The average 30-year fixed rate mortgage is 6.35% today, an increase of 0.02% since yesterday. The 15-year fixed mortgage rate stands at 5.51%, up by 0.05%. The 30-year FHA mortgage now averages 5.66%, having dropped by 0.01. Meanwhile, the 30-year jumbo mortgage rate is 6.53%, reflecting an increase of 0.03%.

Live Updates

12/10/25

4:38 PM ET: Mortgage markets are responding positively to the Fed meeting and press conference. The Fed predicts higher growth and lower inflation with no major changes to the path of rates in coming years. This could mean the Fed will have an easier time issuing additional cuts in the future.

Connect with a lender to see what you qualify for.

3:26 PM ET: Powell on housing: A 0.25% cut to the federal funds rate won't make much difference to the housing market (a lower fed funds rate doesn't always translate to lower mortgage rates). Inventory is low, contributing to high prices. This isn't a problem the Fed is equipped to deal with.

3:17 PM ET: The best antidote for higher prices, says Powell, is a strong economy where incomes outpace inflation for years rather than attacking inflation aggressively. The Fed does want to get inflation back to 2% without hurting employment.

3:15 PM ET: Trump's rhetoric around replacing Powell as Fed Chair does not affect his decision making or Fed direction going forward.

3:13 PM ET: Powell expects tariff-induced price increases to peak in the first quarter of 2026. If no new tariffs are announced, inflation could come down toward the end of next year.

3:07 PM ET: Powell on the gradually-rising unemployment rate: The Fed has cut 0.75% in the last three meetings, which should support employment enough to avoid sharp increases in unemployment without inducing inflation. Both supply and demand for workers is down, so there is a balance in the economy, but only due to weakening of both sides.

3:00 PM ET: Powell: Everyone on the FOMC agrees that inflation is too high and also that labor has softened. This is leading to varying opinions within the Fed on how to deal with both issues. This is the reason for three dissenters for this meeting's decision. Powell says the Fed is well positioned to make data-driven decisions in future meetings.

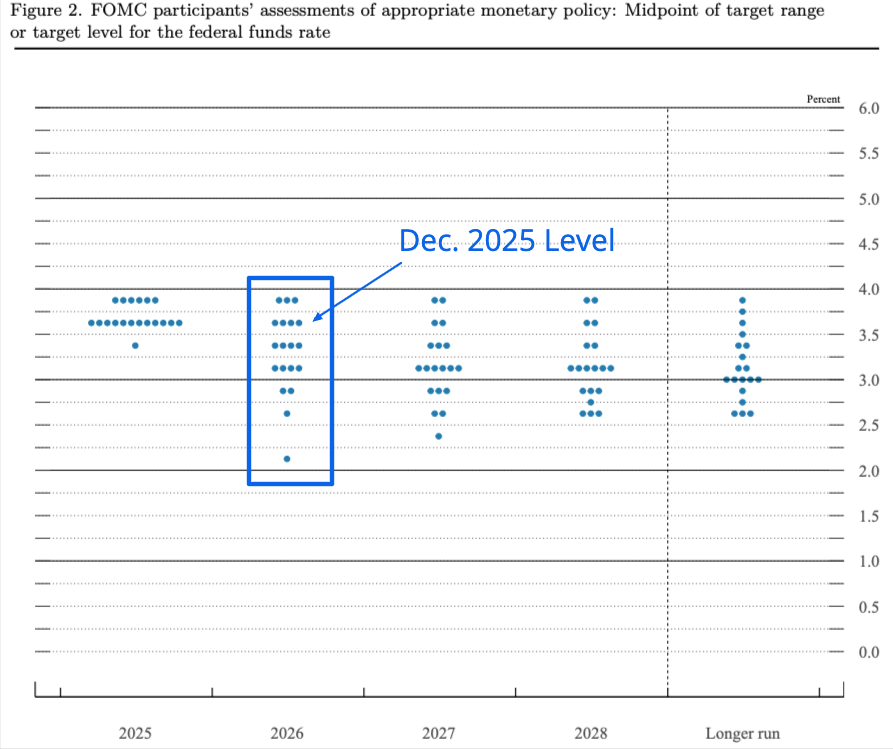

2:50 PM ET: The Fed projects the federal funds rate at 3.4% at the end of 2026 (0.25% below today's new level) and 3.1% at the end of 2027 (0.50% below today's level), which matches September's projection.

2:45 PM ET: Powell says employment has softened but risks to inflation have increased due to tariffs. This will make the Fed's job harder as it balances both risks. Policies that spur employment (lower rates) could also increase inflation.

2:40 PM ET: Fed Chair Jerome Powell says labor has softened recently and downside risks of employment have increased. Inflation has eased since 2022, but is above the Fed's 2% long-run goal. Inflation expectations are now at 2.9% for 2025 and 2.4% for 2026.

