Get a copy of your credit report. Find out which accounts are in collections, and call and negotiate with those companies to reduce the negative impact on your credit. There’s nothing you can do with those on your credit report.”

Ammar said credit bureaus update their scores on the seventh of every month, sometimes as late as the fifteenth. So depending on when a borrower pays off an account in collections, it could take a month or more to reflect on the lender's report.

» MORE: Calculate your monthly mortgage payment with a trusted lender

Pay Higher Rates

When repairing credit or using government-backed loans aren’t feasible, borrowers might have to pay higher mortgage rates as a last resort.

Higher borrower risk equates to higher rates. Higher rates, in turn, mean a higher monthly mortgage payment.

About one in three Americans have credit scores below 670, often called sub-prime, according to Experian. While they will pay more to get a mortgage – if they can get approved from a subprime lender – there are safeguards in place including the “Ability to Repay” federal regulation aimed at avoiding a crisis like the 2008 financial collapse that was sparked by widespread defaults in subprime mortgages.

But, even if borrowers can jump through that hoop, should they wait until their credit is better before buying a house?

“I’m an ownership advocate,” said NAR’s Smith, a 38-year veteran of the real estate industry. “I would hope that everybody would work toward achieving that. If they can pull the trigger and buy a house, then that is a good way to fix the credit, by having that loan and paying on it for two to three years.”

After a few years of on-time payments, mortgage holders might be able to refinance for more favorable rates, depending on current market rates, he said.

Homebuyers who wait months to build an optimal credit score before applying for a mortgage can lose out on building equity in a new home as U.S. home prices continue to rise – albeit at a slower pace than 2021's record 18% gain. Home prices likely will gain 3.7% in 2025, says Realtor.com.

That price appreciation means buyers might be paying significantly higher future prices for the same house, making higher-rate loans preferable to renting in many cases, Smith said.

“If you can survive the payments, you buy,” he said.

That last part – whether the monthly payment is affordable – is key. Taking out an unaffordable mortgage can be catastrophic for borrowers who already have bad credit, he said.

» Don't Miss: Thinking about buying a home but want to secure a good rate? Find a lender that gives you the power to lock an interest rate for an extended period so you can shop around for a home comfortably knowing that your rate is secure and won't go up.