The average 30-year fixed rate mortgage is 6.28% today, an increase of 0.04% since yesterday. The 15-year fixed mortgage rate stands at 5.4%, up by 0.03%. The 30-year FHA mortgage now averages 5.58%, having dropped by 0.01. Meanwhile, the 30-year jumbo mortgage rate is 6.47%, reflecting no change.

Breaking: Fed cuts by 0.25%. See our live coverage of today's Fed rate announcement.

What to expect from the Fed's Wednesday rate announcement

The Federal Reserve's rate-setting meeting is almost certain to influence mortgage rates more than anything else this week — and maybe this month.

"The Federal Reserve’s decision will take center stage in the coming week, with the central bank widely expected to cut general interest rates after recent weak U.S. jobs data," said The Wall Street Journal last Friday.

Markets are very confident that the Federal Open Market Committee (FOMC, the Fed's rate-setting body) will implement a quarter-point (0.25% or 25 basis points) cut. Indeed, the CME FedWatch tool put the probability at 86.2% over the weekend.

Recent economic data have tended to make such a cut more likely. Last Friday's inflation data showed little change in how much prices were rising, while last Wednesday's ADP employment report showed worse employment numbers than markets were expecting. Both those boosted the argument for a cut.

"Fed officials should be able to focus on the wavering labor market and cut interest rates by another quarter percentage point at their final meeting of the year next week, thanks to relatively stable inflation data," Barron's said on Friday.

Of course, there's still an outside chance that the Fed will disappoint, holding rates steady. That would likely be bad for mortgage rates because markets have already priced in the expected cut, and will need to react to the surprise.

However, that's not the only threat to lower mortgage rates that arises from Wednesday's Fed events.

👉Stay ahead of the market. Subscribe to the Mortgage Research Network Podcast.

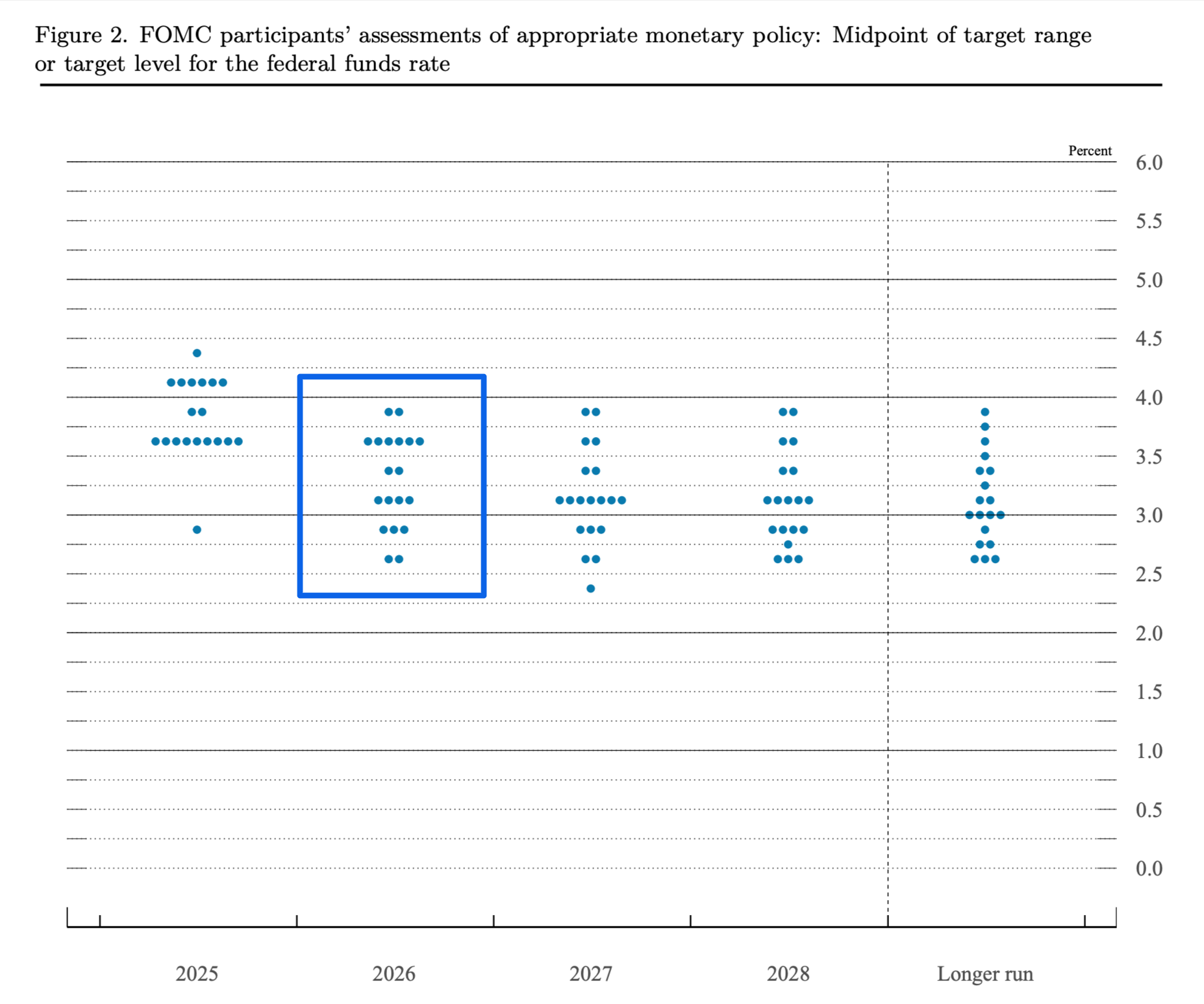

The "dot plot" threat

Markets are as worried by the prospects for 2026 cuts to general interest rates as they are by what the Fed does on Wednesday.