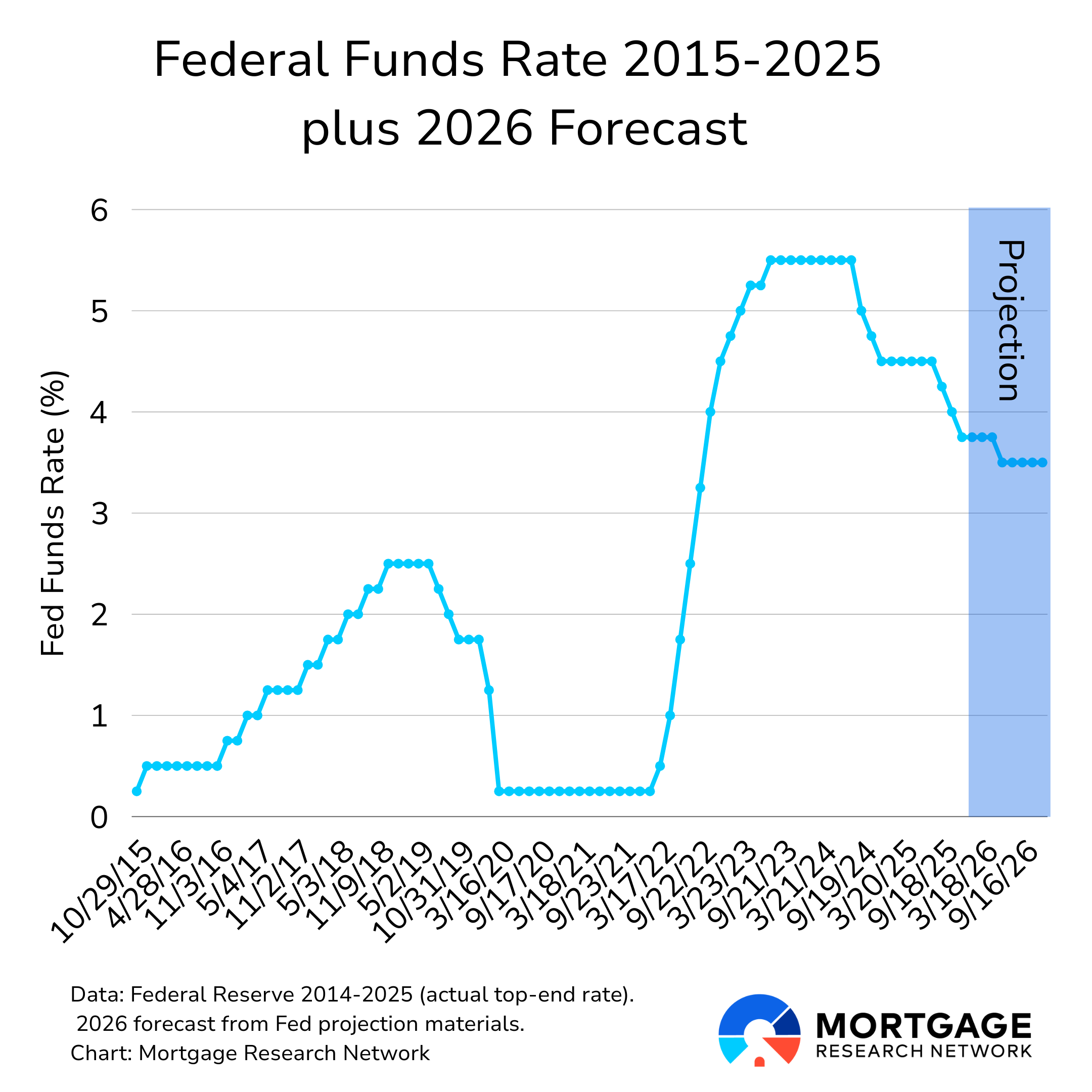

Fed Cuts by 0.25%

The Federal Reserve cut its key interest rate by 0.25% today to a range of 3.50-3.75%.

It's the sixth cut since the Fed started easing monetary policy in September 2024.

Today's move was widely expected by mortgage markets. Still, mortgage rates are improving after Fed Chair Jerome Powell confirmed that inflation is elevated but under control, and that the labor market is softening.

Check today's rates with top lenders.

Today's decision wasn't made unanimously. Three members of the Federal Open Market Committee (or FOMC, the Fed's rate-setting arm) dissented, the first time that's happened since 2019. One member wanted a 0.50% cut while two others wanted no change.

What's ahead in 2026?

The key document in the Fed's economic projections is the "dot plot." This is a chart that shows how each member of the Fed expects the Fed funds rate to move in the coming months and years.

December's dot plot indicates that the fed funds rate could end up between 3.25%-3.5% in 2026 which would be 0.25% below today's level. The best case scenario currently is an additional 0.25% cut for a total 0.50% reduction from today's new level by the end of 2026.

But the Fed's official projection, as reiterated in the post-meeting press conference, that the Fed is expecting to cut just one more time in 2026.

Below is a view of December's dot plot with a blue square added to 2026 fed funds rate expectations.