"The [U.S. Treasury] 10-year note and 30-year bond had their worst weekly performances since April and May on conflicting economic data that is sowing doubts about how much the Federal Reserve can cut interest rates in 2026," said MarketWatch on Friday afternoon. (Mortgage rates often shadow 10-year Treasury notes.)

"Traders widely expect a quarter-point rate cut next week that will push the central bank’s main policy target down to between 3.5% and 3.75%," continued MarketWatch. "But they were less certain about next year and see a decent chance that the central bank won’t cut rates again through next March."

Markets will be more certain at 2 p.m. Eastern on Wednesday. That's when the Fed publishes its quarterly summary of economic projections, which includes a document called the "dot plot."

Britannica

explains: "The Fed dot plot is a chart that shows you where each FOMC

member thinks interest rates will be by the end of the current year, two

or three (depending on the time of year) consecutive years after, and

the more ambiguous 'longer run.' Each 'dot' represents a member’s

individual view."

Mortgage Rate Trends: Past 90 Days

Purchase Rates

| Loan Type | Rate | APR | Daily Change | Monthly Change |

|---|---|---|---|---|

| 30-Year Fixed | 6.28% | 6.3% | +0.04% | -0.04% |

| 15-Year Fixed | 5.4% | 5.45% | +0.03% | -0.05% |

| 30-Year Fixed FHA | 5.58% | 6.8% | -0.01% | -0.01% |

| 30-Year Fixed VA | 5.66% | 5.81% | +0.02% | +-0% |

| 30-Year Fixed USDA | 5.64% | 5.78% | +0.08% | +0.08% |

| 30-Year Fixed Jumbo | 6.47% | 6.49% | +0% | -0.21% |

| 5/6 Year ARM | 6.09% | 6.12% | +0.04% | -0.18% |

Refinance Rates

| Loan Type | Rate | APR | Daily Change | Monthly Change |

|---|---|---|---|---|

| 30-Year Fixed | 6.36% | 6.38% | +0.04% | -0.05% |

| 15-Year Fixed | 5.39% | 5.43% | +0.05% | -0.03% |

| 30-Year Fixed FHA | 5.56% | 6.77% | -0.01% | +0% |

| 30-Year Fixed VA | 5.7% | 5.83% | +0.02% | +0% |

| 5/6 Year ARM | 6.1% | 6.14% | +0.04% | -0.28% |

Example dot plot from the September 2025 Fed meeting indicating 2026 rates in the 3.375-3.625% range. A higher 2026 projection after the December meeting could push rates up immediately. Source: FOMC (blue emphasis box added)

Dot plots can be hugely influential because they give markets insights into the minds of the very people who will move general interest rates in the future.

And bad news (meaning fewer-than-expected rate cuts in 2026) could send mortgage rates sharply higher on Wednesday afternoon and beyond, even if the Fed cuts general rates that day.

Fed chair's news conference

We'd normally warn that Fed Chair Jerome Powell's news conference (due Wednesday at 2:30 p.m. Eastern) has the potential to influence mortgage rates as much as the rate announcement and dot plot. However, we're genuinely unsure how markets will react to his remarks this time.

Powell is due to retire in May, and could already be a lame-duck chair. Certainly, his former consensus-building approach to his job appears to have fallen apart recently, partly because other Fed officials have already left or have indicated they plan to go in a few months. Division and dissent among FOMC members is the new normal.

Will markets still treat his remarks this week with the awe they have in the past? We'll have to wait and see.

What's coming up?

Although economic reports are usually the main drivers of changes to mortgage rates, they're not the only ones. The general mood in markets and economically consequential news can also affect those rates. News items concerning employment, inflation, tariffs and deficit funding are especially influential at the moment.

With the government reopening, we can anticipate the publication of official reports to slowly return to normal. Had the shutdown been brief, we could have expected a flood of official economic reports on reopening. But the length of the hiatus means that it is no longer the case. Data won't have been collected — let alone compiled and prepared for publication — during the shutdown. So, delayed or even canceled reports are inevitable.

Mortgage rates today and tomorrow

There are no economic reports on today's MarketWatch economic calendar.

Tomorrow brings two reports. And one in particular may affect mortgage rates, not least because it could influence the Fed's rate-setting decision. That's the job openings and labor turnover survey (JOLTS) for October.

"The Job Openings and Labor Turnover Survey (JOLTS) program of the Bureau of Labor Statistics (BLS) produces monthly and annual estimates of job openings, hires, and separations for the nation," says the BLS. "The JOLTS program also produces monthly state estimates for all 50 states and the District of Columbia at the total nonfarm industry level."

Markets often shrug off this excellent report because it's usually a little stale for their tastes. However, this time, thanks to the government shutdown, it will be the freshest official employment data markets and the Fed have seen for months.