Mortgage Rate Trends: Past 90 Days

Purchase Rates

| Loan Type | Rate | APR | Daily Change | Monthly Change |

|---|---|---|---|---|

| 30-Year Fixed | 6.35% | 6.38% | +0.02% | +0.04% |

| 15-Year Fixed | 5.51% | 5.55% | +0.05% | +0.08% |

| 30-Year Fixed FHA | 5.66% | 6.87% | -0.01% | +0.11% |

| 30-Year Fixed VA | 5.74% | 5.88% | +0.02% | +0.08% |

| 30-Year Fixed USDA | 5.76% | 5.91% | +0.01% | +0.15% |

| 30-Year Fixed Jumbo | 6.53% | 6.55% | +0.03% | -0.15% |

| 5/6 Year ARM | 6.15% | 6.19% | -0.01% | -0.14% |

Refinance Rates

| Loan Type | Rate | APR | Daily Change | Monthly Change |

|---|---|---|---|---|

| 30-Year Fixed | 6.45% | 6.47% | +0.03% | +0.06% |

| 15-Year Fixed | 5.49% | 5.52% | +0.05% | +0.08% |

| 30-Year Fixed FHA | 5.63% | 6.83% | -0.01% | +0.11% |

| 30-Year Fixed VA | 5.79% | 5.93% | +0.04% | +0.1% |

| 5/6 Year ARM | 6.16% | 6.19% | +0.03% | -0.15% |

👉Stay ahead of the market. Subscribe to the Mortgage Research Network Podcast.

Fed chair's news conference

Powell's news conference is scheduled for 2:30 PM ET and always seems to sway markets. Powell often tempers expectations for future cuts during the conference, reversing optimism that builds before it.

That's why mortgage rates often rise late in the day after the Fed announcement.

However, Fed chair Powell could be leaving his position in May, and the president is already interviewing replacements. Does this mean Powell is already a lame duck? If so, markets might shrug off his remarks. If not, mortgage rates might rise if he's pessimistic about future cuts or fall if he's optimistic about them.

What went into today's decision?

Fed agreement on policy is divided. One member wanted a deeper rate cut while two wanted no cut at all. The differences of opinion are warranted.

The decision was made without a recent version of a key report, the Employment Situation, due to the government shutdown. It's one of the most important pieces of data for rate-cut decisions. The last report covered September 2025. October's report will not be published, and November data won't be released until December 16.

The lack of data put the Fed in a tricky spot: the central bank risks cutting rates into a robust economy, conditions that could spur inflation. Or, it could keep rates high, spurring employers to cut jobs, adding to rising unemployment numbers.

Labor data has been showing signs of weakness

The economy has shed jobs two of the last four months for which we have data, a rare event. In the past decade, the economy has only lost jobs during three months – all during COVID.

In the past six months, only 58,500 jobs were added monthly nationwide on average. The 24-month average prior was 171,000 jobs. Keep in mind that the economy needs to add 153,000 per month just to keep up with new workers entering the workforce according to the St. Louis Federal Reserve.

The unemployment rate is still low at just 4.4%, but that's up from 3.8% two years ago.

Inflation is nearly in line with Fed goals at 2.6% based on readings of the seasonally-adjusted personal consumption expenditures (PCE) index. So curbing inflation isn't as big a concern for the Fed as in 2022 when that reading was closer to 5%.

In light of employment and inflation data (the two elements the Fed must balance), it's no wonder that Powell and the Fed cut rates. But the decision likely felt akin to walking around the house blindfolded: you may not know you made a wrong move until it's too late.

What's coming up?

Although economic reports are usually the main drivers of changes to mortgage rates, they're not the only ones. The general mood in markets and economically consequential news can also affect those rates. News items concerning employment, inflation, tariffs and deficit funding are especially influential at the moment.

With the government now reopened, we can anticipate the publication of official reports to slowly return to normal. Had the shutdown been brief, we could have expected a flood of official economic reports on reopening. But the length of the hiatus means that it is no longer the case. Data won't have been collected — let alone compiled and prepared for publication — during the shutdown. So, delayed and even canceled reports are inevitable.

This week

Markets will spend Wednesday and Thursday absorbing the Fed decision and press conference.

Mortgage rates today and tomorrow

There are two economic reports on today's MarketWatch economic calendar. The more important one is due at 8:30 a.m. (EST), and is the third quarter's employment cost index.

That is an important inflation indicator for wages. If the FOMC has a chance, it might consider this report when deciding whether to cut general interest rates this afternoon.

Markets are expecting that index to be 0.9% in the third quarter, unchanged since the second quarter. If it comes in higher than that, mortgage rates might rise, but a lower figure could see them fall.

Today's other report is the federal budget for November, and is due at 2 p.m. EST. This rarely moves mortgage rates.

Tomorrow brings a couple of relatively minor reports: initial jobless claims during the week ending Dec. 6, and the September trade deficit. If either of those affects mortgage rates, it's unlikely to be by much.